Academic Profile

Statistics

Similar Authors

Papers on arXiv

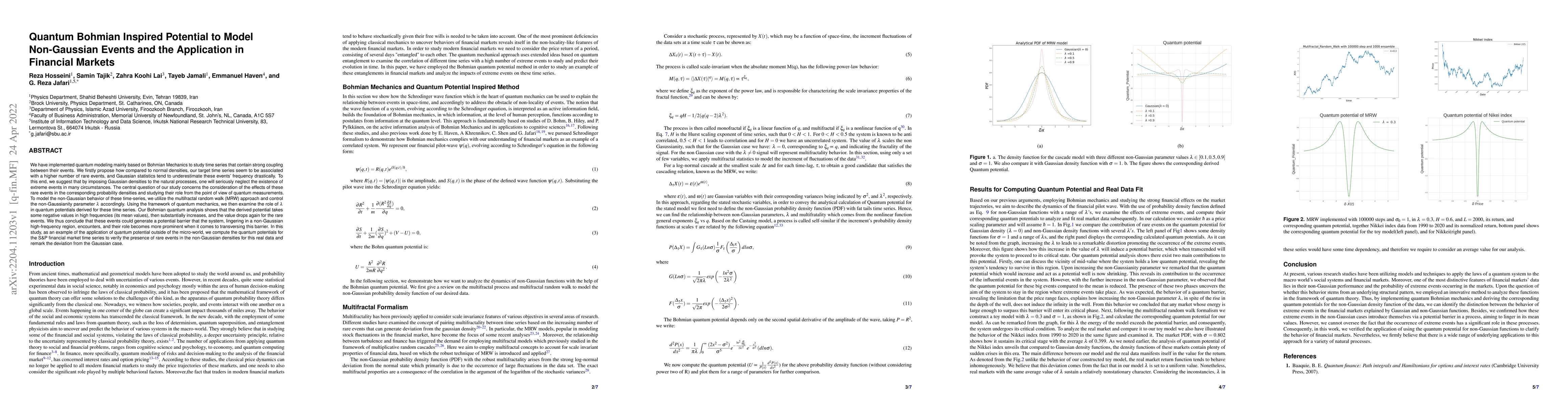

We have implemented quantum modeling mainly based on Bohmian Mechanics to study time series that contain strong coupling between their events. We firstly propose how compared to normal densities, ou...

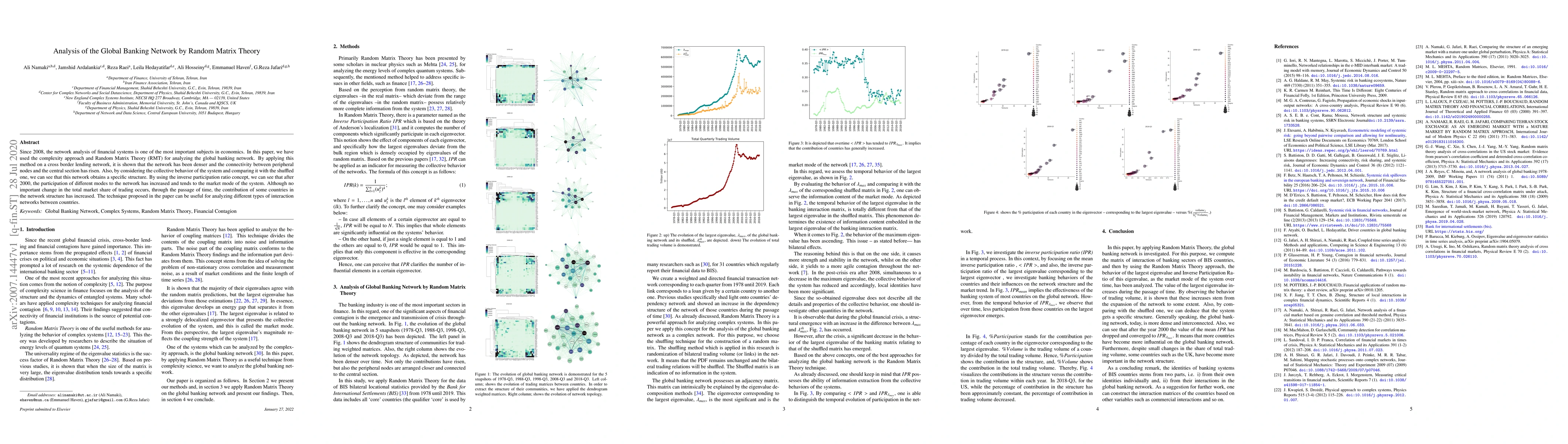

Since 2008, the network analysis of financial systems is one of the most important subjects in economics. In this paper, we have used the complexity approach and Random Matrix Theory (RMT) for analy...

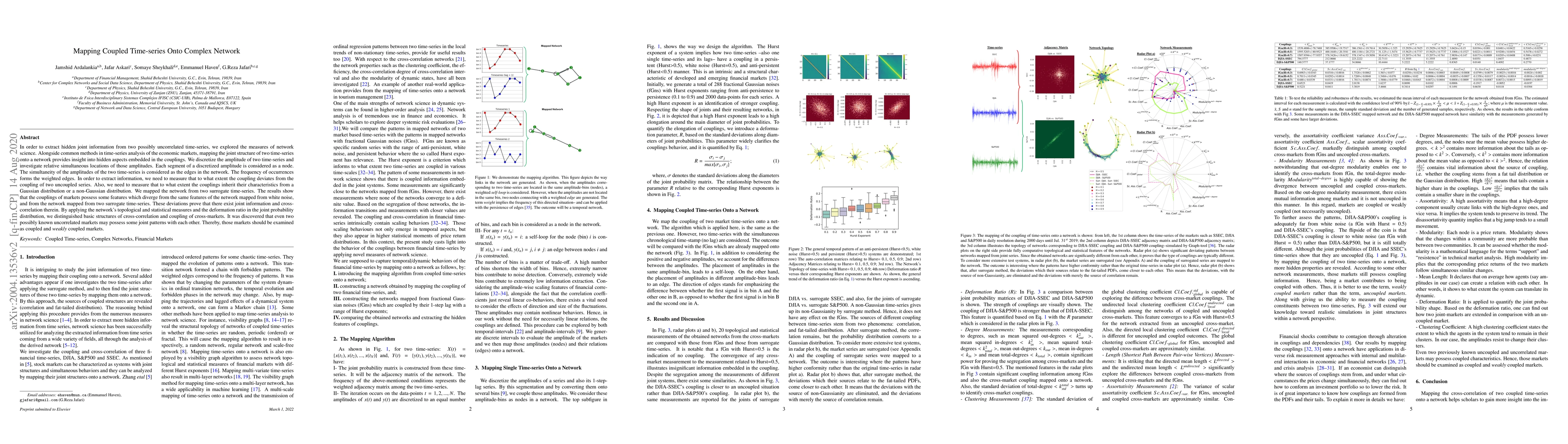

In order to extract hidden joint information from two possibly uncorrelated time-series, we explored the measures of network science. Alongside common methods in time-series analysis of the economic...

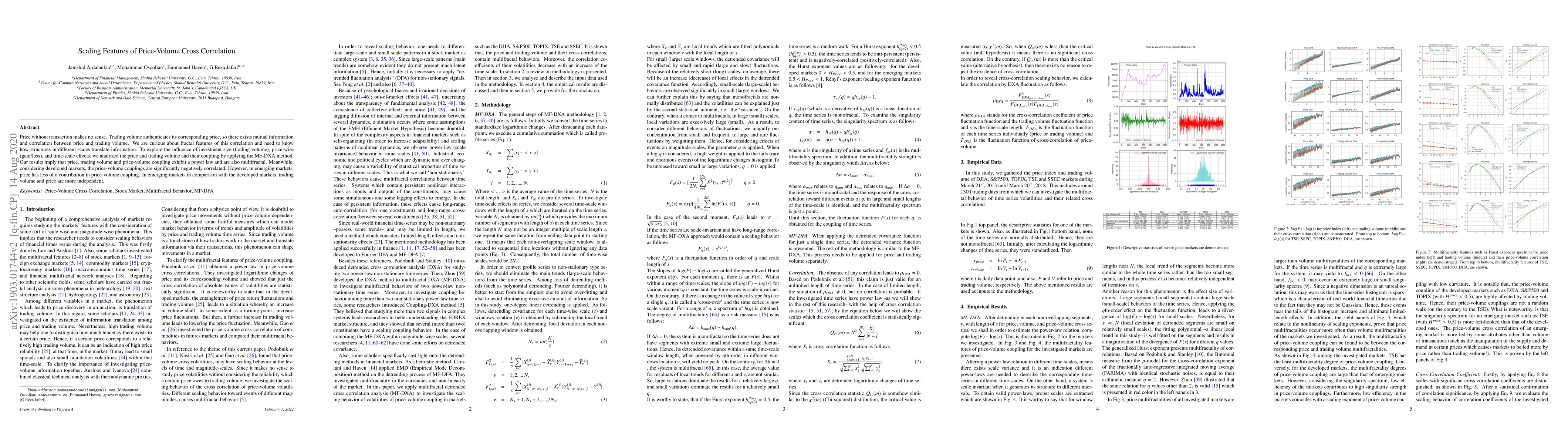

Price without transaction makes no sense. Trading volume authenticates its corresponding price, so there exist mutual information and correlation between price and trading volume. We are curious abo...