Academic Profile

Statistics

Similar Authors

Papers on arXiv

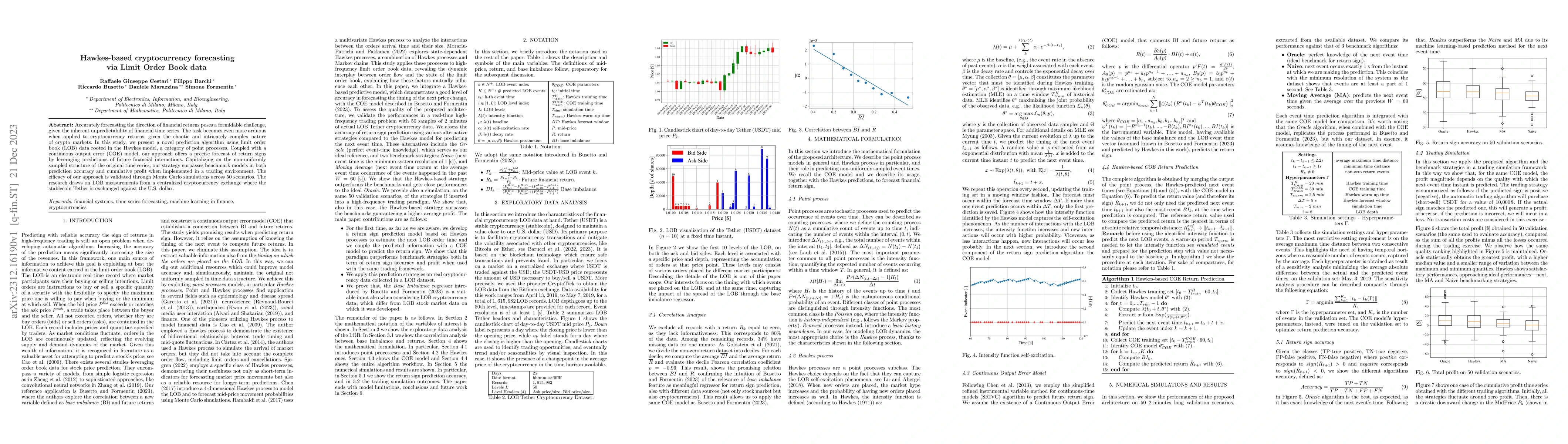

Accurately forecasting the direction of financial returns poses a formidable challenge, given the inherent unpredictability of financial time series. The task becomes even more arduous when applied ...

In this work we analytically solve an optimal retirement problem, in which the agent optimally allocates the risky investment, consumption and leisure rate to maximise a gain function characterised ...

In this paper we deal with the optimal bankruptcy problem for an agent who can optimally allocate her consumption rate, the amount of capital invested in the risky asset as well as her leisure time....

We present new numerical schemes for pricing perpetual Bermudan and American options as well as $\alpha$-quantile options. This includes a new direct calculation of the optimal exercise barrier for ...

We present numerical methods based on the fast Fourier transform (FFT) to solve convolution integral equations on a semi-infinite interval (Wiener-Hopf equation) or on a finite interval (Fredholm eq...

We show how spectral filters can improve the convergence of numerical schemes which use discrete Hilbert transforms based on a sinc function expansion, and thus ultimately on the fast Fourier transf...

In this note, we show how to solve an optimal retirement problem in presence of a stochastic wage dealing with a free boundary problem. In particular, we show how to deal with an incomplete market cas...

We explore the interplay between sovereign debt default/renegotiation and environmental factors (e.g., pollution from land use, natural resource exploitation). Pollution contributes to the likelihood ...

We investigate the optimal execution of contracts that are used in merger\&acquisition deals. We consider cash-settled and physically delivered contracts between a broker and a counterpart. Contracts ...