Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce a novel class of credit risk models in which the drift of the survival process of a firm is a linear function of the factors. The prices of defaultable bonds and credit default swaps (C...

We propose a function-learning methodology with a control-theoretical foundation. We parametrise the approximating function as the solution to a control system on a reproducing-kernel Hilbert space,...

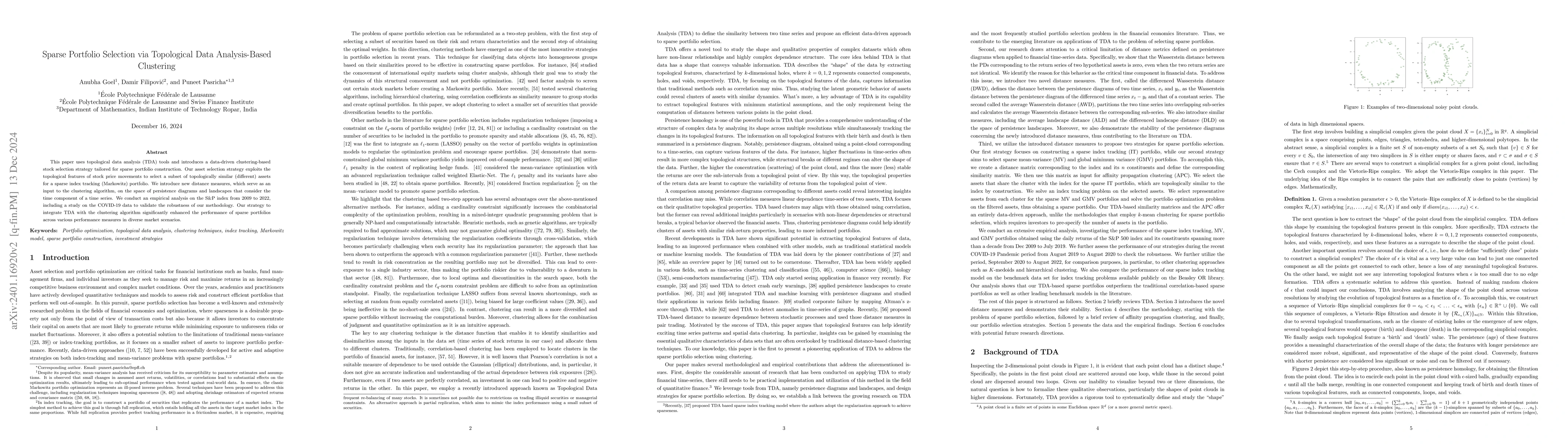

This paper uses topological data analysis (TDA) tools and introduces a data-driven clustering-based stock selection strategy tailored for sparse portfolio construction. Our asset selection strategy ...

We introduce an ensemble learning method based on Gaussian Process Regression (GPR) for predicting conditional expected stock returns given stock-level and macro-economic information. Our ensemble l...

We introduce an ensemble learning method for dynamic portfolio valuation and risk management building on regression trees. We learn the dynamic value process of a derivative portfolio from a finite ...

We introduce a universal framework for mean-covariance robust risk measurement and portfolio optimization. We model uncertainty in terms of the Gelbrich distance on the mean-covariance space, along ...

This study deals with the pricing and hedging of single-tranche collateralized debt obligations (STCDOs). We specify an affine two-factor model in which a catastrophic risk component is incorporated...

We present a general framework for portfolio risk management in discrete time, based on a replicating martingale. This martingale is learned from a finite sample in a supervised setting. The model l...

We propose a methodology for computing single and multi-asset European option prices, and more generally expectations of scalar functions of (multivariate) random variables. This new approach combin...

L\'evy driven term structure models have become an important subject in the mathematical finance literature. This paper provides a comprehensive analysis of the L\'evy driven Heath-Jarrow-Morton typ...

Over the last decade, dividends have become a standalone asset class instead of a mere side product of an equity investment. We introduce a framework based on polynomial jump-diffusions to jointly p...

We develop a comprehensive mathematical framework for polynomial jump-diffusions in a semimartingale context, which nest affine jump-diffusions and have broad applications in finance. We show that t...

We study discretizations of polynomial processes using finite state Markov processes satisfying suitable moment matching conditions. The states of these Markov processes together with their transiti...

This paper investigates theoretical and methodological foundations for stochastic optimal control (SOC) in discrete time. We start formulating the control problem in a general dynamic programming fram...

This paper develops a model-free framework for static fixed-income pricing and the replication of liability cash flows. We show that the absence of static arbitrage across a universe of fixed-income i...