Guido Gazzani

5 papers on arXiv

Academic Profile

Statistics

Similar Authors

Papers on arXiv

Pricing and calibration in the 4-factor path-dependent volatility model

We consider the path-dependent volatility (PDV) model of Guyon and Lekeufack (2023), where the instantaneous volatility is a linear combination of a weighted sum of past returns and the square root ...

Joint calibration to SPX and VIX options with signature-based models

We consider a stochastic volatility model where the dynamics of the volatility are described by linear functions of the (time extended) signature of a primary underlying process, which is supposed t...

Signature-based models: theory and calibration

We consider asset price models whose dynamics are described by linear functions of the (time extended) signature of a primary underlying process, which can range from a (market-inferred) Brownian mo...

Risk measures under model uncertainty: a Bayesian viewpoint

We introduce two kinds of risk measures with respect to some reference probability measure, which both allow for a certain order structure and domination property. Analyzing their relation to each o...

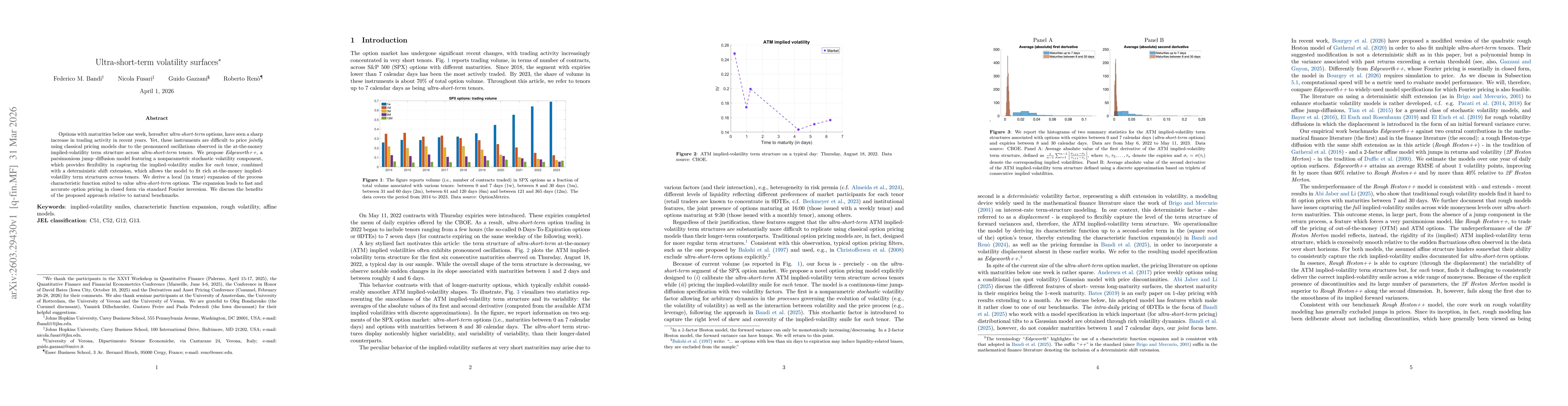

Ultra-short-term volatility surfaces

Options with maturities below one week, hereafter "ultra-short-term" options, have seen a sharp increase in trading activity in recent years. Yet, these instruments are difficult to price jointly usin...