Academic Profile

Statistics

Similar Authors

Papers on arXiv

Unimodular sequences with low autocorrelations are desired in many applications, especially in the area of radar and code-division multiple access (CDMA). In this paper, we propose a new algorithm t...

This paper introduces Polynomial Graphical Lasso (PGL), a new approach to learning graph structures from nodal signals. Our key contribution lies in modeling the signals as Gaussian and stationary o...

Algorithms that ensure reproducible findings from large-scale, high-dimensional data are pivotal in numerous signal processing applications. In recent years, multivariate false discovery rate (FDR) ...

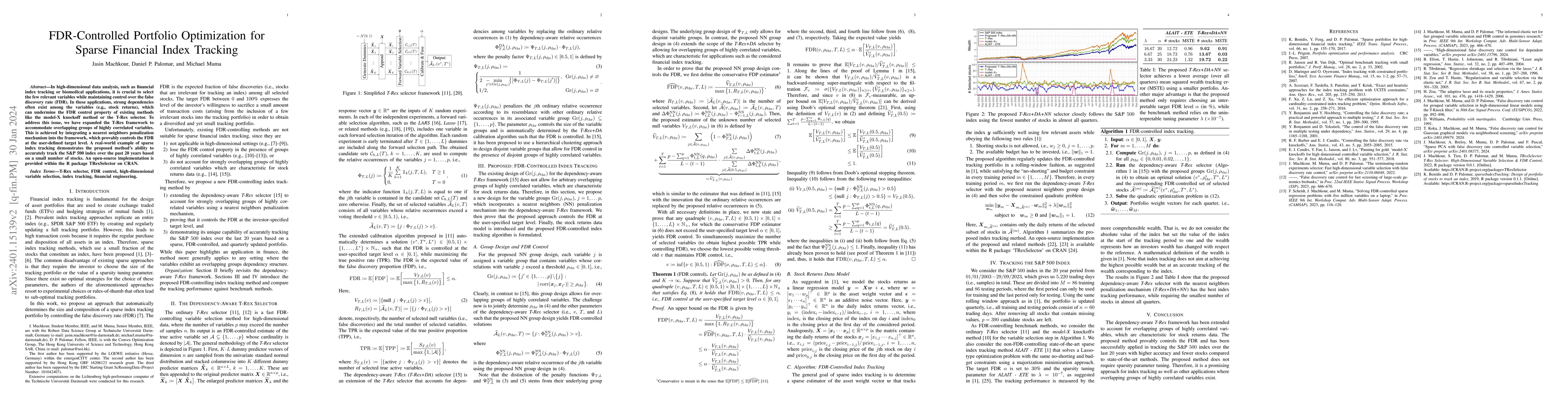

In high-dimensional data analysis, such as financial index tracking or biomedical applications, it is crucial to select the few relevant variables while maintaining control over the false discovery ...

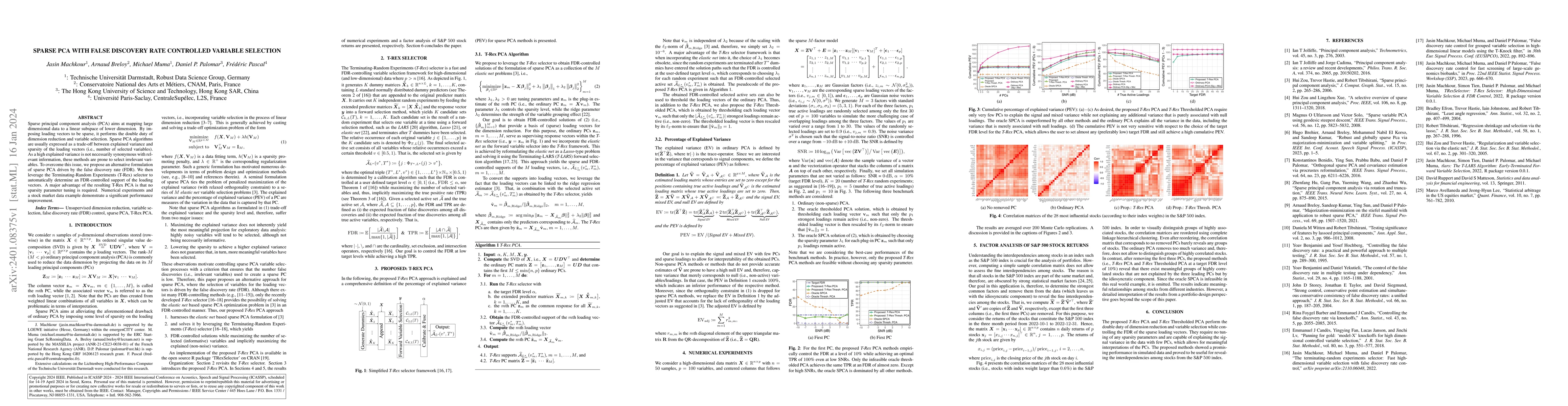

Sparse principal component analysis (PCA) aims at mapping large dimensional data to a linear subspace of lower dimension. By imposing loading vectors to be sparse, it performs the double duty of dim...

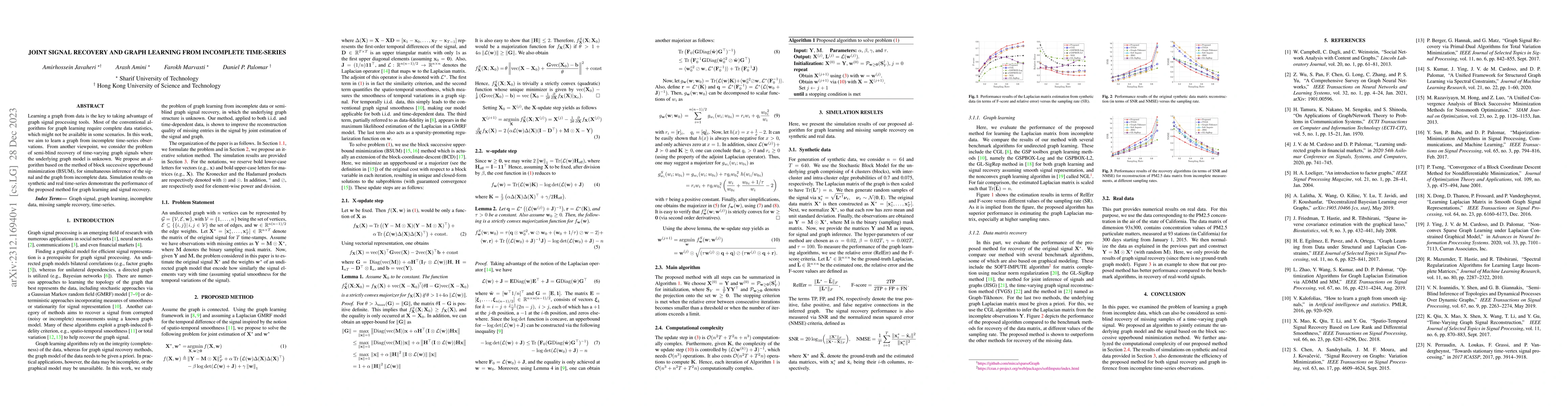

Learning a graph from data is the key to taking advantage of graph signal processing tools. Most of the conventional algorithms for graph learning require complete data statistics, which might not b...

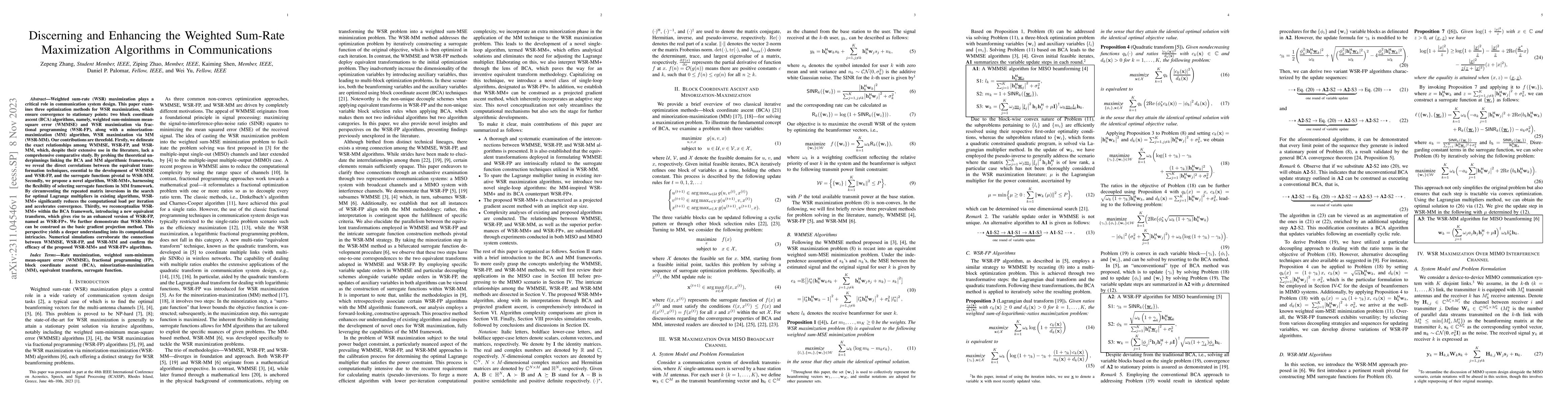

Weighted sum-rate (WSR) maximization plays a critical role in communication system design. This paper examines three optimization methods for WSR maximization, which ensure convergence to stationary...

This paper studies the problem of learning the large-scale Gaussian graphical models that are multivariate totally positive of order two ($\text{MTP}_2$). By introducing the concept of bridge, which...

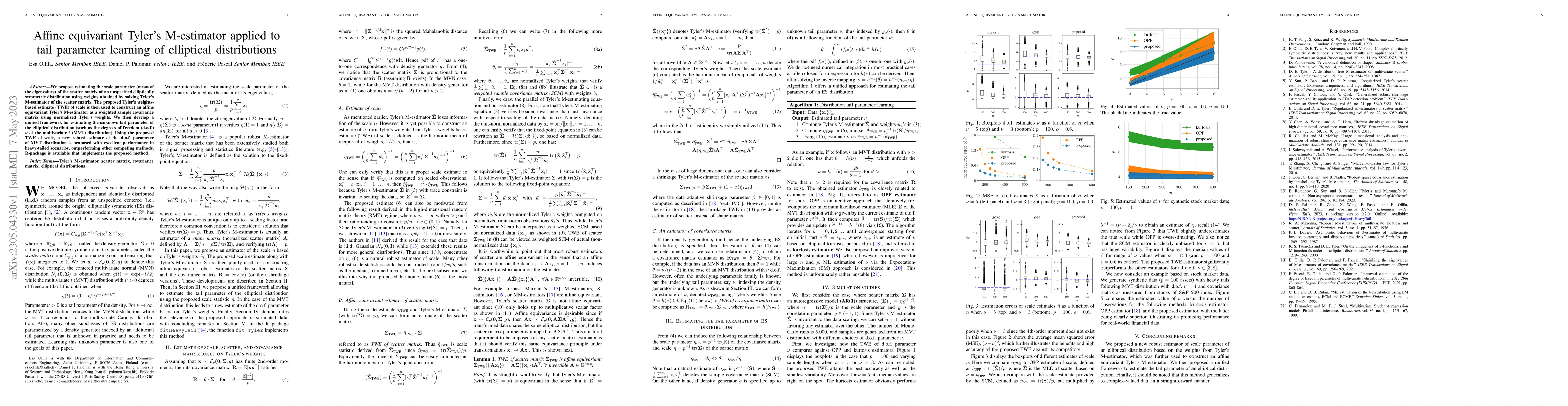

We propose estimating the scale parameter (mean of the eigenvalues) of the scatter matrix of an unspecified elliptically symmetric distribution using weights obtained by solving Tyler's M-estimator ...

The mean and variance of portfolio returns are the standard quantities to measure the expected return and risk of a portfolio. Efficient portfolios that provide optimal trade-offs between mean and v...

We consider the problem of estimating (diagonally dominant) M-matrices as precision matrices in Gaussian graphical models. These models exhibit intriguing properties, such as the existence of the ma...

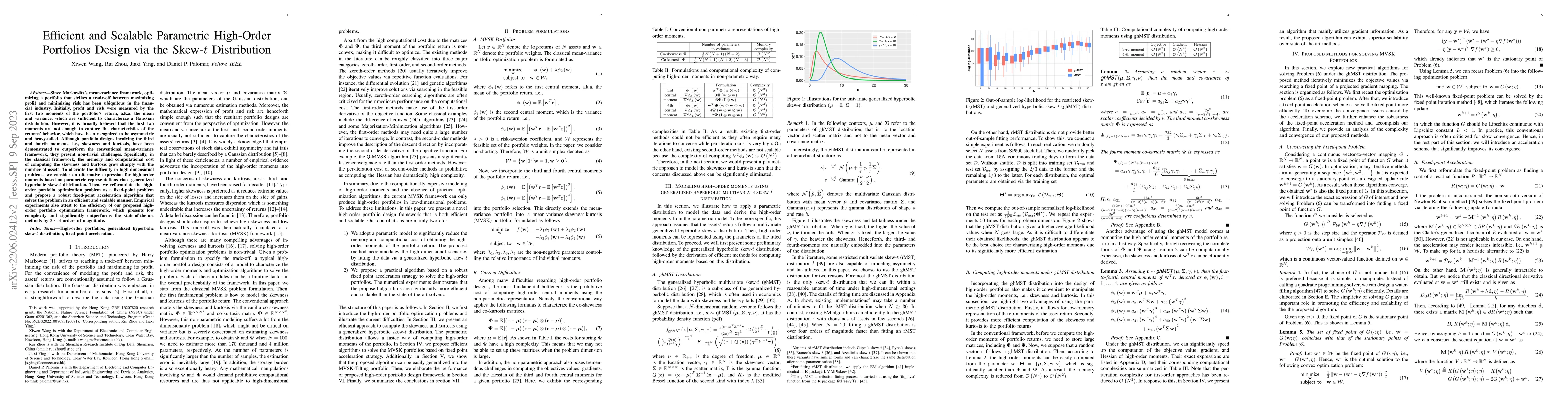

Since Markowitz's mean-variance framework, optimizing a portfolio that maximizes the profit and minimizes the risk has been ubiquitous in the financial industry. Initially, profit and risk were meas...

We study the problem of estimating precision matrices in Gaussian distributions that are multivariate totally positive of order two ($\mathrm{MTP}_2$). The precision matrix in such a distribution is...

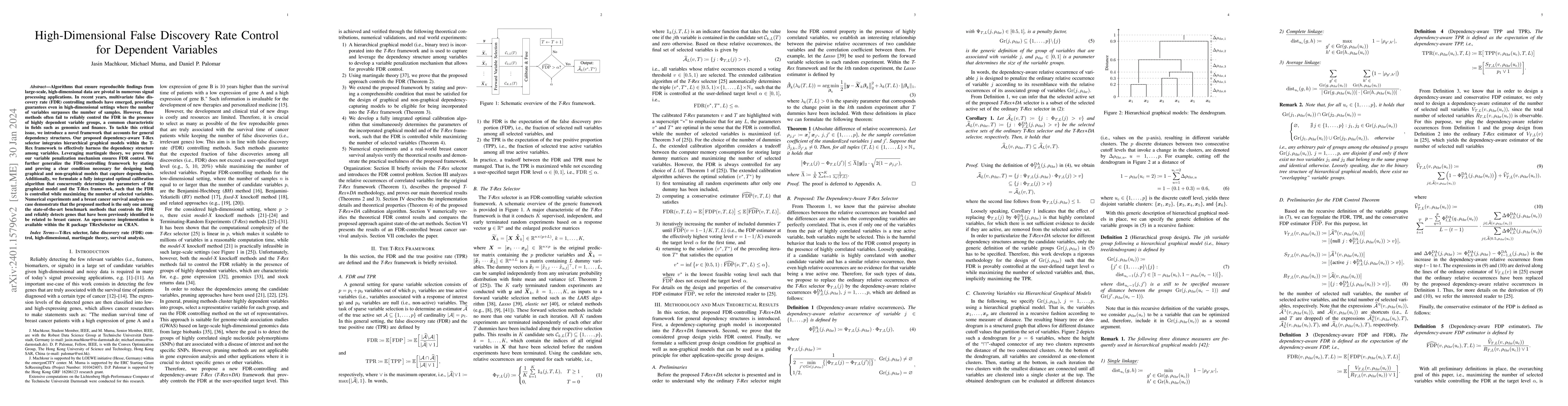

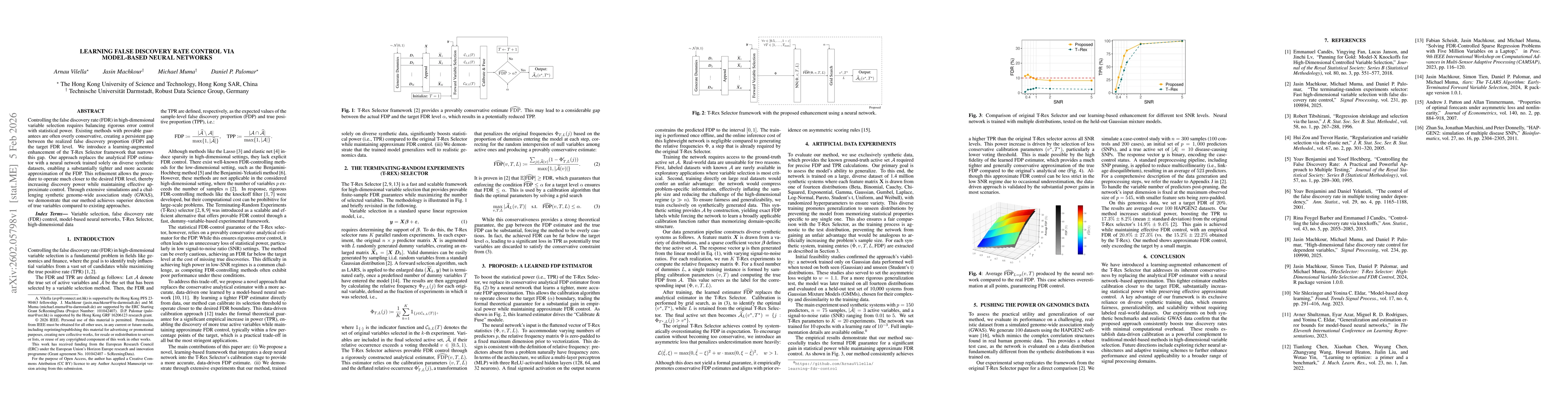

We propose the Terminating-Random Experiments (T-Rex) selector, a fast variable selection method for high-dimensional data. The T-Rex selector controls a user-defined target false discovery rate (FD...

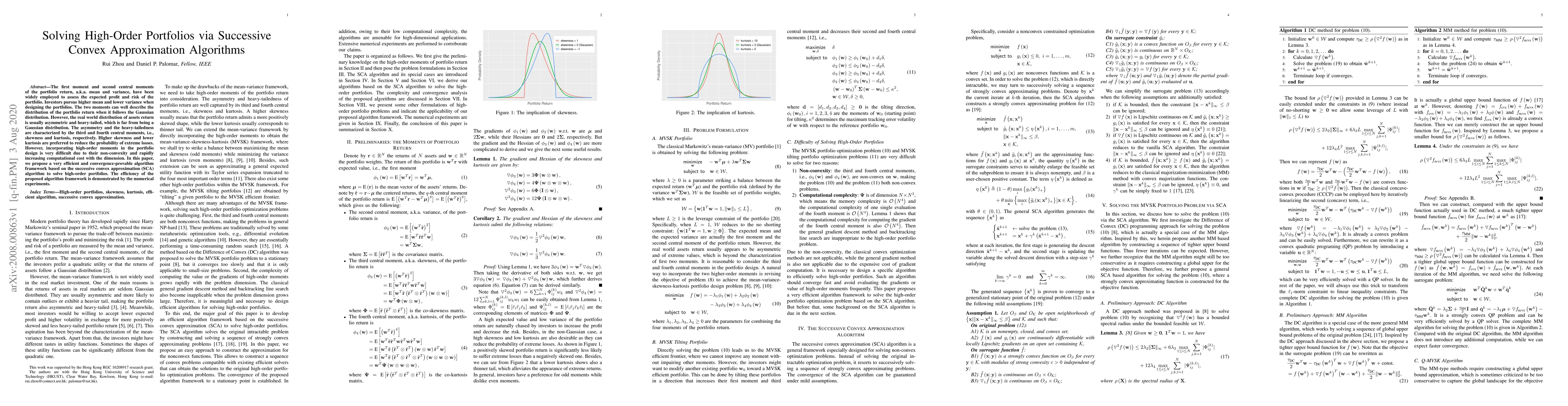

The first moment and second central moments of the portfolio return, a.k.a. mean and variance, have been widely employed to assess the expected profit and risk of the portfolio. Investors pursue hig...

We consider the problem of learning a sparse graph under the Laplacian constrained Gaussian graphical models. This problem can be formulated as a penalized maximum likelihood estimation of the Lapla...

A highly popular regularized (shrinkage) covariance matrix estimator is the shrinkage sample covariance matrix (SCM) which shares the same set of eigenvectors as the SCM but shrinks its eigenvalues ...

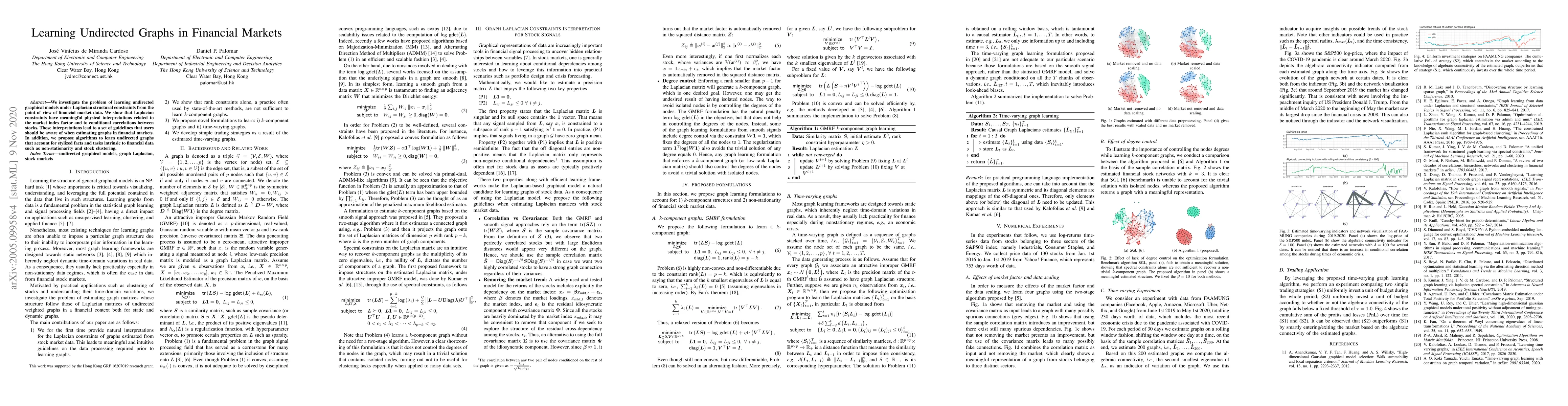

We investigate the problem of learning undirected graphical models under Laplacian structural constraints from the point of view of financial market data. We show that Laplacian constraints have mea...

A popular regularized (shrinkage) covariance estimator is the shrinkage sample covariance matrix (SCM) which shares the same set of eigenvectors as the SCM but shrinks its eigenvalues toward its gra...

This paper considers the problem of robustly estimating the parameters of a heavy-tailed multivariate distribution when the covariance matrix is known to have the structure of a low-rank matrix plus...

Learning a graph with a specific structure is essential for interpretability and identification of the relationships among data. It is well known that structured graph learning from observed samples...

In this two-part work, we propose an algorithmic framework for solving non-convex problems whose objective function is the sum of a number of smooth component functions plus a convex (possibly non-s...

Modern genomics research relies on genome-wide association studies (GWAS) to identify the few genetic variants among potentially millions that are associated with diseases of interest. Only reproducib...

Genomics biobanks are information treasure troves with thousands of phenotypes (e.g., diseases, traits) and millions of single nucleotide polymorphisms (SNPs). The development of methodologies that pr...

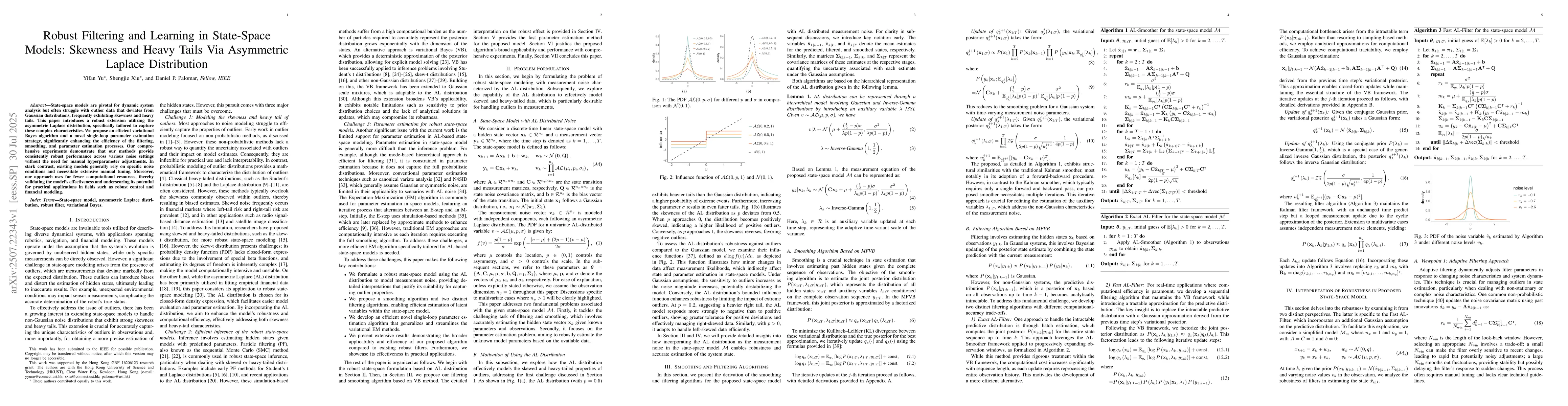

In this paper, we present a novel optimization algorithm designed specifically for estimating state-space models to deal with heavy-tailed measurement noise and constraints. Our algorithm addresses tw...

Graph models provide efficient tools to capture the underlying structure of data defined over networks. Many real-world network topologies are subject to change over time. Learning to model the dynami...

This tutorial aims to provide signal processing (SP) and machine learning (ML) practitioners with vital tools, in an accessible way, to answer the question: How to deal with missing data? There are ma...

State-space models are pivotal for dynamic system analysis but often struggle with outlier data that deviates from Gaussian distributions, frequently exhibiting skewness and heavy tails. This paper in...

Controlling the false discovery rate (FDR) in high-dimensional variable selection requires balancing rigorous error control with statistical power. Existing methods with provable guarantees are often ...

High-dimensional variable selection, particularly in genomics, requires error-controlling procedures that scale to millions of predictors. The Terminating-Random Experiments (T-Rex) selector achieves ...

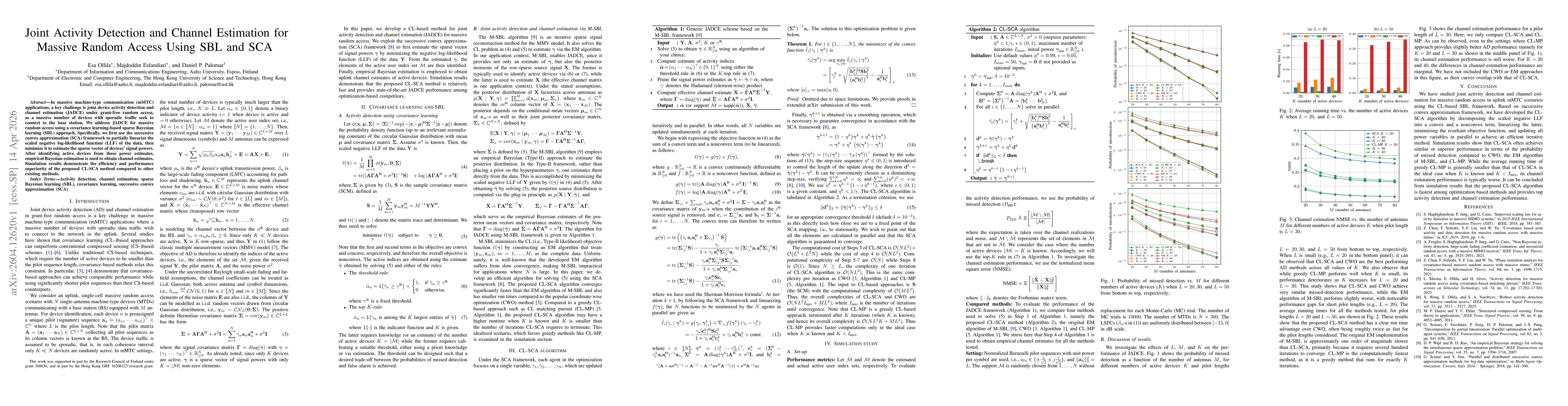

In massive machine-type communication (mMTC) applications, a key challenge is joint device activity detection and channel estimation (JADCE) under grant-free random access, as a massive number of devi...