Academic Profile

Statistics

Similar Authors

Papers on arXiv

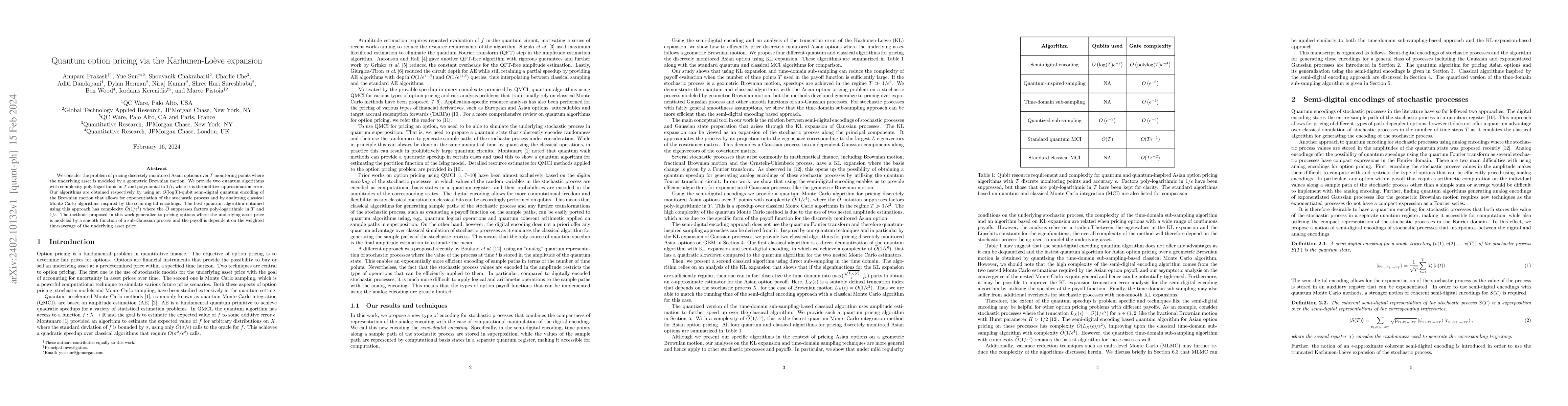

We consider the problem of pricing discretely monitored Asian options over $T$ monitoring points where the underlying asset is modeled by a geometric Brownian motion. We provide two quantum algorith...

Quantum machine learning has the potential for a transformative impact across industry sectors and in particular in finance. In our work we look at the problem of hedging where deep reinforcement le...

We present a method for finding optimal hedging policies for arbitrary initial portfolios and market states. We develop a novel actor-critic algorithm for solving general risk-averse stochastic cont...

We present an actor-critic-type reinforcement learning algorithm for solving the problem of hedging a portfolio of financial instruments such as securities and over-the-counter derivatives using pur...

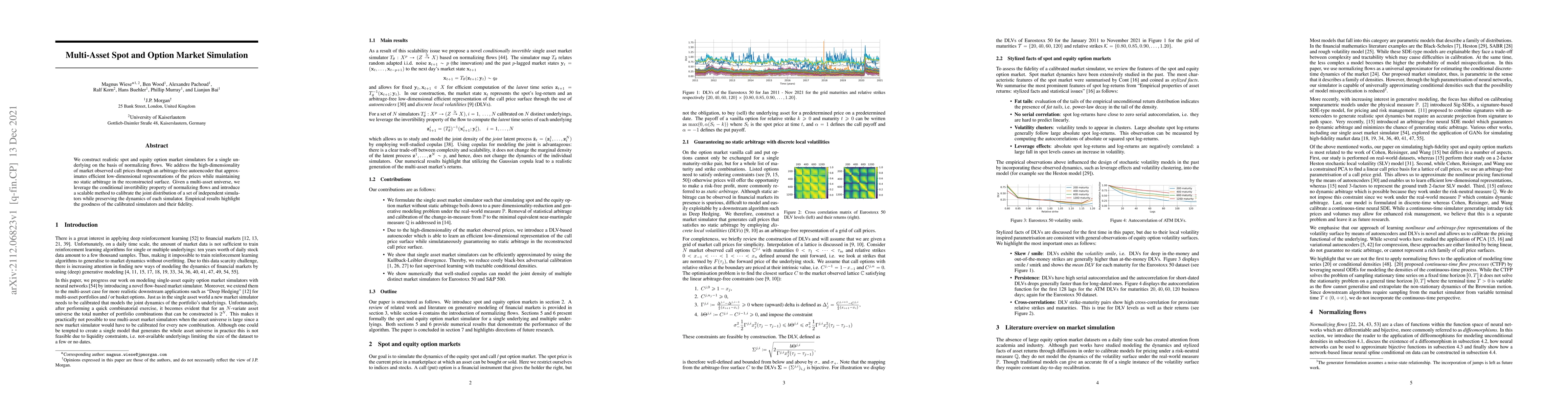

We construct realistic spot and equity option market simulators for a single underlying on the basis of normalizing flows. We address the high-dimensionality of market observed call prices through a...

We present a machine learning approach for finding minimal equivalent martingale measures for markets simulators of tradable instruments, e.g. for a spot price and options written on the same underl...

We present a numerically efficient approach for learning a risk-neutral measure for paths of simulated spot and option prices up to a finite horizon under convex transaction costs and convex trading...

Neural network based data-driven market simulation unveils a new and flexible way of modelling financial time series without imposing assumptions on the underlying stochastic dynamics. Though in thi...

We construct realistic equity option market simulators based on generative adversarial networks (GANs). We consider recurrent and temporal convolutional architectures, and assess the impact of state...

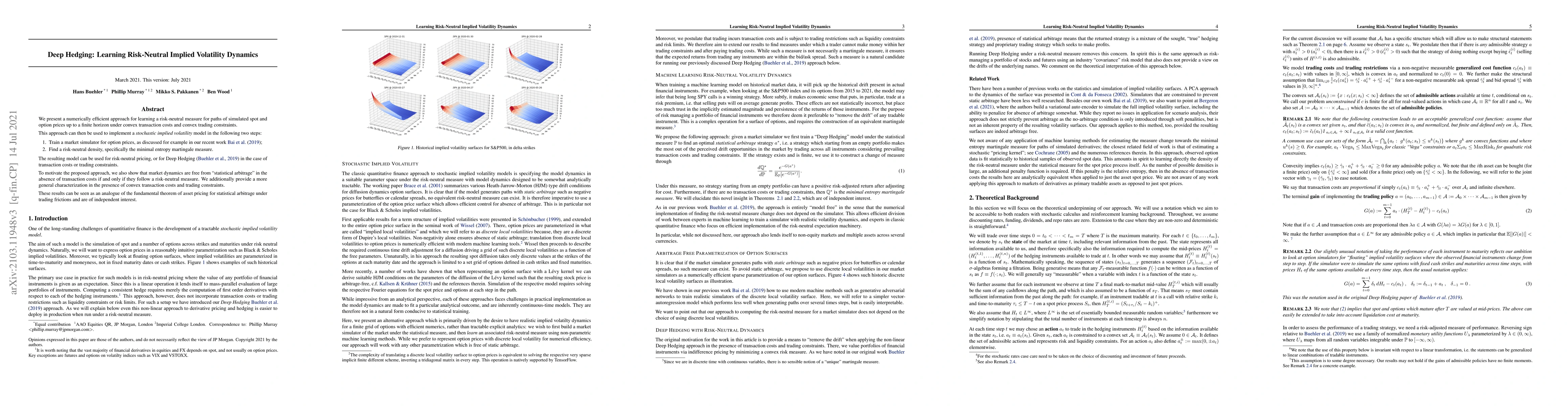

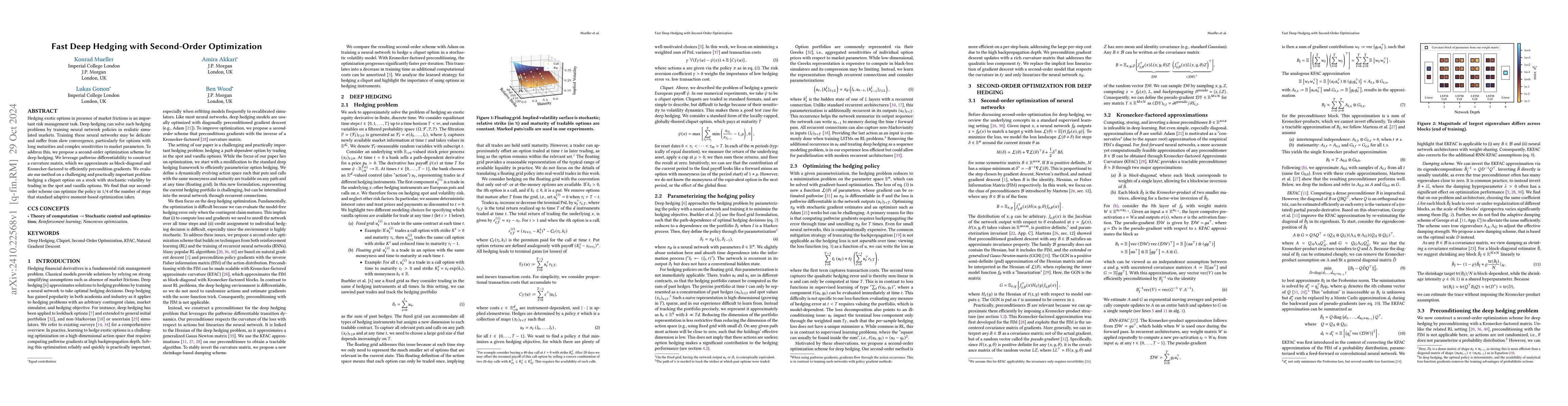

Hedging exotic options in presence of market frictions is an important risk management task. Deep hedging can solve such hedging problems by training neural network policies in realistic simulated mar...

Generating realistic financial time series is challenging as training data is often limited to a single historical path. With such scarce data, overfitting is hard to avoid, especially under adversari...