Academic Profile

Statistics

Similar Authors

Papers on arXiv

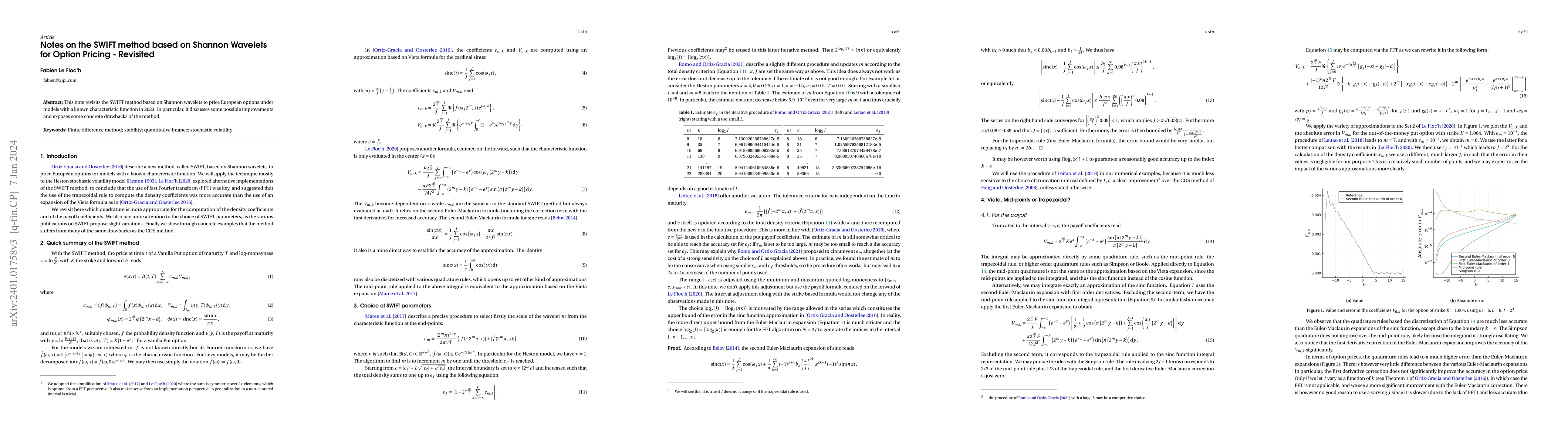

This note revisits the SWIFT method based on Shannon wavelets to price European options under models with a known characteristic function in 2023. In particular, it discusses some possible improveme...

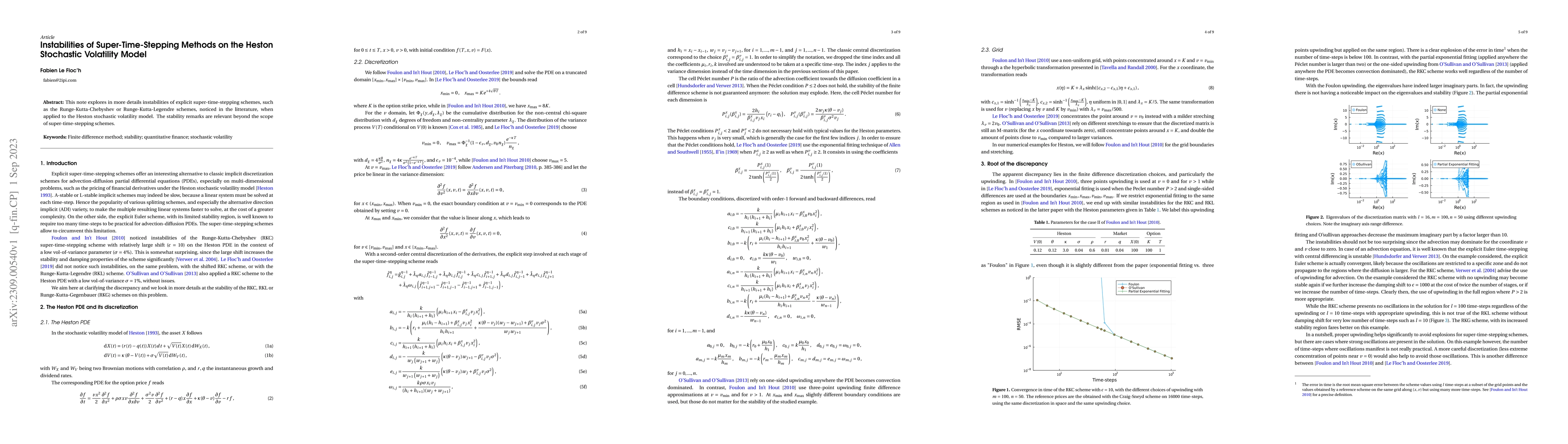

This note explores in more details instabilities of explicit super-time-stepping schemes, such as the Runge-Kutta-Chebyshev or Runge-Kutta-Legendre schemes, noticed in the litterature, when applied ...

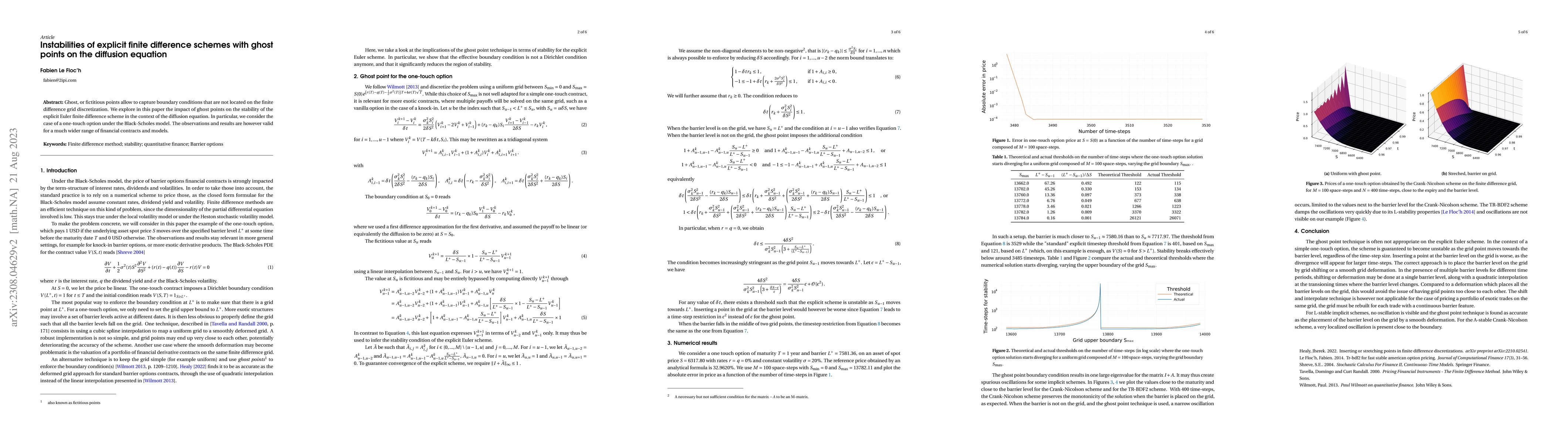

Ghost, or fictitious points allow to capture boundary conditions that are not located on the finite difference grid discretization. We explore in this paper the impact of ghost points on the stabili...

This paper generalizes the local variance gamma model of Carr and Nadtochiy, to a piecewise quadratic local variance function. The formulation encompasses the piecewise linear Bachelier and piecewis...

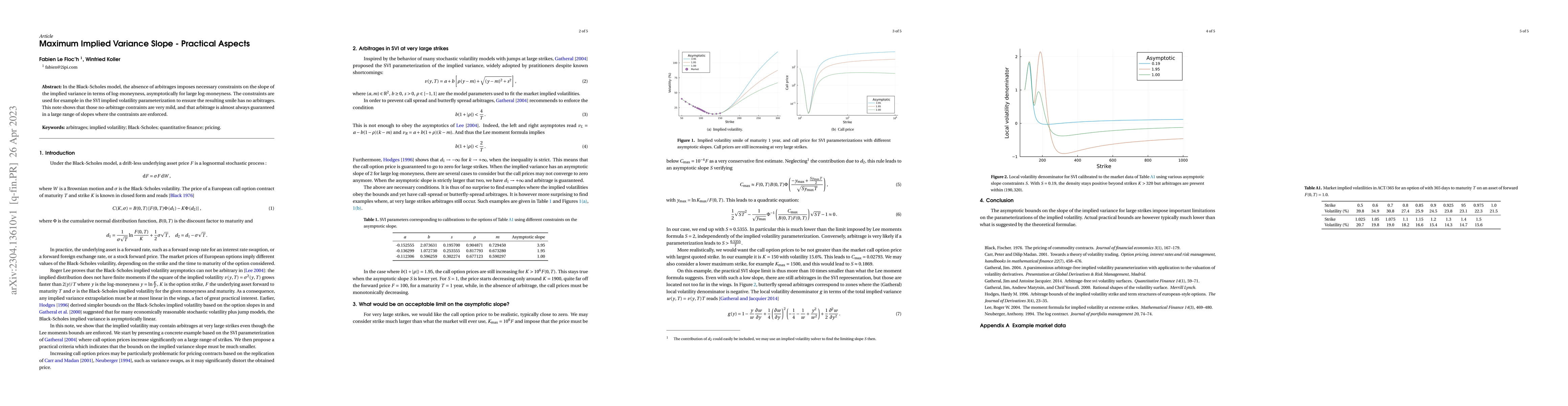

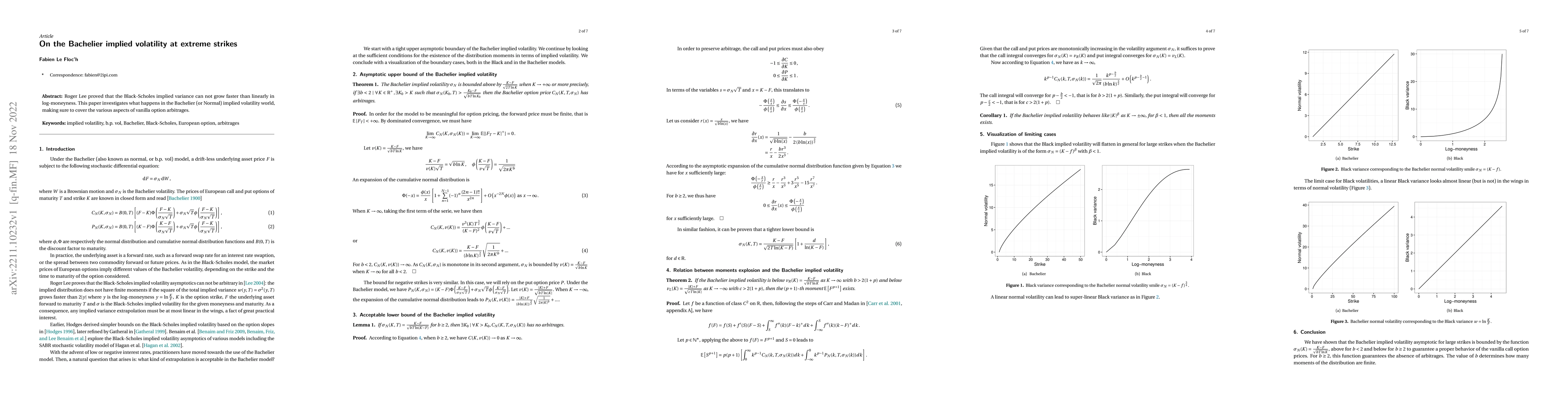

In the Black-Scholes model, the absence of arbitrages imposes necessary constraints on the slope of the implied variance in terms of log-moneyness, asymptotically for large log-moneyness. The constr...

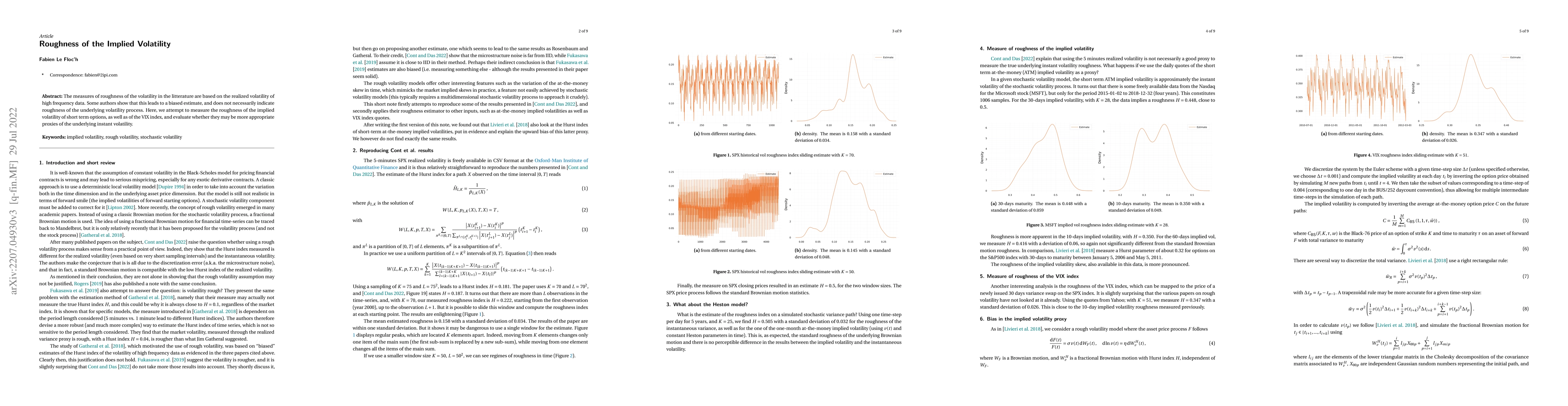

What kind of implied volatility extrapolation is appropriate? Roger Lee proved that the Black-Scholes implied variance can not grow faster than linearly in log-moneyness. This paper investigates wha...

The measures of roughness of the volatility in the litterature are based on the realized volatility of high frequency data. Some authors show that this leads to a biased estimate, and does not neces...

The classic Brennan-Schwartz algorithm to solve the linear complementary problem, which arises from the finite difference discretization of the partial differential equation related to American opti...

This paper presents how to apply the stochastic collocation technique to assets that can not move below a boundary. It shows that the polynomial collocation towards a lognormal distribution does not...

There is no exact closed form formula for pricing of European options with discrete cash dividends under the model where the underlying asset price follows a piecewise lognormal process with jumps a...

This paper presents the Runge-Kutta-Legendre finite difference scheme, allowing for an additional shift in its polynomial representation. A short presentation of the stability region, comparatively ...

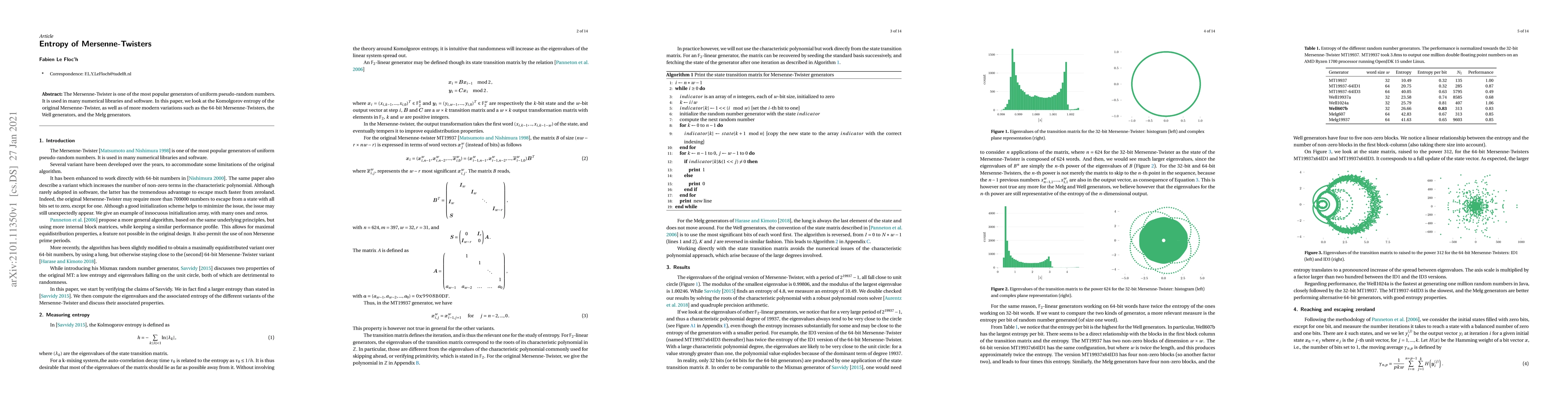

The Mersenne-Twister is one of the most popular generators of uniform pseudo-random numbers. It is used in many numerical libraries and software. In this paper, we look at the Komolgorov entropy of ...

This note shows that the cosine expansion based on the Vieta formula is equivalent to a discretization of the Parseval identity. We then evaluate the use of simple direct algorithms to compute the S...

This paper presents simple formulae for the local variance gamma model of Carr and Nadtochiy, extended with a piecewise-linear local variance function. The new formulae allow to calibrate the model ...

We present closed analytical approximations for the pricing of Asian basket spread options under the Black-Scholes model. The formulae are obtained by using a stochastic Taylor expansion around a log-...

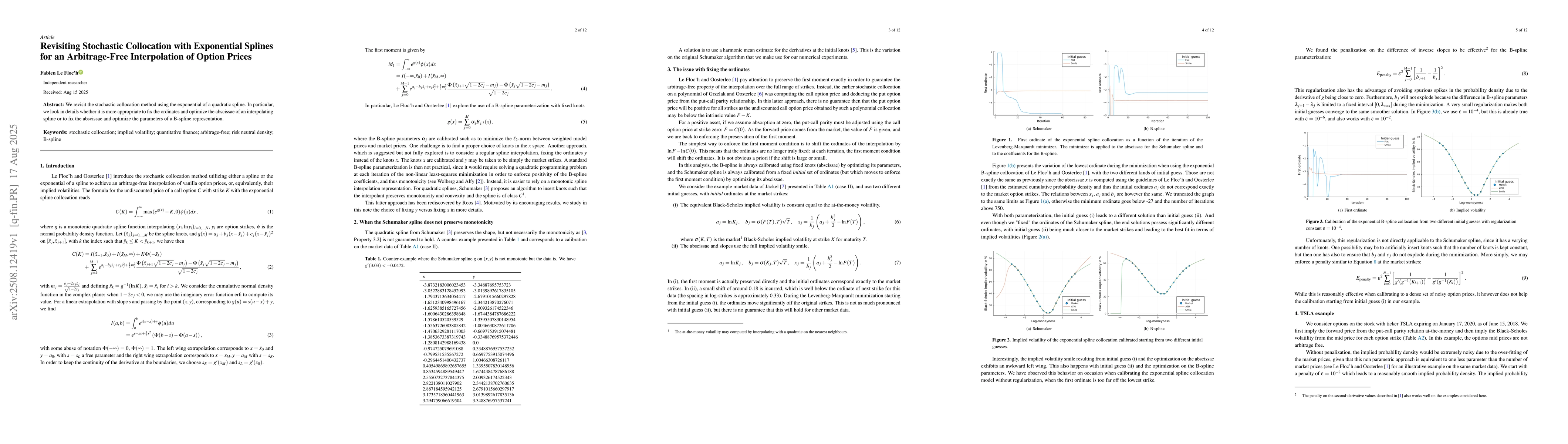

We revisit the stochastic collocation method using the exponential of a quadratic spline. In particular, we look in details whether it is more appropriate to fix the ordinates and optimize the absciss...

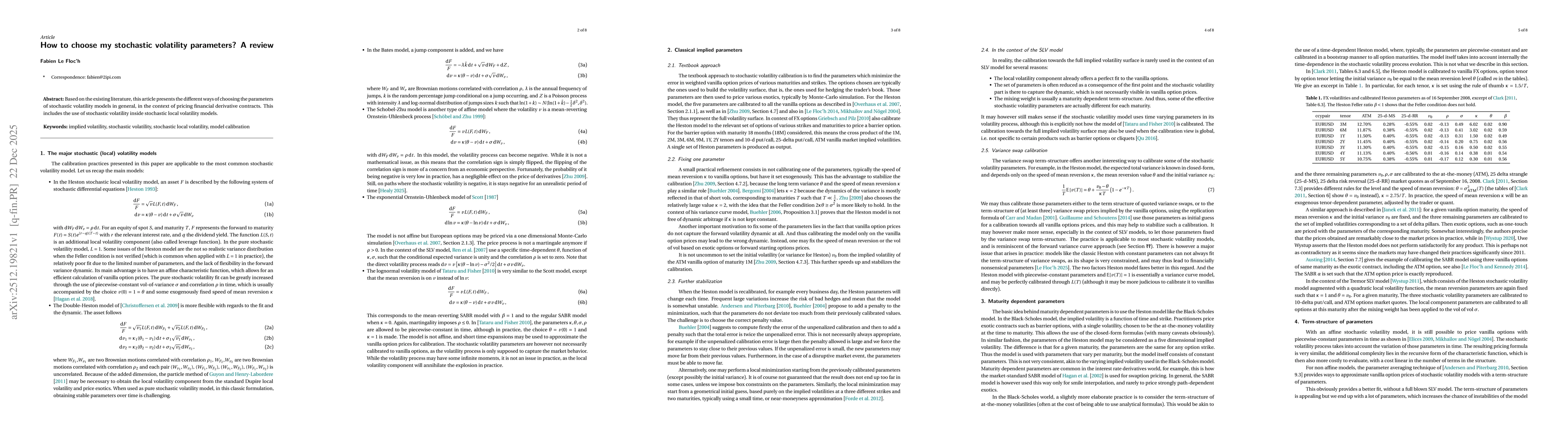

Based on the existing literature, this article presents the different ways of choosing the parameters of stochastic volatility models in general, in the context of pricing financial derivative contrac...

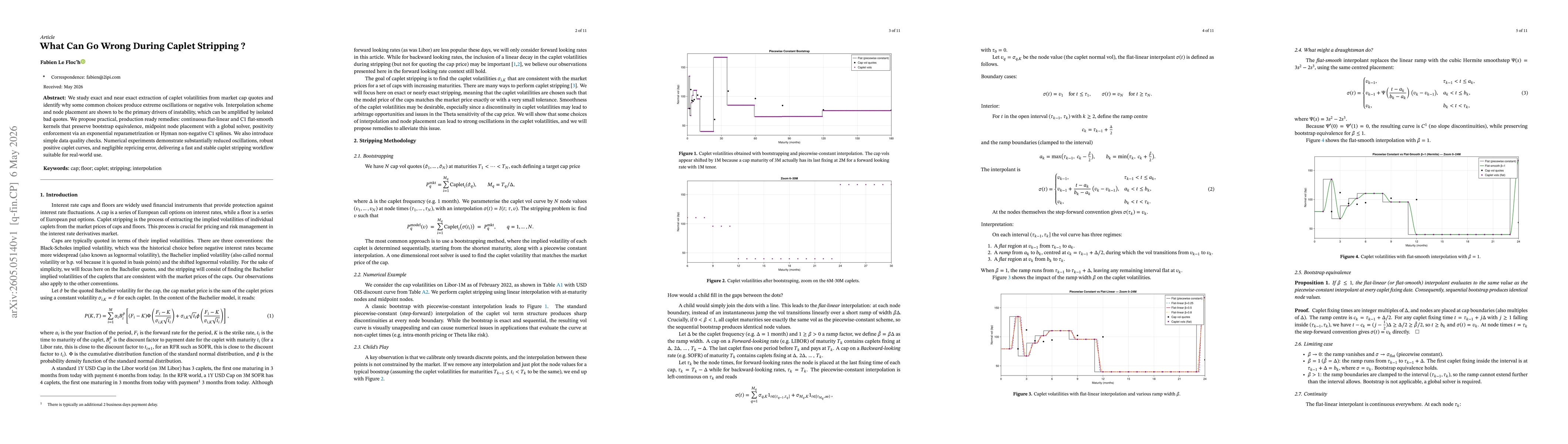

We study exact and near exact extraction of caplet volatilities from market cap quotes and identify why some common choices produce extreme oscillations or negative vols. Interpolation scheme and node...

We present two explicit rational formulae for Bachelier, or normal, implied volatility. The formulae take the option price, forward, strike, and expiry as inputs and return the implied normal volatili...

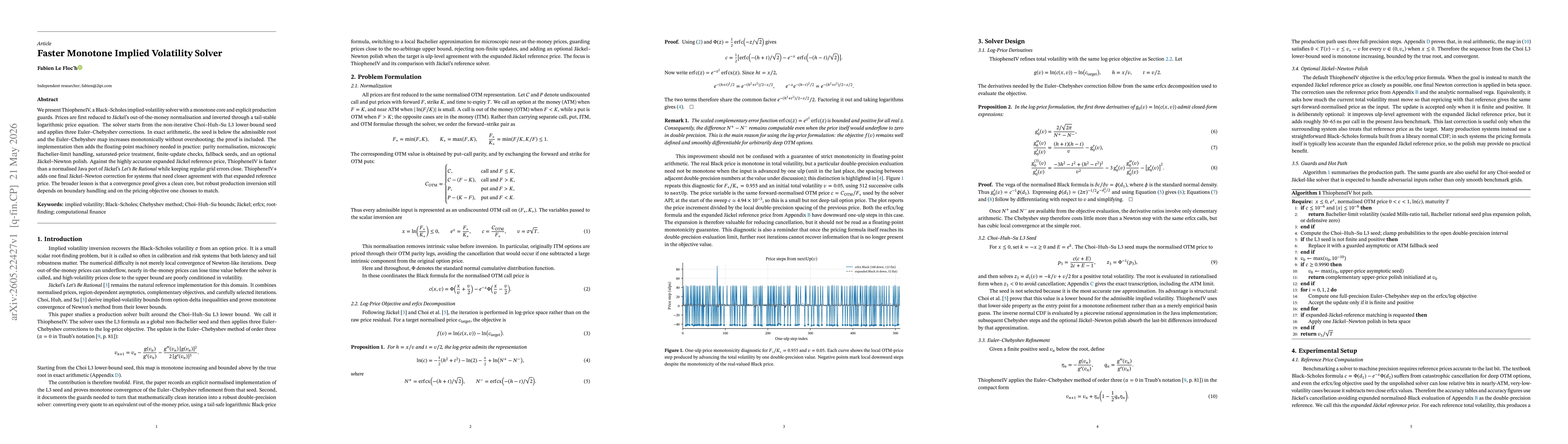

We present ThiopheneIV, a Black-Scholes implied-volatility solver with a monotone core and explicit production guards. Prices are first reduced to Jäckel's out-of-the-money normalisation and inverted ...

FlashIV is a low-latency Black--Scholes implied-volatility solver for production use. It normalises each input to an out-of-the-money price and solves a tail-stable erfcx/log-price residual. The hot p...