Academic Profile

Statistics

Similar Authors

Papers on arXiv

In Data Assimilation, observations are fused with simulations to obtain an accurate estimate of the state and parameters for a given physical system. Combining data with a model, however, while accu...

For pricing American options, %after suitable discretization in space and time, a sequence of discrete linear complementarity problems (LCPs) or equivalently Hamilton-Jacobi-Bellman (HJB) equations ...

We are concerned with high-dimensional coupled FBSDE systems approximated by the deep BSDE method of Han et al. (2018). It was shown by Han and Long (2020) that the errors induced by the deep BSDE m...

It is well-known that decision-making problems from stochastic control can be formulated by means of a forward-backward stochastic differential equation (FBSDE). Recently, the authors of Ji et al. 2...

The Crank-Nicolson (CN) method is a well-known time integrator for evolutionary partial differential equations (PDEs) arising in many real-world applications. Since the solution at any time depends ...

In this paper, we propose a machine learning algorithm for time-inconsistent portfolio optimization. The proposed algorithm builds upon neural network based trading schemes, in which the asset alloc...

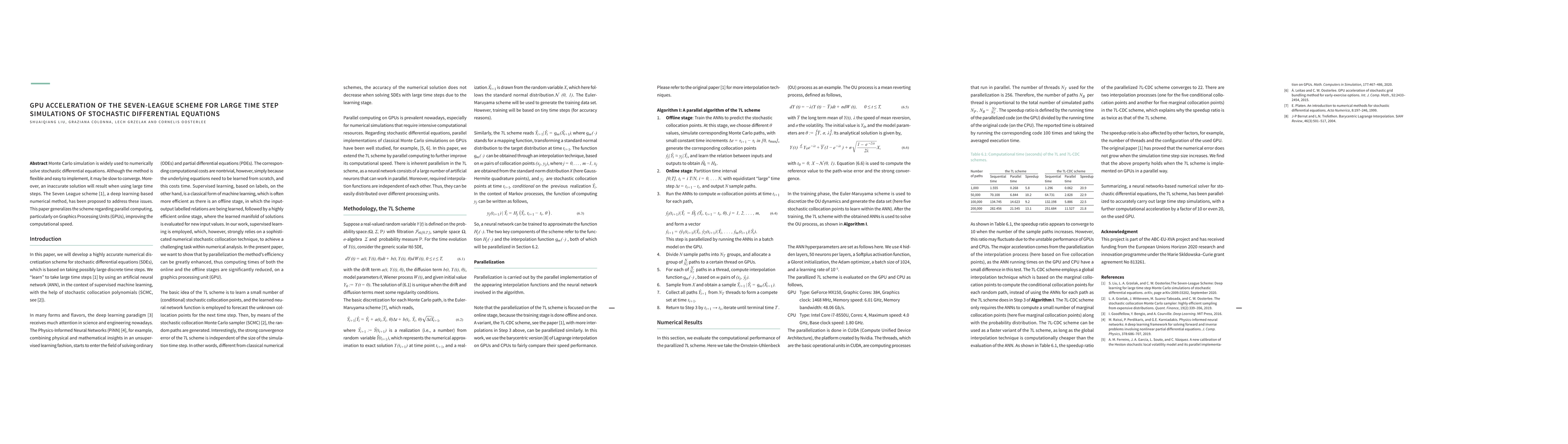

Monte Carlo simulation is widely used to numerically solve stochastic differential equations. Although the method is flexible and easy to implement, it may be slow to converge. Moreover, an inaccura...

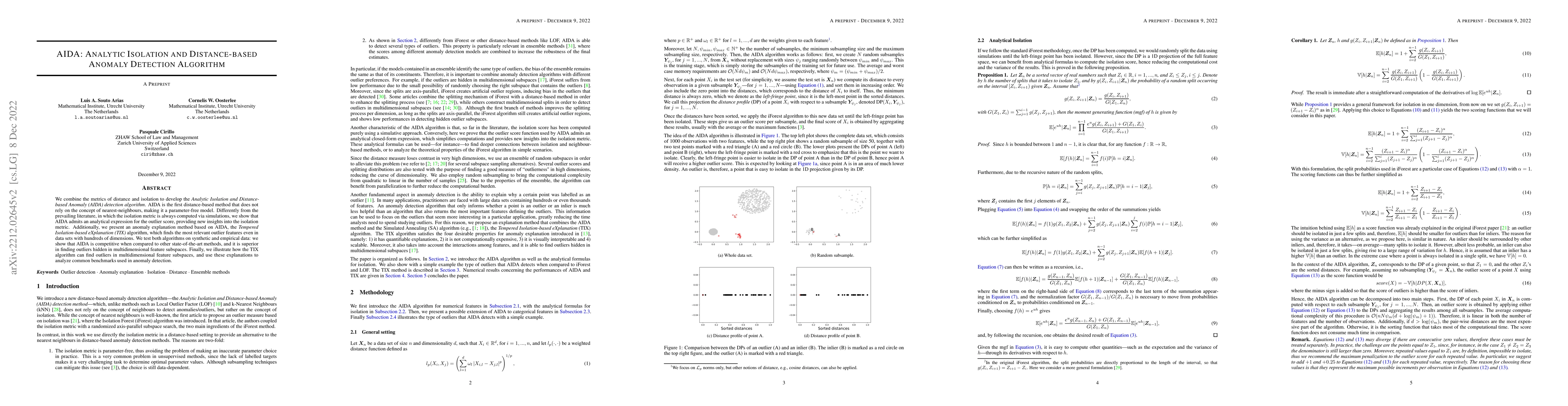

We combine the metrics of distance and isolation to develop the Analytic Isolation and Distance-based Anomaly (AIDA) detection algorithm. AIDA is the first distance-based method that does not rely o...

We propose a new jump-diffusion process, the Heston-Queue-Hawkes (HQH) model, combining the well-known Heston model and the recently introduced Queue-Hawkes (Q-Hawkes) jump process. Like the Hawkes ...

In this paper, we will evaluate integrals that define the conditional expectation, variance and characteristic function of stochastic processes with respect to fractional Brownian motion (fBm) for a...

In this paper, we propose a deep learning based numerical scheme for strongly coupled FBSDEs, stemming from stochastic control. It is a modification of the deep BSDE method in which the initial valu...

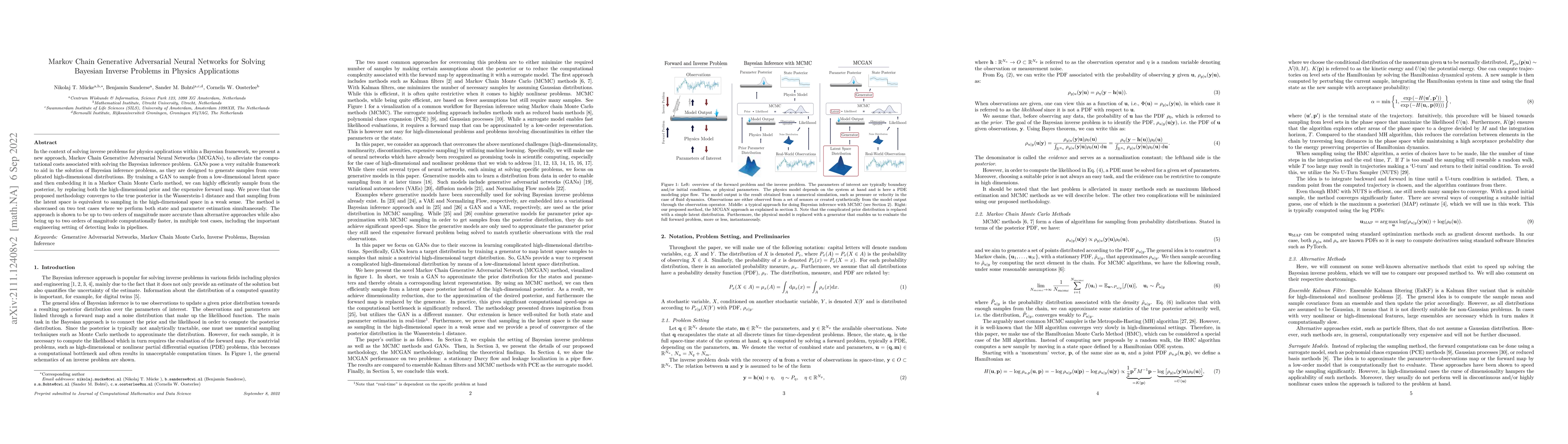

In the context of solving inverse problems for physics applications within a Bayesian framework, we present a new approach, Markov Chain Generative Adversarial Neural Networks (MCGANs), to alleviate...

A novel discretization is presented for forward-backward stochastic differential equations (FBSDE) with differentiable coefficients, simultaneously solving the BSDE and its Malliavin sensitivity pro...

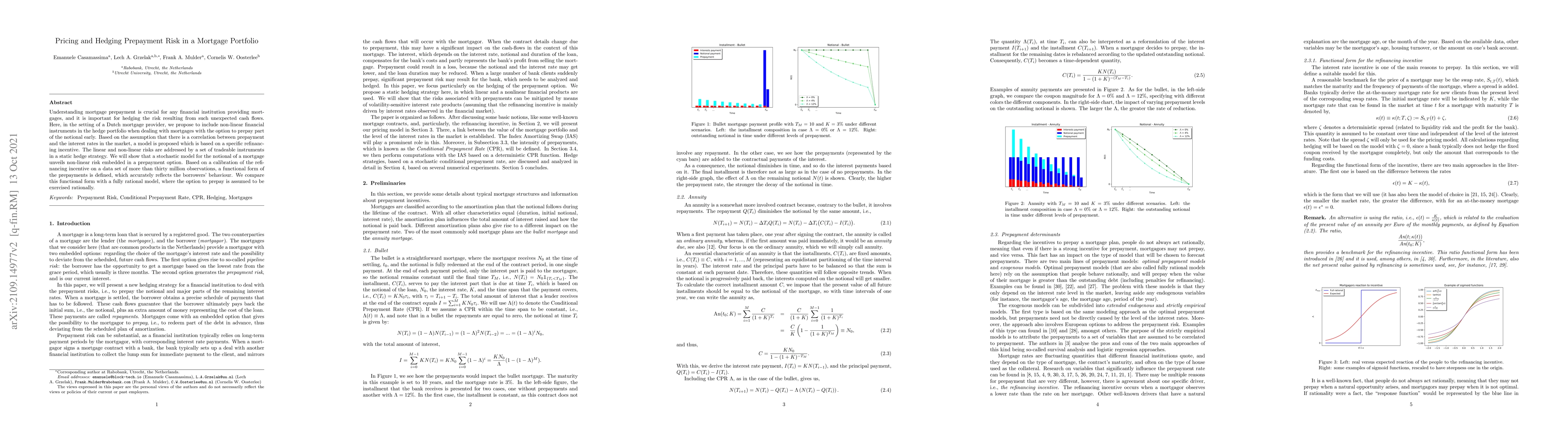

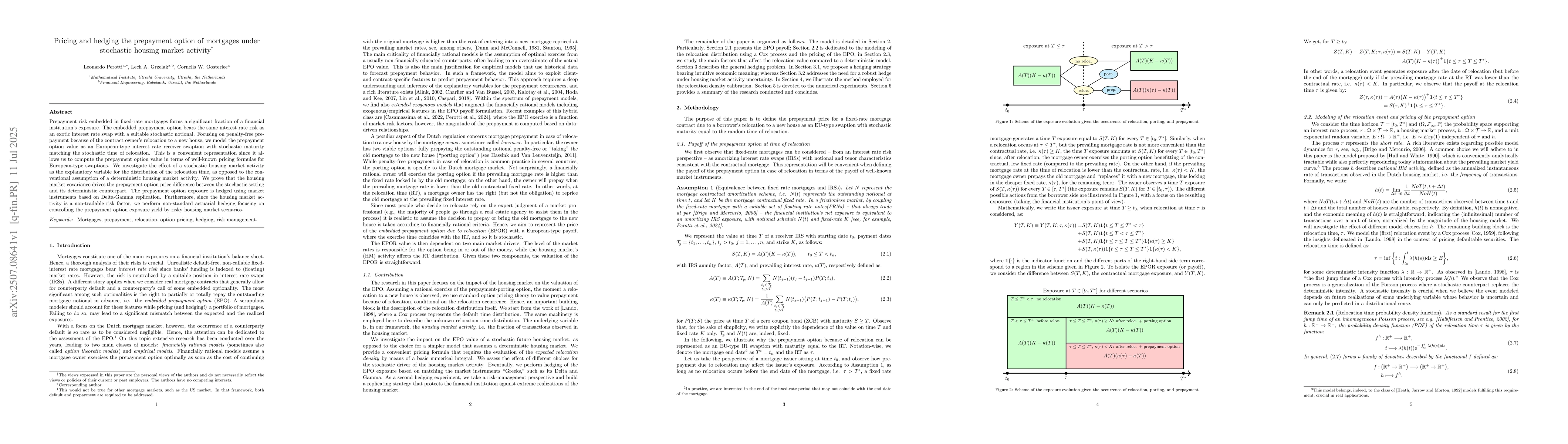

Understanding mortgage prepayment is crucial for any financial institution providing mortgages, and it is important for hedging the risk resulting from such unexpected cash flows. Here, in the setti...

This paper presents how to apply the stochastic collocation technique to assets that can not move below a boundary. It shows that the polynomial collocation towards a lognormal distribution does not...

Generative adversarial networks (GANs) have shown promising results when applied on partial differential equations and financial time series generation. We investigate if GANs can also be used to ap...

Storage of electricity has become increasingly important, due to the gradual replacement of fossil fuels by more variable and uncertain renewable energy sources. In this paper, we provide details on...

We present a novel reduced order model (ROM) approach for parameterized time-dependent PDEs based on modern learning. The ROM is suitable for multi-query problems and is nonintrusive. It is divided ...

In this paper, we propose a neural network-based method for CVA computations of a portfolio of derivatives. In particular, we focus on portfolios consisting of a combination of derivatives, with and...

In this paper, we propose third-order semi-discretized schemes in space based on the tempered weighted and shifted Gr\"unwald difference (tempered-WSGD) operators for the tempered fractional diffusi...

Artificial neural networks (ANNs) have recently also been applied to solve partial differential equations (PDEs). In this work, the classical problem of pricing European and American financial optio...

Extracting implied information, like volatility and/or dividend, from observed option prices is a challenging task when dealing with American options, because of the computational costs needed to so...

In this article, we combine a lattice sequence from Quasi-Monte Carlo rules with the philosophy of the Fourier-cosine method to design an approximation scheme for expectation computation. We study t...

Various valuation adjustments, or XVAs, can be written in terms of non-linear PIDEs equivalent to FBSDEs. In this paper we develop a Fourier-based method for solving FBSDEs in order to efficiently a...

A data-driven approach called CaNN (Calibration Neural Network) is proposed to calibrate financial asset price models using an Artificial Neural Network (ANN). Determining optimal values of the mode...

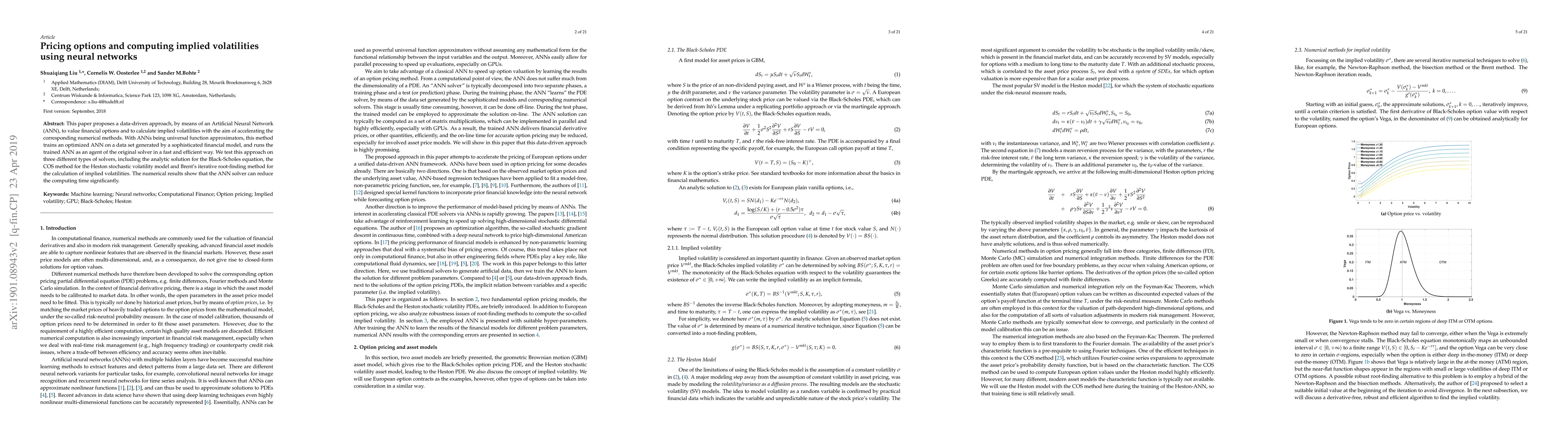

This paper proposes a data-driven approach, by means of an Artificial Neural Network (ANN), to value financial options and to calculate implied volatilities with the aim of accelerating the correspo...

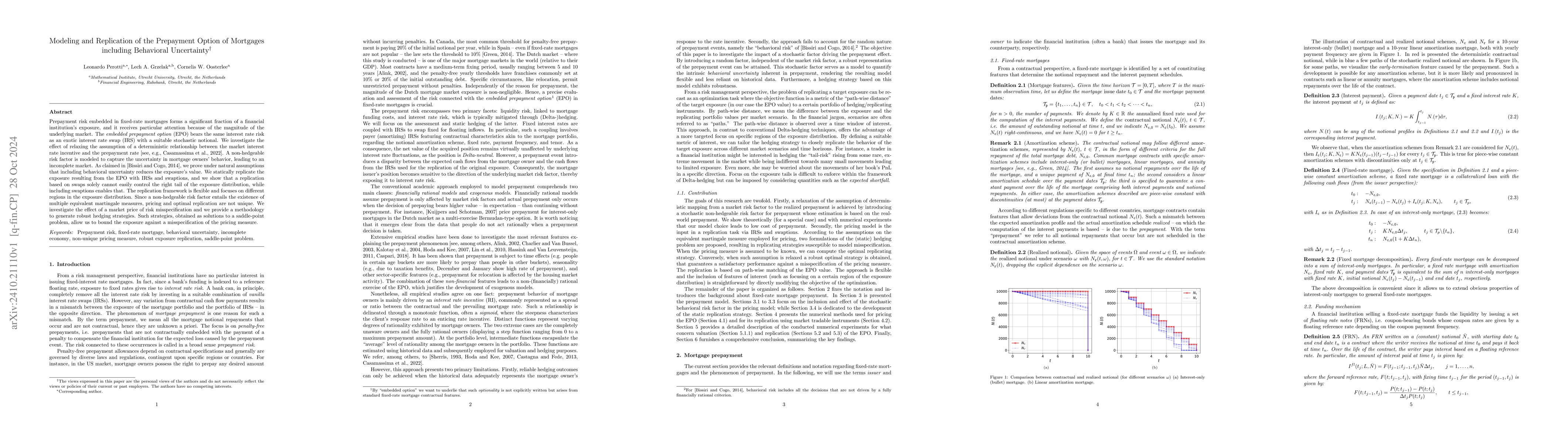

Prepayment risk embedded in fixed-rate mortgages forms a significant fraction of a financial institution's exposure, and it receives particular attention because of the magnitude of the underlying mar...

A higher-order numerical method is presented for scalar valued, coupled forward-backward stochastic differential equations. Unlike most classical references, the forward component is not only discreti...

A deep BSDE approach is presented for the pricing and delta-gamma hedging of high-dimensional Bermudan options, with applications in portfolio risk management. Large portfolios of a mixture of multi-a...

We introduce the deep multi-FBSDE method for robust approximation of coupled forward-backward stochastic differential equations (FBSDEs), focusing on cases where the deep BSDE method of Han, Jentzen, ...

In this paper, we investigate the Markovian iteration method for solving coupled forward-backward stochastic differential equations (FBSDEs) featuring a fully coupled forward drift, meaning the drift ...

Prepayment risk embedded in fixed-rate mortgages forms a significant fraction of a financial institution's exposure. The embedded prepayment option bears the same interest rate risk as an exotic inter...

Stochastic differential equations (SDEs) driven by fractional Brownian motion (fBm) are increasingly used to model systems with rough dynamics and long-range dependence, such as those arising in quant...

We propose the Compound BSDE method, a fully forward, deep-learning-based approach for solving a broad class of problems in financial mathematics, including optimal stopping. The method is based on a ...

We introduce a damped variant of the Shannon Wavelet Inverse Fourier Technique (SWIFT) for pricing European options when the characteristic function of the underlying model is available. The key idea ...

We develop an analytic Fourier cosine (COS) method for the valuation of compound options. By deriving closed-form expressions for the cosine coefficients at all compound stages, the proposed method el...

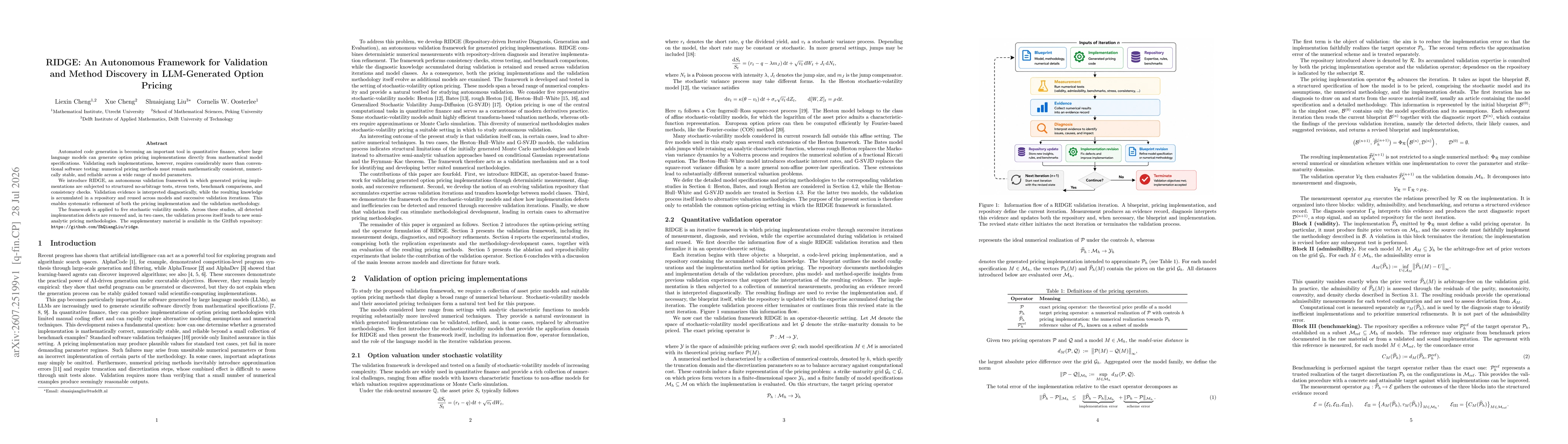

Automated code generation is becoming an important tool in quantitative finance, where large language models can generate option pricing implementations directly from mathematical model specifications...