Academic Profile

Statistics

Similar Authors

Papers on arXiv

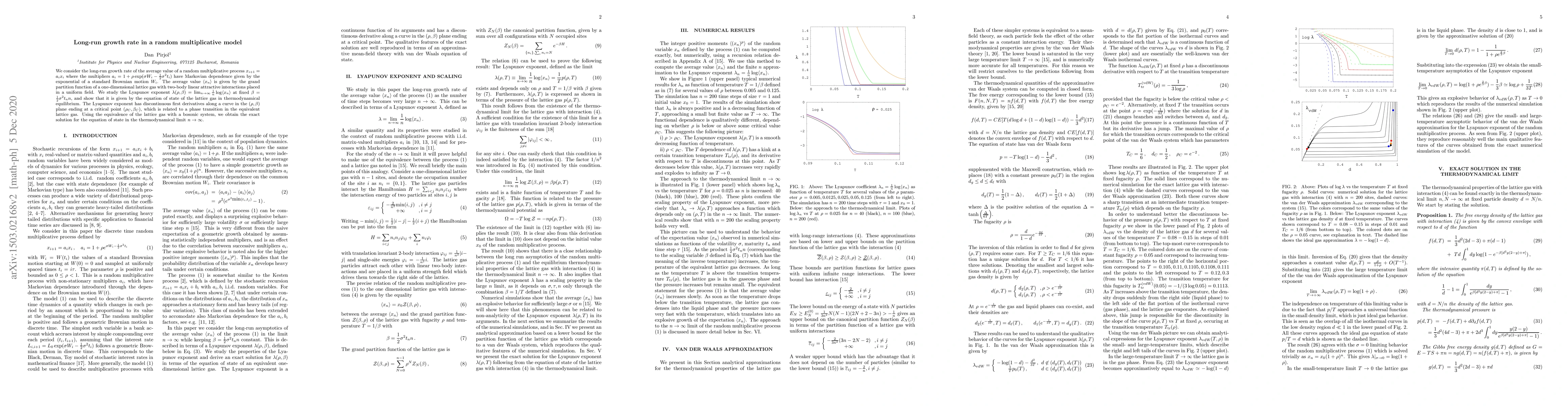

We consider the long-run growth rate of the average value of a random multiplicative process $x_{i+1} = a_i x_i$ where the multipliers $a_i=1+\rho\exp(\sigma W_i - \frac12 \sigma^2 t_i)$ have Markov...

We derive the short-maturity asymptotics for option prices in the local volatility model in a new short-maturity limit $T\to 0$ at fixed $\rho = (r-q) T$, where $r$ is the interest rate and $q$ is t...

We present a study of the short maturity asymptotics for Asian options in a jump-diffusion model with a local volatility component, where the jumps are modeled as a compound Poisson process. The ana...

We present an asymptotic result for the Laplace transform of the time integral of the geometric Brownian motion $F(\theta,T) = \mathbb{E}[e^{-\theta X_T}]$ with $X_T = \int_0^T e^{\sigma W_s + ( a -...

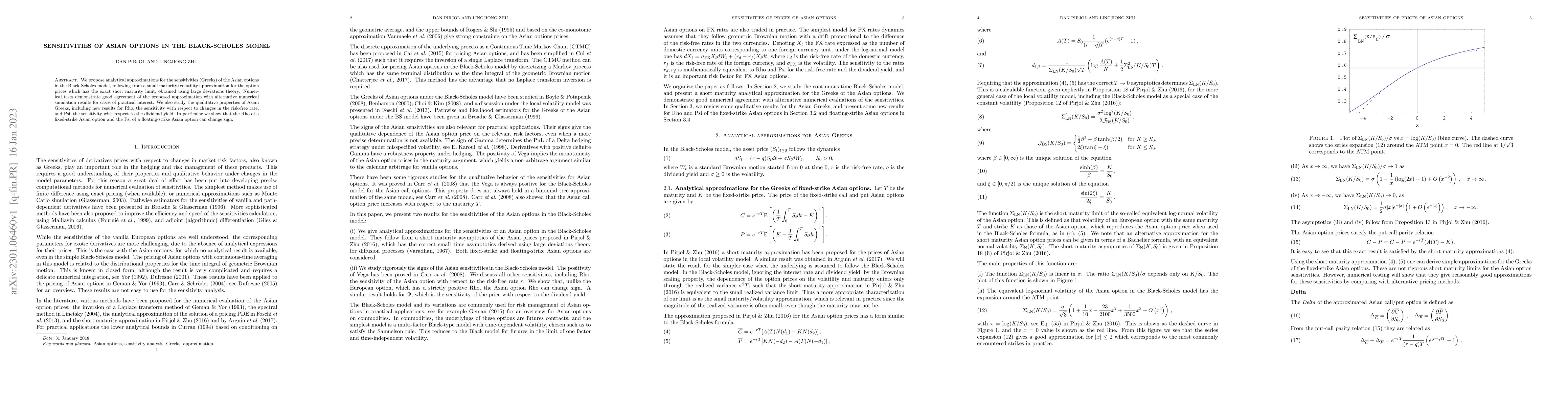

We propose analytical approximations for the sensitivities (Greeks) of the Asian options in the Black-Scholes model, following from a small maturity/volatility approximation for the option prices wh...

We study the numerical evaluation of several functions appearing in the small time expansion of the distribution of the time-integral of the geometric Brownian motion as well as its joint distributi...

We study the stochastic growth process in discrete time $x_{i+1} = (1 + \mu_i) x_i$ with growth rate $\mu_i = \rho e^{Z_i - \frac12 var(Z_i)}$ proportional to the exponential of an Ornstein-Uhlenbec...

The Hartman-Watson distribution with density $f_r(t)$ is a probability distribution defined on $t \geq 0$ which appears in several problems of applied probability. The density of this distribution i...

We study the explosion of the solutions of the SDE in the quasi-Gaussian HJM model with a CEV-type volatility. The quasi-Gaussian HJM models are a popular approach for modeling the dynamics of the y...

Quasi-Gaussian HJM models are a popular approach for modeling the dynamics of the yield curve. This is due to their low dimensional Markovian representation, which greatly simplifies their numerical...

We study the short maturity asymptotics for prices of forward start Asian options under the assumption that the underlying asset follows a local volatility model. We obtain asymptotics for the cases...

The short maturity limit $T\to 0$ for the implied volatility of an Asian option in the Black-Scholes model is determined by the large deviations property for the time-average of the geometric Brownian...

We derive the short-maturity asymptotics for prices of options on realized variance in local-stochastic volatility models. We consider separately the short-maturity asymptotics for out-of-the-money an...

We derive the short-maturity asymptotics for Asian option prices in local-stochastic volatility (LSV) models. Both out-of-the-money (OTM) and at-the-money (ATM) asymptotics are considered. Using large...

We derive the short-maturity asymptotics for European and VIX option prices in local-stochastic volatility models where the volatility follows a continuous-path Markov process. Both out-of-the-money (...

We study the pricing of VIX options in the SABR model $dS_t = \sigma_t S_t^\beta dB_t, d\sigma_t = \omega \sigma_t dZ_t$ where $B_t,Z_t$ are standard Brownian motions correlated with correlation $\rho...

This note gives a bound on the error of the leading term of the $t\to 0$ asymptotic expansion of the Hartman-Watson distribution $\theta(r,t)$ in the regime $rt=\rho$ constant. The leading order term ...

We present a study of the short-maturity asymptotics for VIX and European option prices in local-stochastic volatility models with compound Poisson jumps. Both out-of-the-money (OTM) and at-the-money ...

We present a study of the leading-order asymptotics for VIX option prices in Bergomi models in the short-maturity and small volatility-of-volatility regimes. Both out-of-the-money (OTM) and at-the-mon...