Academic Profile

Statistics

Similar Authors

Papers on arXiv

Affine Diffusion dynamics are frequently used for Valuation Adjustments (xVA) calculations due to their analytic tractability. However, these models cannot capture the market-implied skew and smile,...

We introduce a class of copulas that we call Principal Component Copulas. This class intends to combine the strong points of copula-based techniques with principal component-based models, which resu...

In this paper we present a complete framework for the energy-stable simulation of stratified incompressible flow in channels, using the one-dimensional two-fluid model. Building on earlier energy-co...

Wrong-Way Risk (WWR) is an important component in Funding Valuation Adjustment (FVA) modelling. Yet, the standard assumption is independence between market risks and the counterparty defaults and fu...

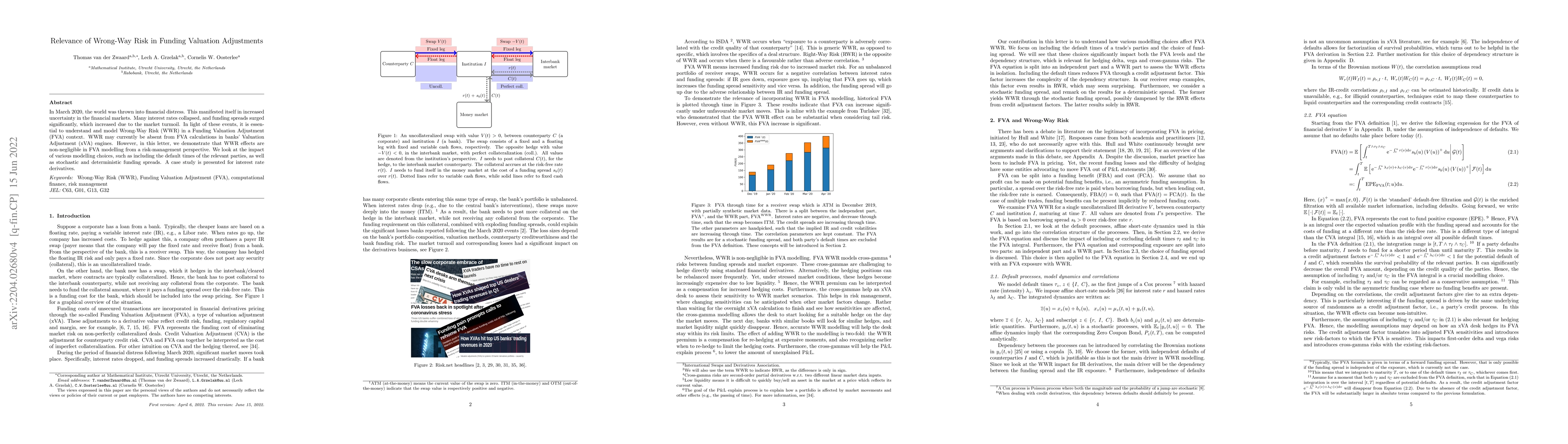

In March 2020, the world was thrown into financial distress. This manifested itself in increased uncertainty in the financial markets. Many interest rates collapsed, and funding spreads surged signi...

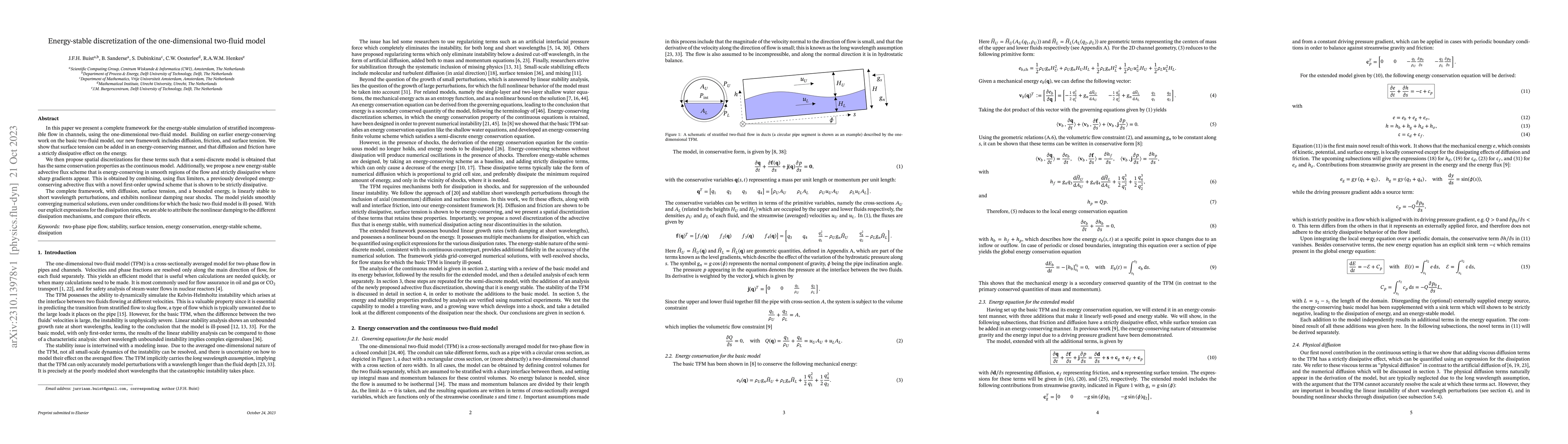

We show that the one-dimensional (1D) two-fluid model (TFM) for stratified flow in channels and pipes (in its incompressible, isothermal form) satisfies an energy conservation equation, which arises...

In this work, we consider rule-based investment strategies for managing a defined contribution saving scheme under the Dutch pension fund testing model. We found that dynamic rule-based investment c...

This study contributes to understanding Valuation Adjustments (xVA) by focussing on the dynamic hedging of Credit Valuation Adjustment (CVA), corresponding Profit & Loss (P&L) and the P&L explain. T...