Academic Profile

Statistics

Similar Authors

Papers on arXiv

We extend upon the saddle-point equation presented in [1] to derive large-time model-implied volatility smiles, providing its theoretical foundation and studying its applications in classical models...

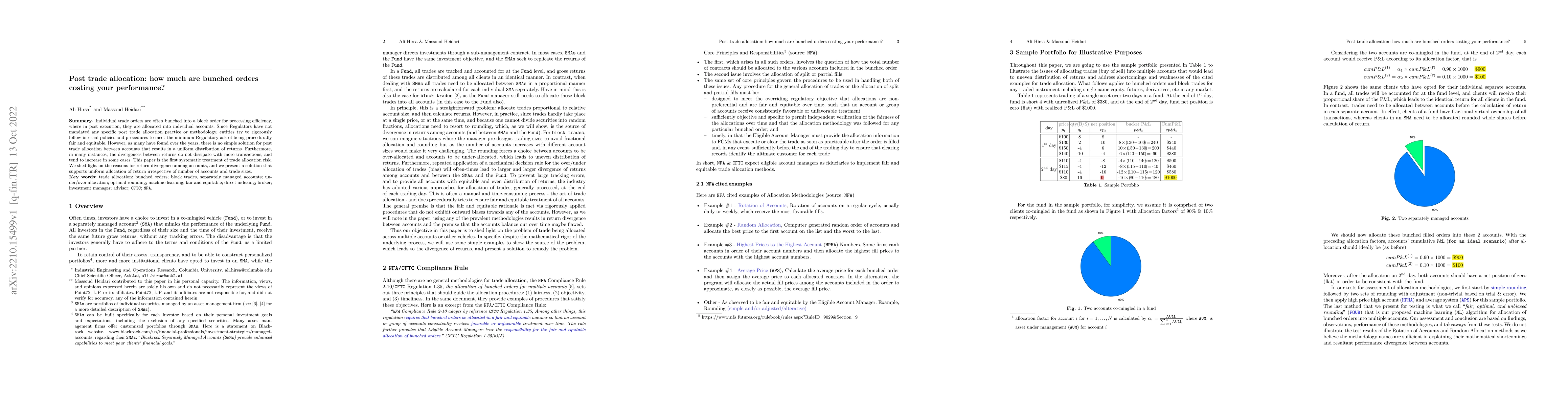

Individual trade orders are often bunched into a block order for processing efficiency, where in post execution, they are allocated into individual accounts. Since Regulators have not mandated any s...

We develop an unsupervised deep learning method to solve the barrier options under the Bergomi model. The neural networks serve as the approximate option surfaces and are trained to satisfy the PDE ...

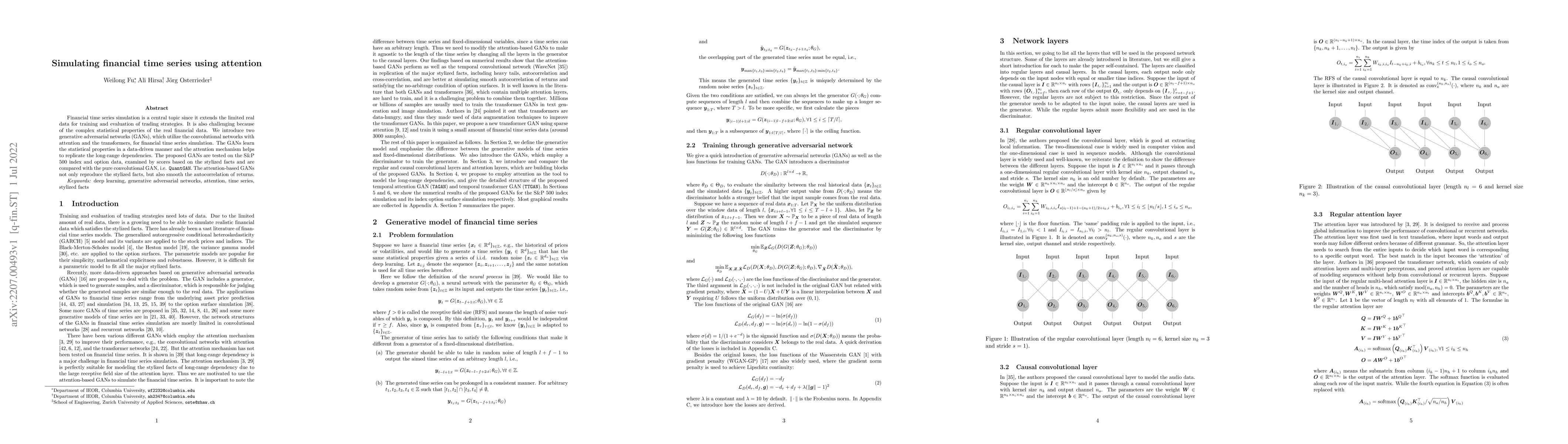

Financial time series simulation is a central topic since it extends the limited real data for training and evaluation of trading strategies. It is also challenging because of the complex statistica...

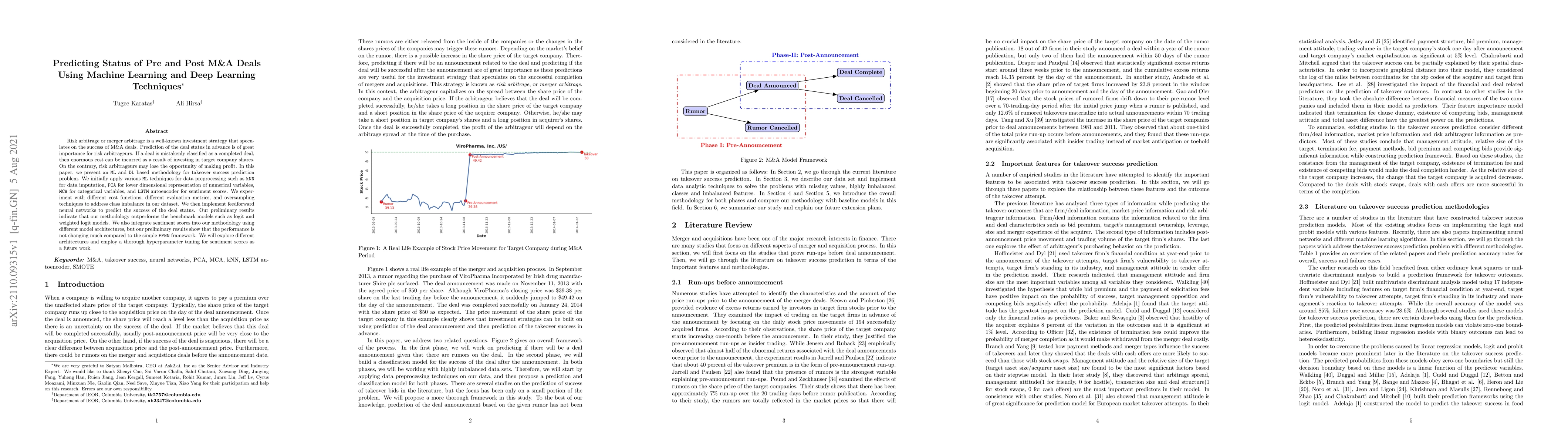

Risk arbitrage or merger arbitrage is a well-known investment strategy that speculates on the success of M&A deals. Prediction of the deal status in advance is of great importance for risk arbitrage...

Institutional investors have been increasing the allocation of the illiquid alternative assets such as private equity funds in their portfolios, yet there exists a very limited literature on cash fl...

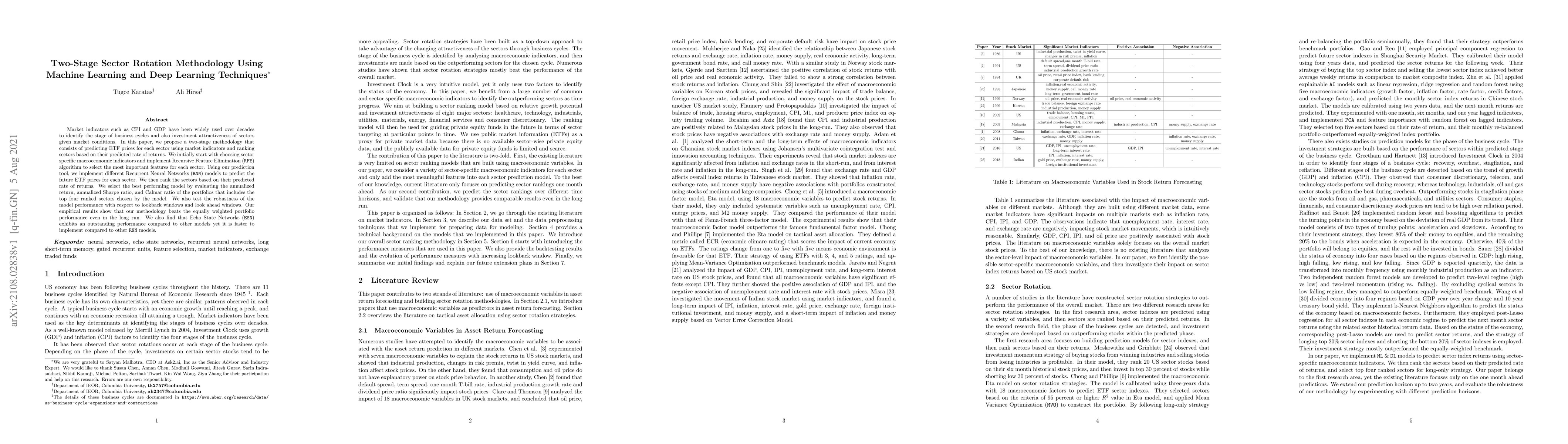

Market indicators such as CPI and GDP have been widely used over decades to identify the stage of business cycles and also investment attractiveness of sectors given market conditions. In this paper...

Financial trading has been widely analyzed for decades with market participants and academics always looking for advanced methods to improve trading performance. Deep reinforcement learning (DRL), a...

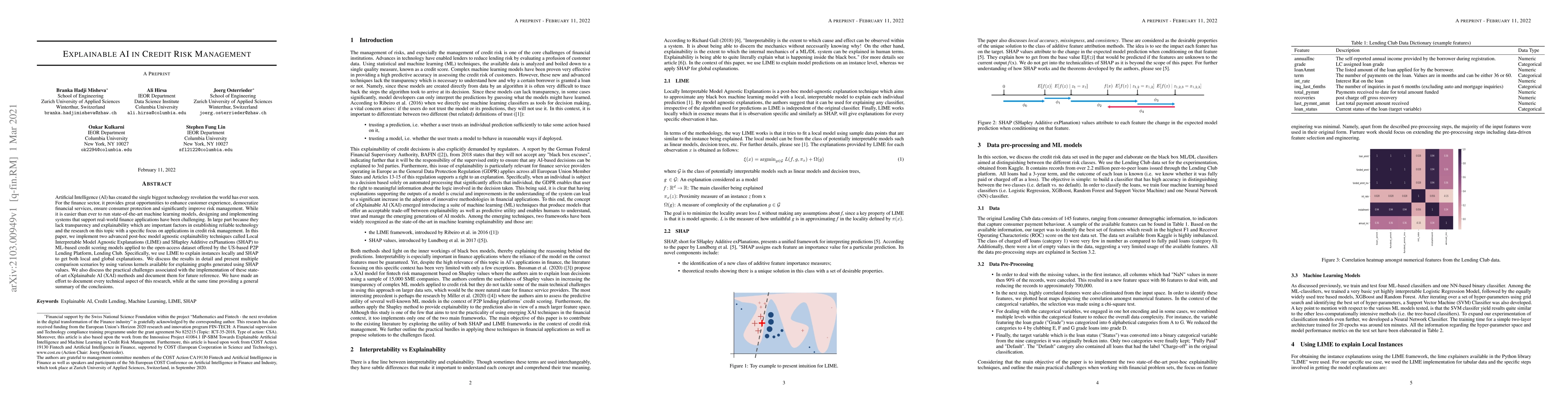

Artificial Intelligence (AI) has created the single biggest technology revolution the world has ever seen. For the finance sector, it provides great opportunities to enhance customer experience, dem...

We propose a framework for generating samples from a probability distribution that differs from the probability distribution of the training set. We use an adversarial process that simultaneously tr...

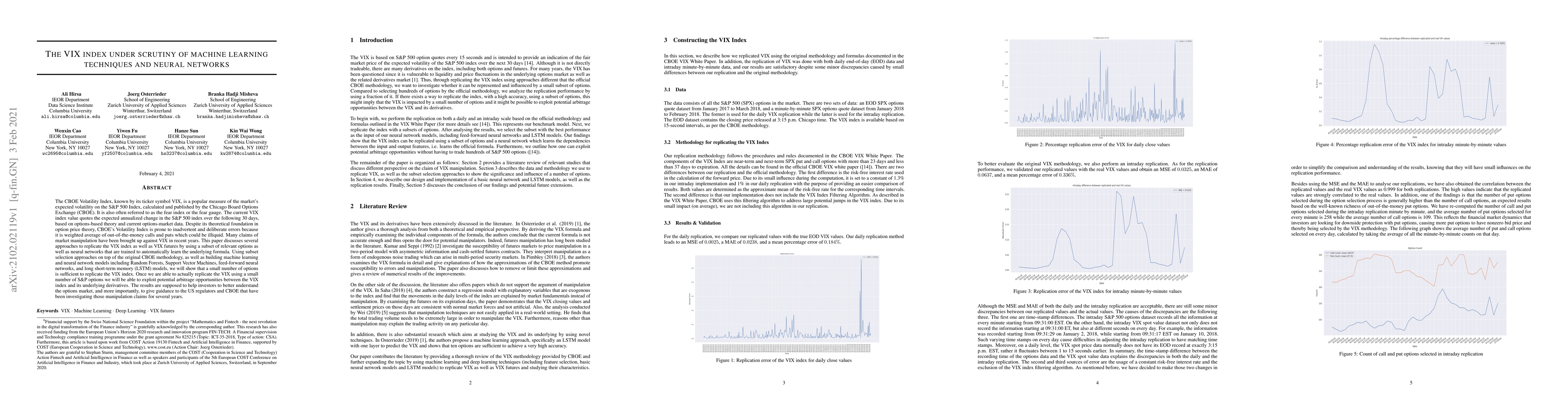

The CBOE Volatility Index, known by its ticker symbol VIX, is a popular measure of the market's expected volatility on the SP 500 Index, calculated and published by the Chicago Board Options Exchang...

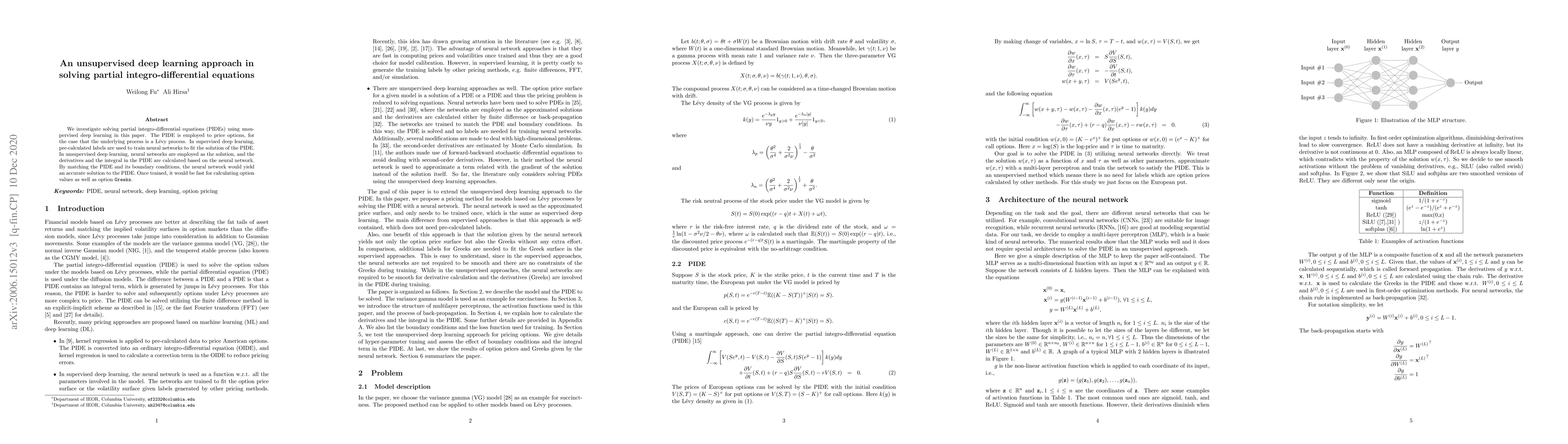

We investigate solving partial integro-differential equations (PIDEs) using unsupervised deep learning in this paper. To price options, assuming underlying processes follow Levy processes, we requir...

We investigate methods for pricing American options under the variance gamma model. The variance gamma process is a pure jump process which is constructed by replacing the calendar time by the gamma...