Academic Profile

Statistics

Similar Authors

Papers on arXiv

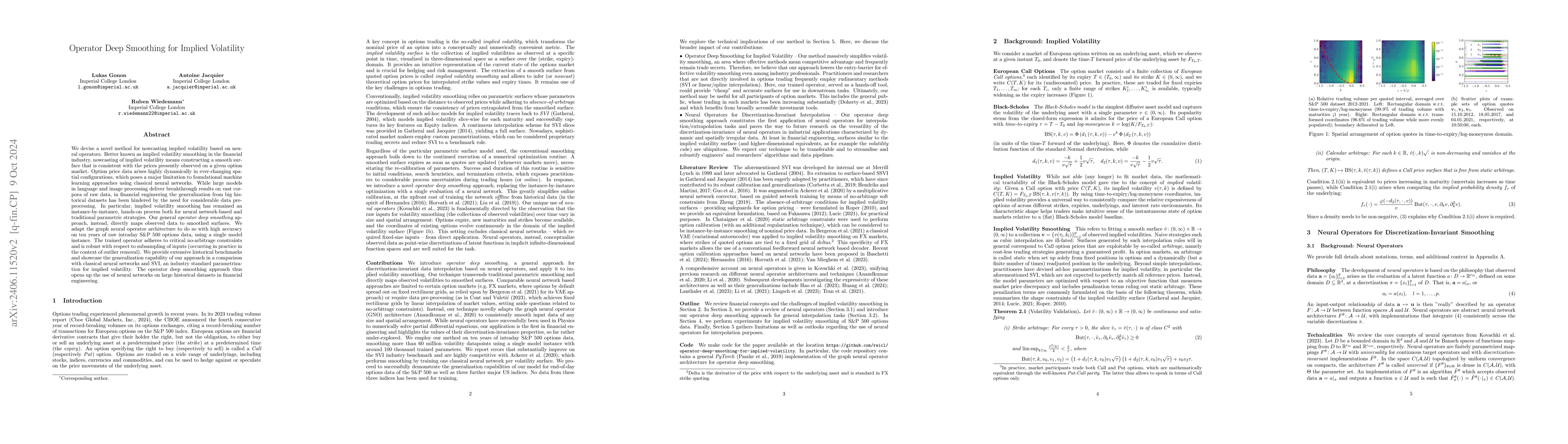

We devise a novel method for implied volatility smoothing based on neural operators. The goal of implied volatility smoothing is to construct a smooth surface that links the collection of prices obs...

One the one hand, rough volatility has been shown to provide a consistent framework to capture the properties of stock price dynamics both under the historical measure and for pricing purposes. On t...

Classical Physics-informed neural networks (PINNs) approximate solutions to PDEs with the help of deep neural networks trained to satisfy the differential operator and the relevant boundary conditio...

This article provides an understanding of Natural Language Processing techniques in the framework of financial regulation, more specifically in order to perform semantic matching search between rule...

Quantum computing has recently appeared in the headlines of many scientific and popular publications. In the context of quantitative finance, we provide here an overview of its potential.

We study concentration properties for laws of non-linear Gaussian functionals on metric spaces. Our focus lies on measures with non-Gaussian tail behaviour which are beyond the reach of Talagrand's ...

Recent mathematical advances in the context of rough volatility have highlighted interesting and intricate connections between path-dependent partial differential equations and backward stochastic p...

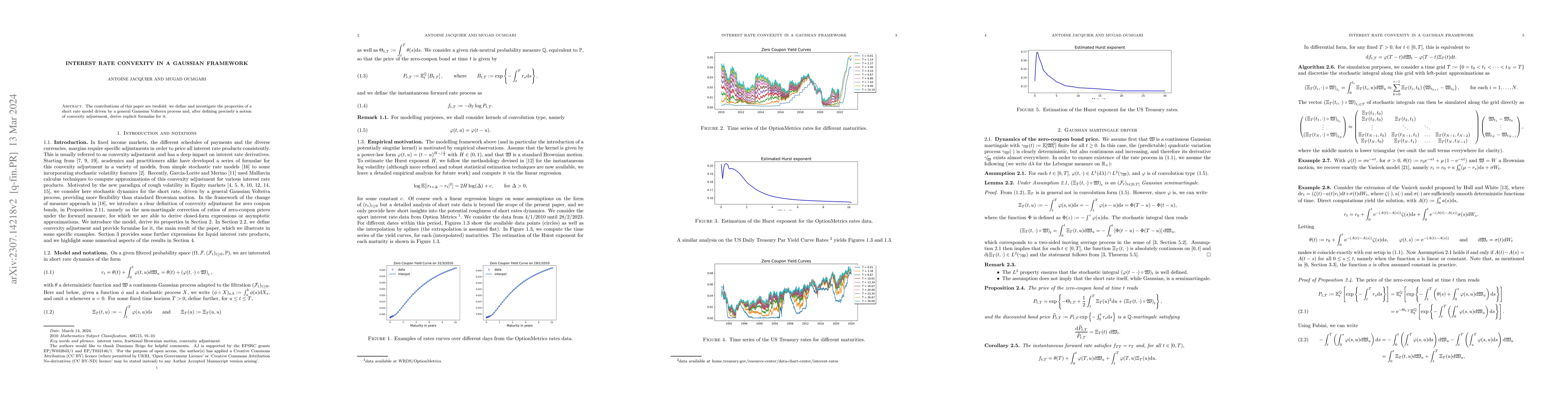

The contributions of this paper are twofold: we define and investigate the properties of a short rate model driven by a general Gaussian Volterra process and, after defining precisely a notion of co...

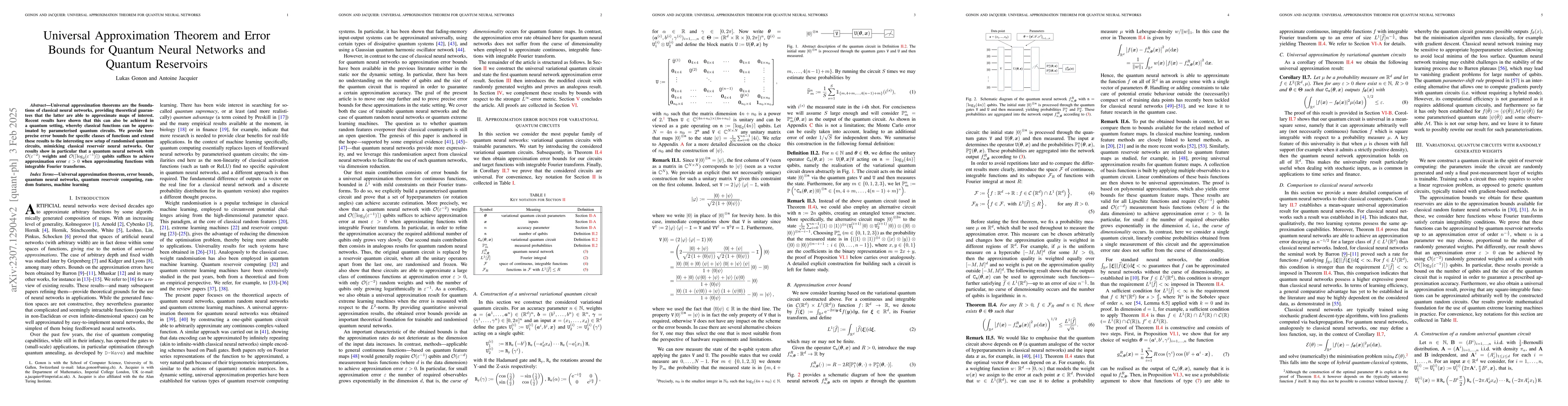

Universal approximation theorems are the foundations of classical neural networks, providing theoretical guarantees that the latter are able to approximate maps of interest. Recent results have show...

We study how the climate transition through a low-carbon economy, implemented by carbon pricing, propagates in a credit portfolio and precisely describe how carbon price dynamics affects credit risk...

We construct a deep learning-based numerical algorithm to solve path-dependent partial differential equations arising in the context of rough volatility. Our approach is based on interpreting the PD...

In the setting of stochastic Volterra equations, and in particular rough volatility models, we show that conditional expectations are the unique classical solutions to path-dependent PDEs. The latte...

We show the existence of a stationary measure for a class of multidimensional stochastic Volterra systems of affine type. These processes are in general not Markovian, a shortcoming which hinders th...

We provide explicit small-time formulae for the at-the-money implied volatility, skew and curvature in a large class of models, including rough volatility models and their multi-factor versions. Our...

We develop a new analysis for portfolio optimisation with options, tackling the three fundamental issues with this problem: asymmetric options' distributions, high dimensionality and dependence stru...

We provide a detailed importance sampling analysis for variance reduction in stochastic volatility models. The optimal change of measure is obtained using a variety of results from large and moderat...

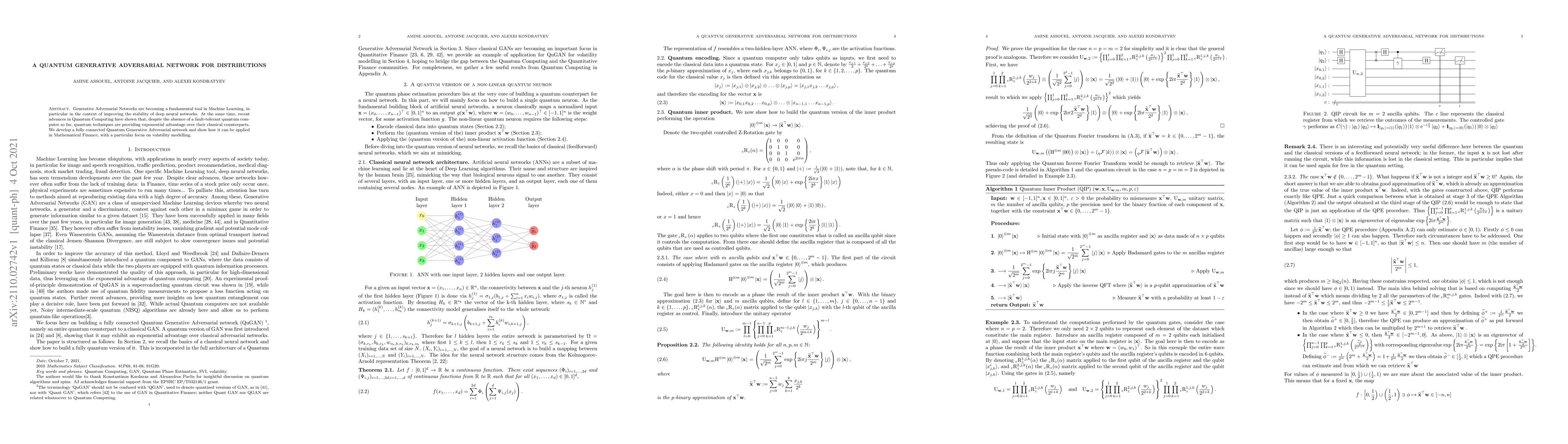

Generative Adversarial Networks are becoming a fundamental tool in Machine Learning, in particular in the context of improving the stability of deep neural networks. At the same time, recent advance...

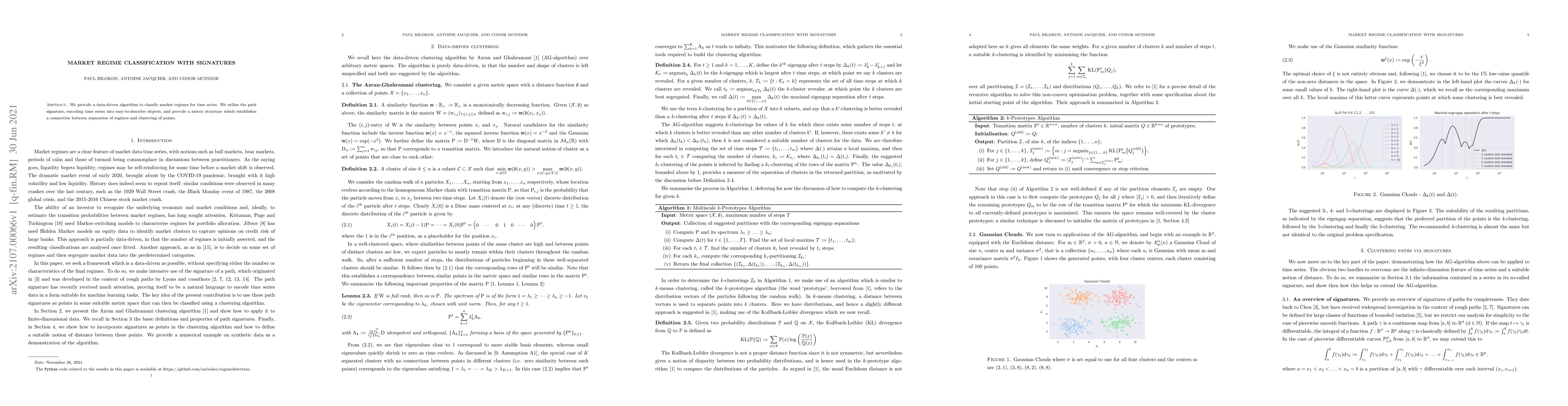

We provide a data-driven algorithm to classify market regimes for time series. We utilise the path signature, encoding time series into easy-to-describe objects, and provide a metric structure which...

We develop a product functional quantization of rough volatility. Since the quantizers can be computed offline, this new technique, built on the insightful works by Luschgy and Pages, becomes a stro...

We revisit the foundational Moment Formula proved by Roger Lee fifteen years ago. We show that when the underlying stock price martingale admits finite log-moments E[|log(S)|^q] for some positive q,...

We provide a unified treatment of pathwise Large and Moderate deviations principles for a general class of multidimensional stochastic Volterra equations with singular kernels, not necessarily of co...

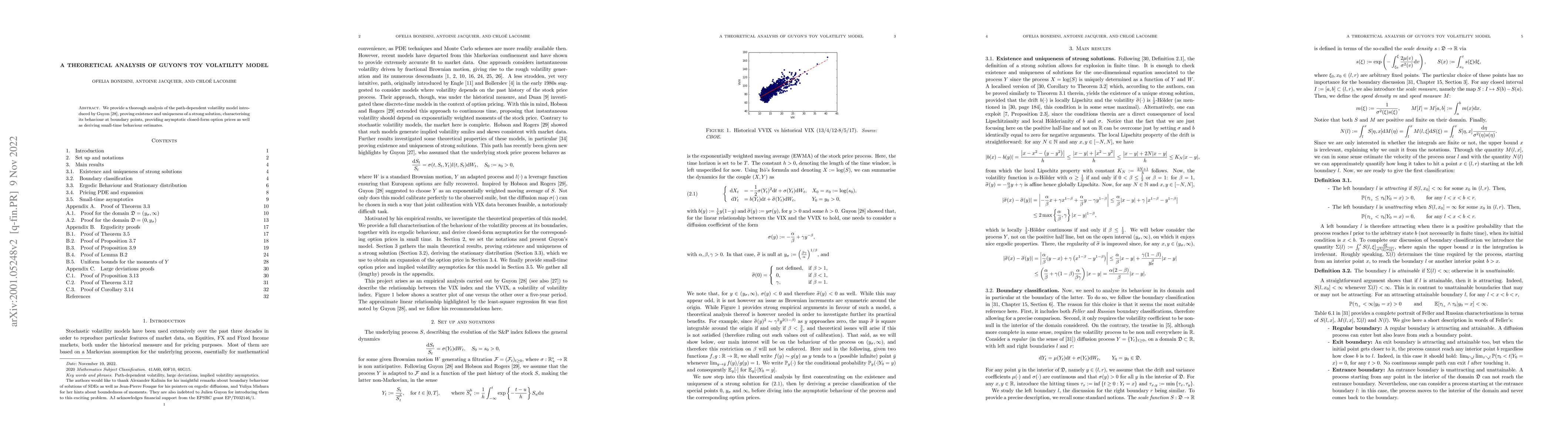

We provide a thorough analysis of the path-dependent volatility model introduced by Guyon \cite{G17}, proving existence and uniqueness of a strong solution, characterising its behaviour at boundary ...

We prove strong existence and uniqueness, and H\"older regularity, of a large class of stochastic Volterra equations, with singular kernels and non-Lipschitz diffusion coefficient. Extending Yamada-...

We propose a hybrid quantum-classical algorithm, originated from quantum chemistry, to price European and Asian options in the Black-Scholes model. Our approach is based on the equivalence between t...

We develop a dynamic version of the SSVI parameterisation for the total implied variance, ensuring that European vanilla option prices are martingales, hence preventing the occurrence of arbitrage, ...

We introduce a new deep-learning based algorithm to evaluate options in affine rough stochastic volatility models. Viewing the pricing function as the solution to a curve-dependent PDE (CPDE), depen...

We extend previous large deviations results for the randomised Heston model to the case of moderate deviations. The proofs involve the G\"artner-Ellis theorem and sharp large deviations tools.

We investigate the links between various no-arbitrage conditions and the existence of pricing functionals in general markets, and prove the Fundamental Theorem of Asset Pricing therein. No-arbitrage...

The non-Markovian nature of rough volatility processes makes Monte Carlo methods challenging and it is in fact a major challenge to develop fast and accurate simulation algorithms. We provide an eff...

We study the small-time behaviour of the rough Bergomi model, introduced by Bayer, Friz and Gatheral (2016), and prove a large deviations principle for a rescaled version of the normalised log stock...

Deep learning methods have become a widespread toolbox for pricing and calibration of financial models. While they often provide new directions and research results, their `black box' nature also resu...

We introduce a canonical way of performing the joint lift of a Brownian motion $W$ and a low-regularity adapted stochastic rough path $\mathbf{X}$, extending [Diehl, Oberhauser and Riedel (2015). A L\...

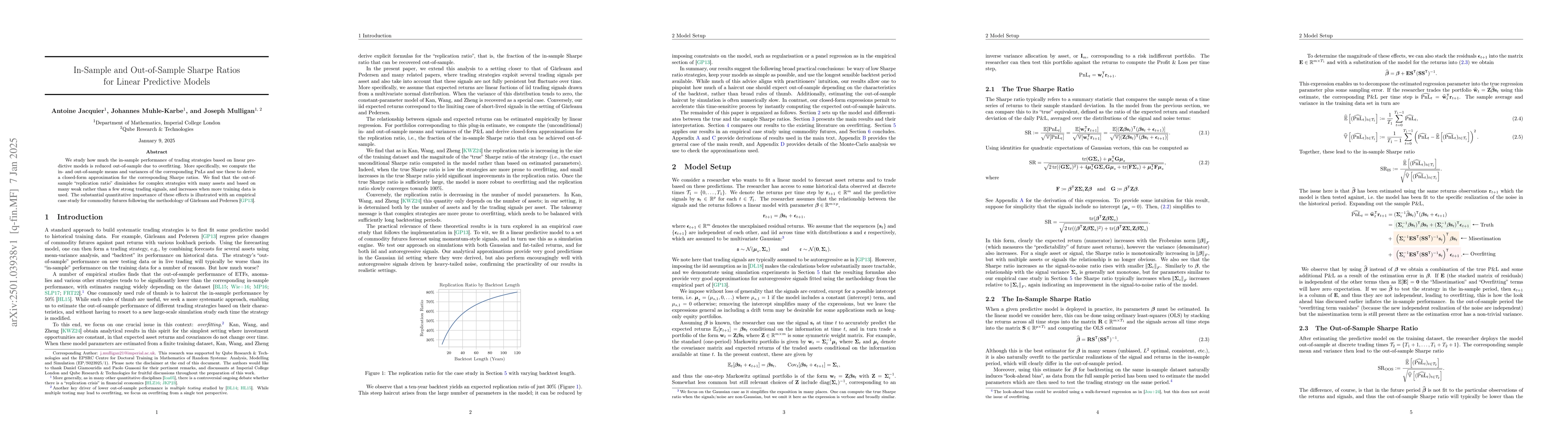

We study how much the in-sample performance of trading strategies based on linear predictive models is reduced out-of-sample due to overfitting. More specifically, we compute the in- and out-of-sample...

We propose a tractable extension of the rough Bergomi model, replacing the fractional Brownian motion with a generalised grey Brownian motion, which we show to be reminiscent of models with stochastic...

We elucidate physical aspects of path signatures by formulating randomised path developments within the framework of matrix models in quantum field theory. Using tools from physics, we introduce a new...

We frame novelty detection on path space as a hypothesis testing problem with signature-based test statistics. Using transportation-cost inequalities of Gasteratos and Jacquier (2023), we obtain tail ...

We investigate quantum systems perturbed by noise in the form of repeated interactions between the system and the environment. As the number of interactions (aka time steps) tends to infinity, we show...

We provide here a universal approximation theorem with precise quantitative error bounds for noisy quantum neural networks. We focus on applications to Quantitative Finance, where target functions are...

Enforcing functional inequality constraints such as monotonicity and convexity in neural networks is a fundamental challenge in many industrial and scientific applications. Classical one-sided penalty...