Academic Profile

Statistics

Similar Authors

Papers on arXiv

The profit and loss (p&l) attrition for each business year into different risk or risk factors (e.g., interest rates, credit spreads, foreign exchange rate etc.) is a regulatory requirement, e.g., u...

We provide a unified framework to obtain numerically certain quantities, such as the distribution function, absolute moments and prices of financial options, from the characteristic function of some...

The Fourier-cosine expansion (COS) method is used to price European options numerically in a very efficient way. To apply the COS method, one has to specify two parameters: a truncation range for th...

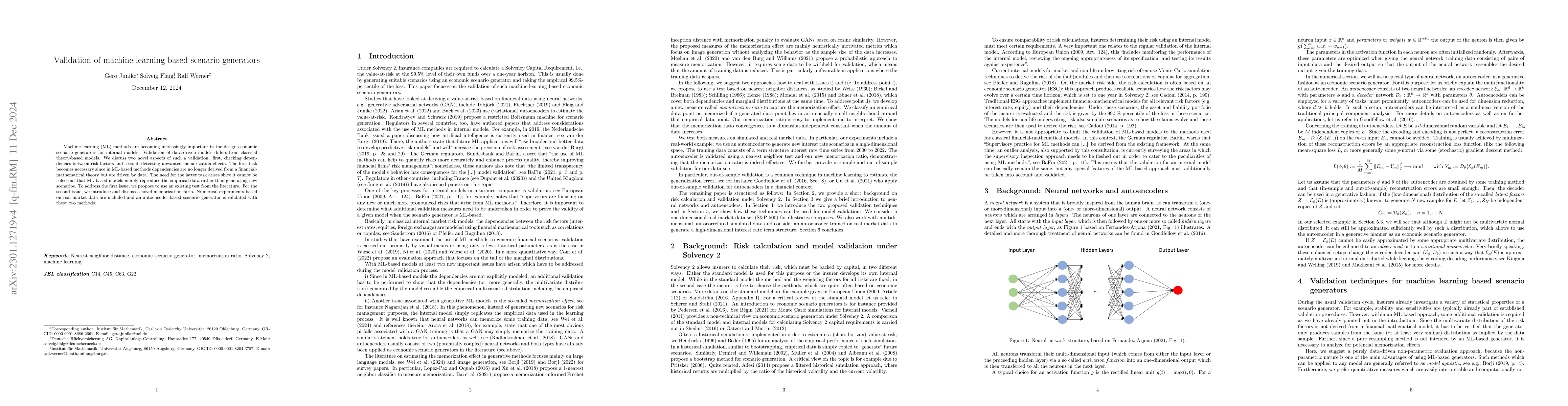

Machine learning methods are getting more and more important in the development of internal models using scenario generation. As internal models under Solvency 2 have to be validated, an important q...

Dybvig (1988a,b) solves in a complete market setting the problem of finding a payoff that is cheapest possible in reaching a given target distribution ("cost-efficient payoff"). In the presence of a...

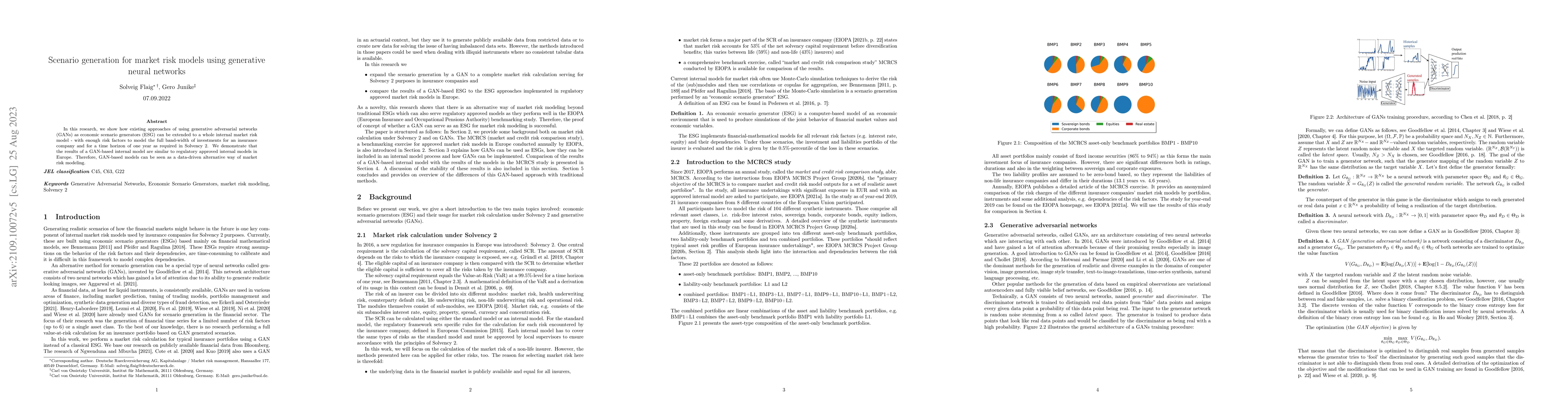

In this research, we show how to expand existing approaches of using generative adversarial networks (GANs) as economic scenario generators (ESG) to a whole internal market risk model - with enough ...

The Fourier cosine expansion (COS) method is used for pricing European options numerically very fast. To apply the COS method, a truncation range for the density of the log-returns need to be provid...

Fourier pricing methods such as the Carr-Madan formula or the COS method are classic tools for pricing European options for advanced models such as the Heston model. These methods require tuning param...

We provide theoretical error bounds for the accurate numerical computation of the quantile function given the characteristic function of a continuous random variable. We show theoretically and empiric...

Batch normalization is one of the most important regularization techniques for neural networks, significantly improving training by centering the layers of the neural network. There have been several ...

Neural networks are able to approximate any continuous function on a compact set. However, it is not obvious how to quantify the error of the neural network, i.e., the remaining bias between the funct...

The surplus of a life insurance policy depends on both systematic changes in mortality risk and financial changes. We propose to decompose the surplus by the axiomatically justified IASU decomposition...