Academic Profile

Statistics

Similar Authors

Papers on arXiv

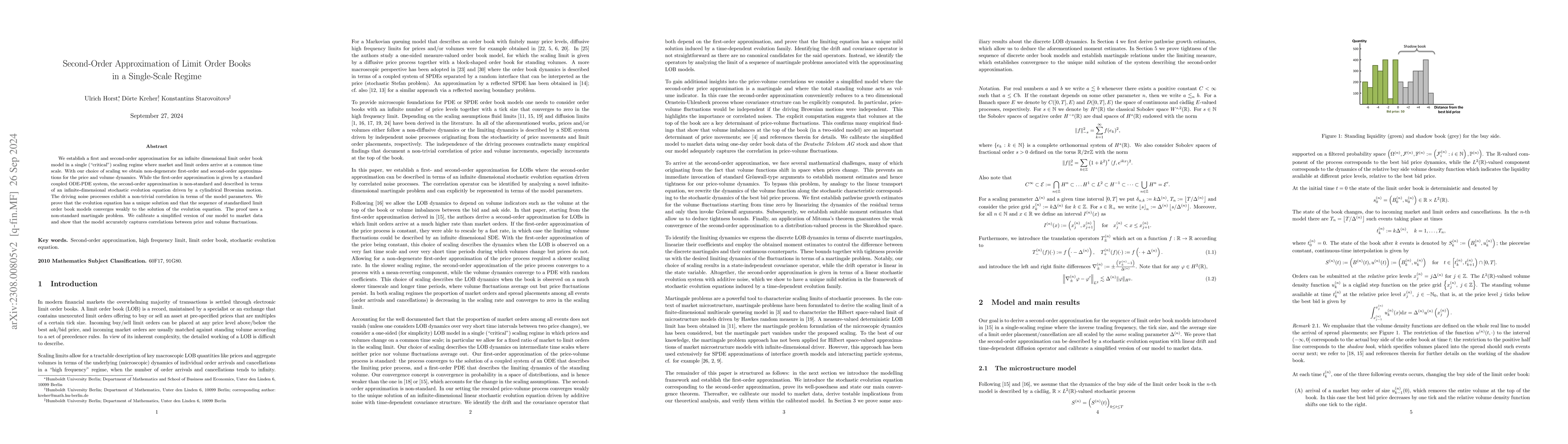

We establish a first and second-order approximation for an infinite dimensional limit order book model (LOB) in a single (''critical'') scaling regime where market and limit orders arrive at a commo...

The concept of correlated noise is well-established in discrete-time stochastic modelling but there is no generally agreed-upon definition of the notion of red noise in continuous-time stochastic mo...

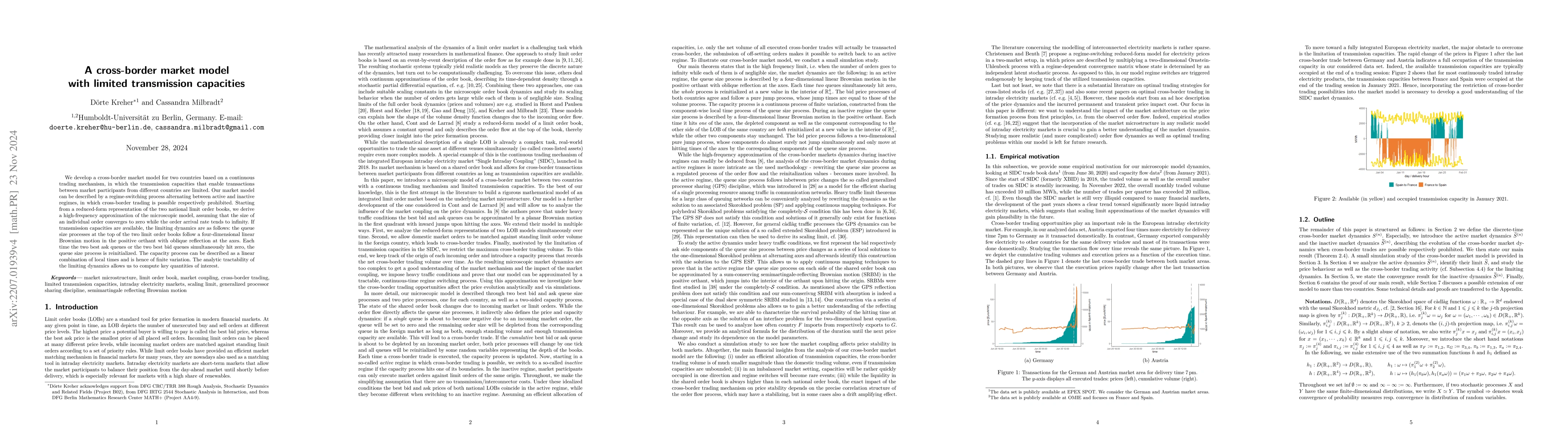

We develop a cross-border market model between two countries in which the transmission capacities that enable transactions between market participants of different countries are limited. Starting fr...

We introduce a new definition of speculative bubbles in discrete-time models based on the discounted stock price losing mass at some finite drop-down under an equivalent martingale measure. We provi...

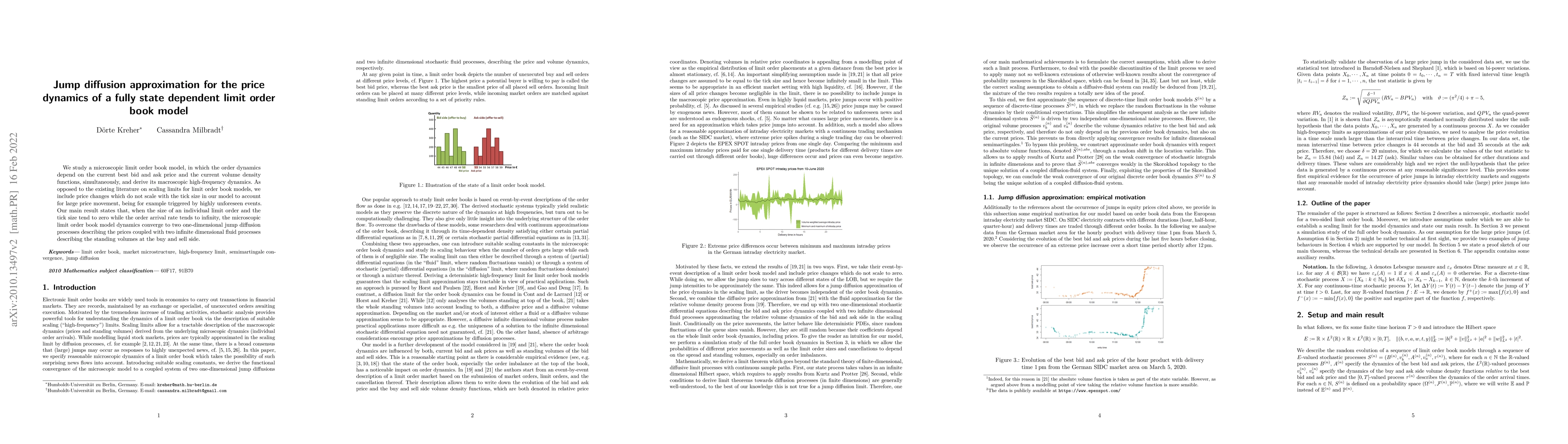

We study a microscopic limit order book model, in which the order dynamics depend on the current best bid and ask price and the current volume density functions, simultaneously, and derive its macro...

We construct non-negative martingale solutions to the stochastic porous medium equation in one dimension with homogeneous Dirichlet boundary conditions which exhibit a type of sticky behavior at zero....

We study the dependence of the fractional Riccati equation in the rough Heston model on the Hurst parameter $H$. For each expansion point $H_0\in(-1/2,1/2]$, we derive a Taylor expansion of the Riccat...