Academic Profile

Statistics

Similar Authors

Papers on arXiv

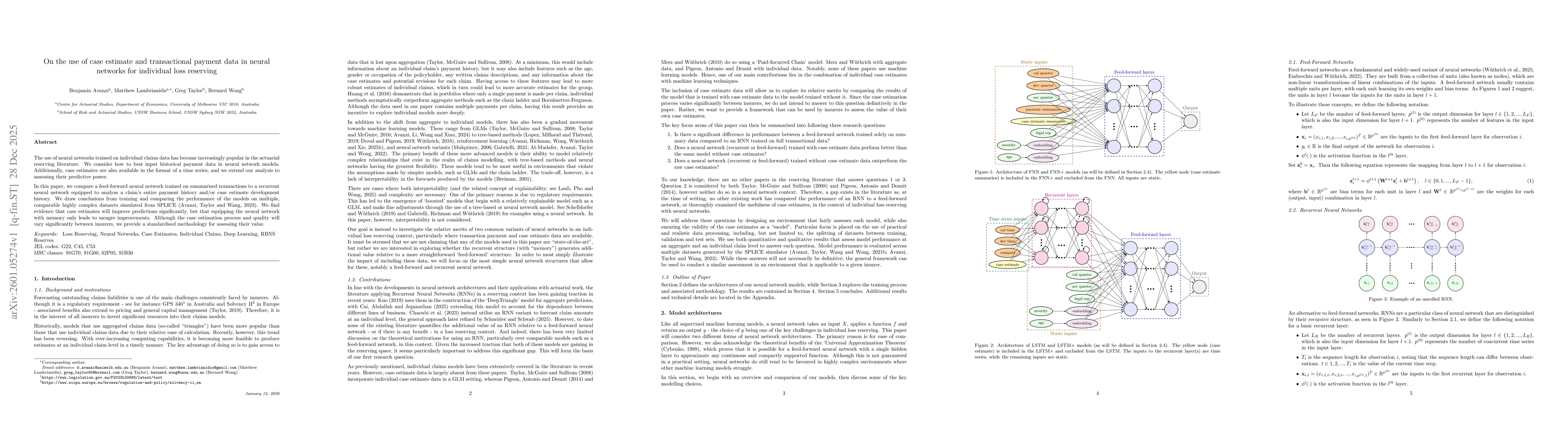

A key task in actuarial modelling involves modelling the distributional properties of losses. Classic (distributional) regression approaches like Generalized Linear Models (GLMs; Nelder and Wedderbu...

A retiree's appetite for risk is a common input into the lifetime utility models that are traditionally used to find optimal strategies for the decumulation of retirement savings. In this work, we...

Understanding the emergence of data breaches is crucial for cyber insurance. However, analyses of data breach frequency trends in the current literature lead to contradictory conclusions. We put for...

High-cardinality categorical features are pervasive in actuarial data (e.g. occupation in commercial property insurance). Standard categorical encoding methods like one-hot encoding are inadequate i...

The optimization criterion for dividends from a risky business is most often formalized in terms of the expected present value of future dividends. That criterion disregards a potential, explicit de...

Loss reserving generally focuses on identifying a single model that can generate superior predictive performance. However, different loss reserving models specialise in capturing different aspects o...

We consider the optimal risk transfer from an insurance company to a reinsurer. The problem formulation considered in this paper is closely connected to the optimal portfolio problem in finance, wit...

In this paper we consider a company whose assets and liabilities evolve according to a correlated bivariate geometric Brownian motion, such as in Gerber and Shiu (2003). We determine what dividend s...

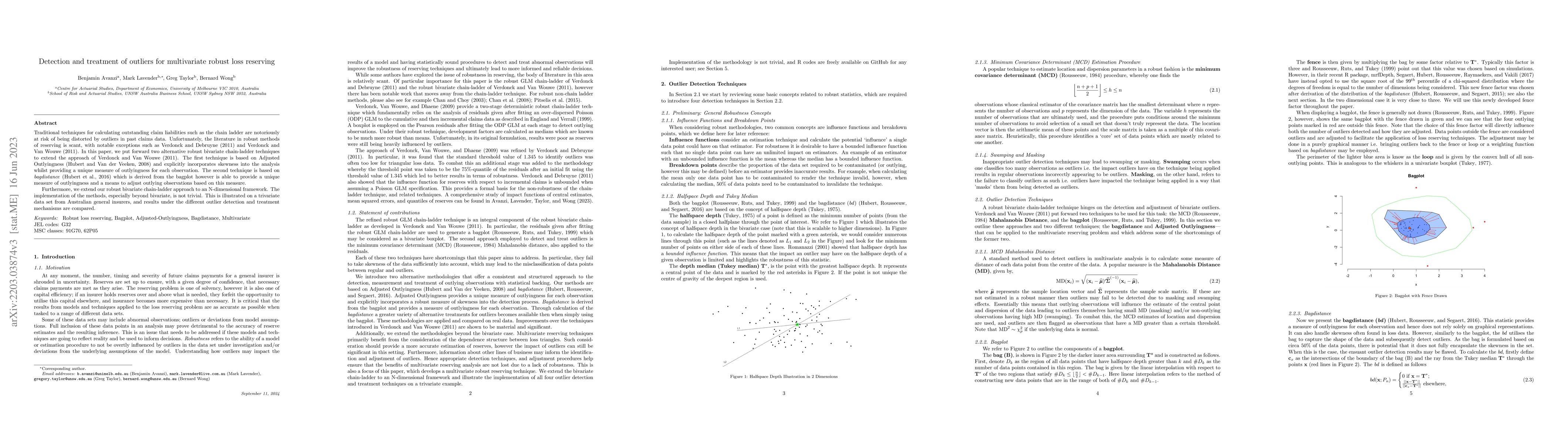

Traditional techniques for calculating outstanding claim liabilities such as the chain ladder are notoriously at risk of being distorted by outliers in past claims data. Unfortunately, the literatur...

The sensitivity of loss reserving techniques to outliers in the data or deviations from model assumptions is a well known challenge. It has been shown that the popular chain-ladder reserving approac...

In this paper, we first introduce a simulator of cases estimates of incurred losses, called `SPLICE` (Synthetic Paid Loss and Incurred Cost Experience). In three modules, case estimates are simulate...

Neural networks offer a versatile, flexible and accurate approach to loss reserving. However, such applications have focused primarily on the (important) problem of fitting accurate central estimate...

Recent years have seen rapid increase in the application of machine learning to insurance loss reserving. They yield most value when applied to large data sets, such as individual claims, or large c...

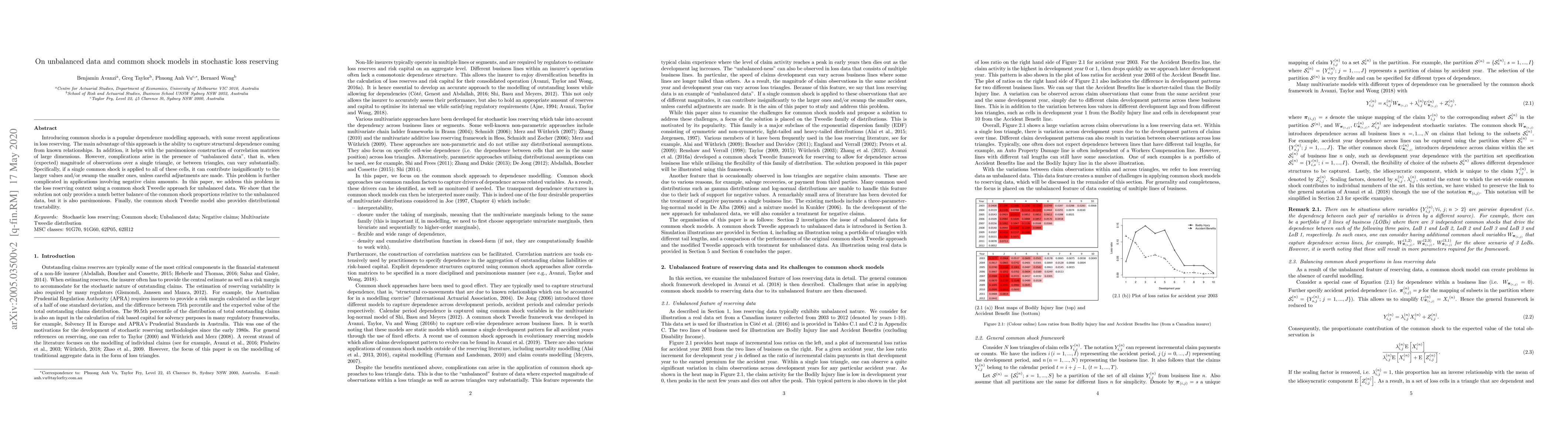

Introducing common shocks is a popular dependence modelling approach, with some recent applications in loss reserving. The main advantage of this approach is the ability to capture structural depend...

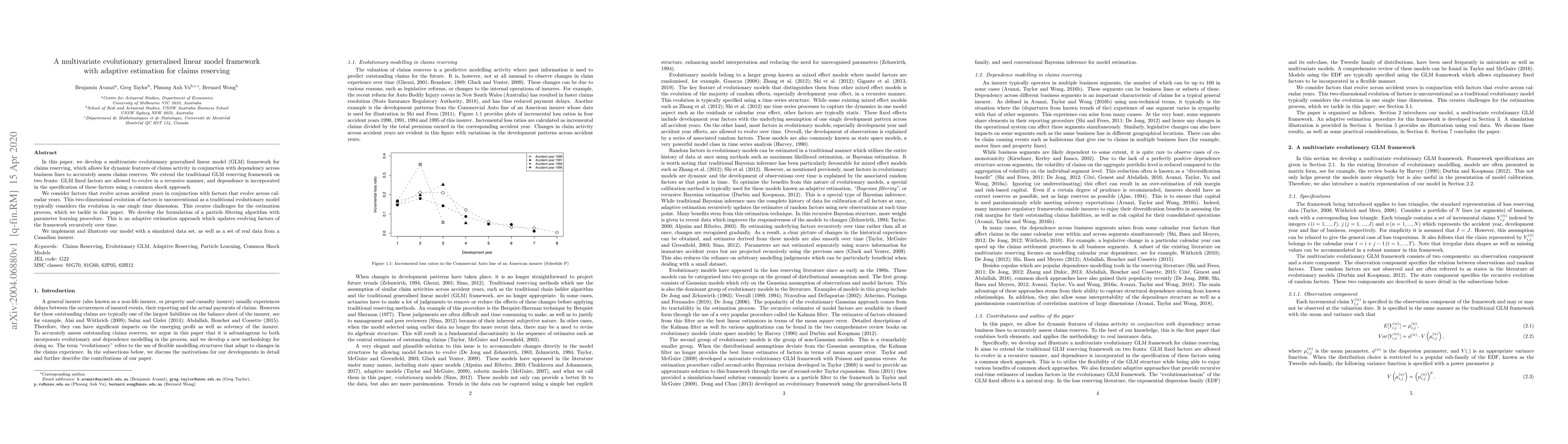

In this paper, we develop a multivariate evolutionary generalised linear model (GLM) framework for claims reserving, which allows for dynamic features of claims activity in conjunction with dependen...

The Central Limit Theorem (CLT) is one of the most fundamental results in statistics. It states that the standardized sample mean of a sequence of $n$ mutually independent and identically distribute...

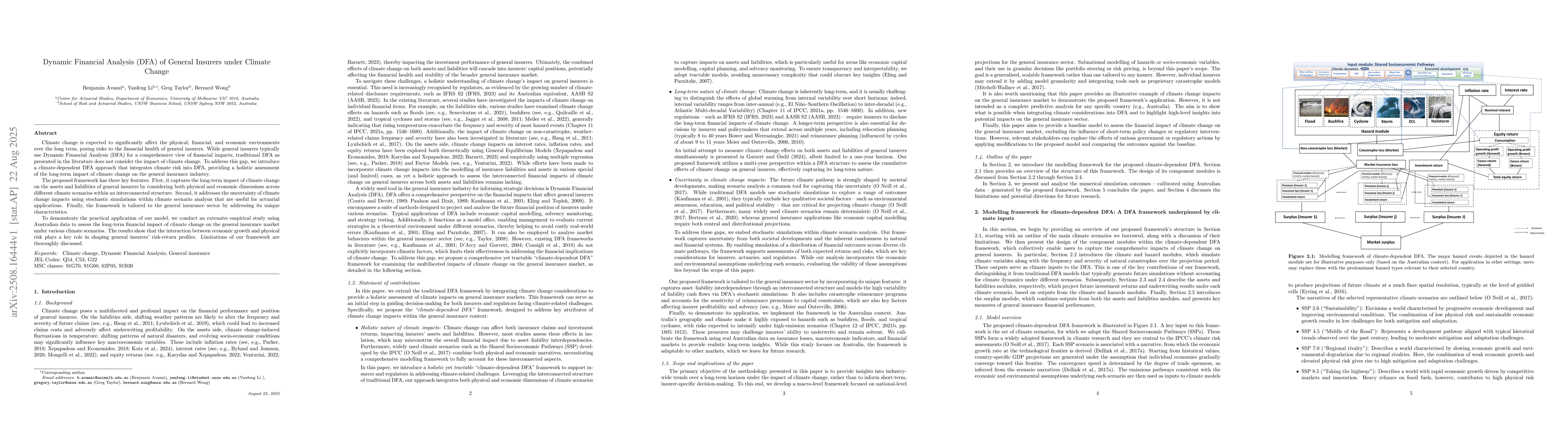

Climate change is expected to significantly affect the physical, financial, and economic environments over the long term, posing risks to the financial health of general insurers. While general insure...

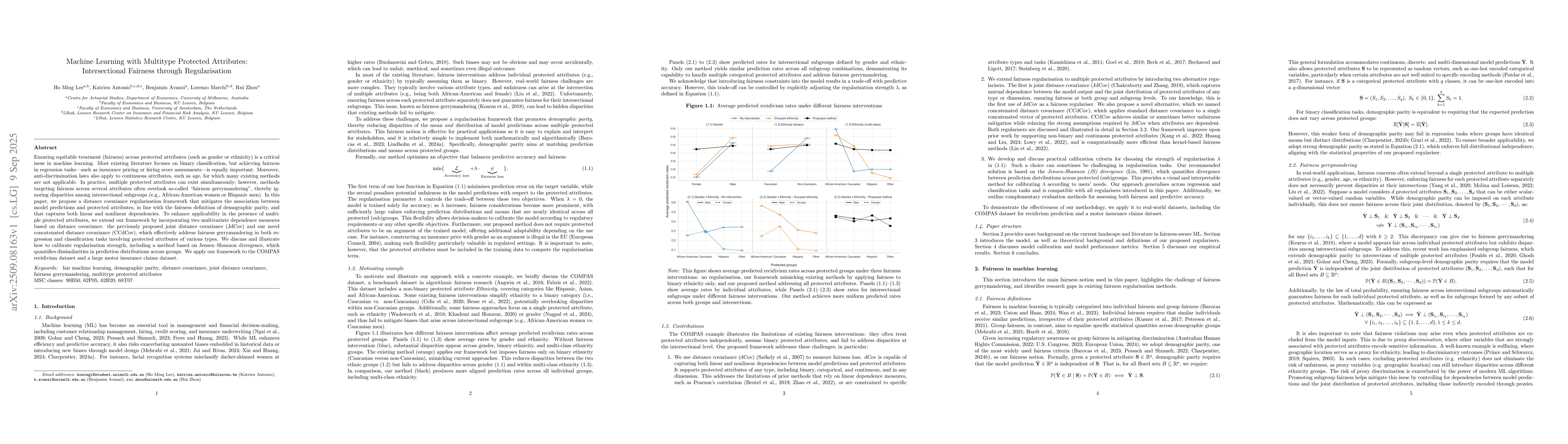

Ensuring equitable treatment (fairness) across protected attributes (such as gender or ethnicity) is a critical issue in machine learning. Most existing literature focuses on binary classification, bu...

In high-risk environments, traditional indemnity insurance is often unaffordable or ineffective, despite its well-known optimality under expected utility. This paper compares excess-of-loss indemnity ...

The use of neural networks trained on individual claims data has become increasingly popular in the actuarial reserving literature. We consider how to best input historical payment data in neural netw...

Outstanding claim liabilities are revised repeatedly as claims develop, yet most modern reserving models are trained as one-shot predictors and typically learn only from settled claims. We formulate i...

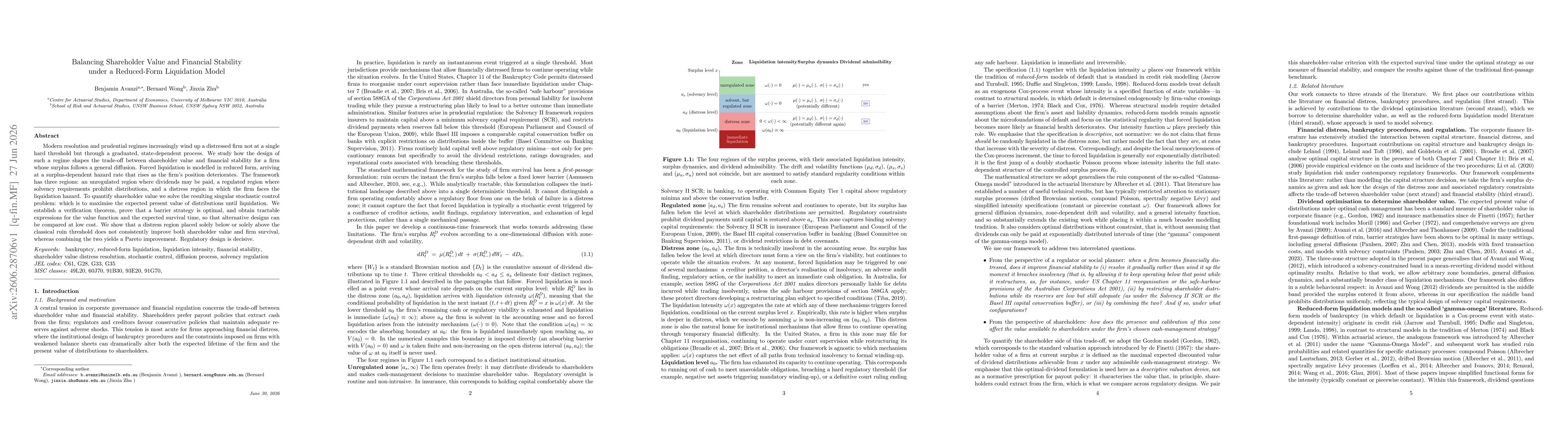

Modern resolution and prudential regimes increasingly wind up a distressed firm not at a single hard threshold but through a graduated, state-dependent process. We study how the design of such a regim...