Academic Profile

Statistics

Similar Authors

Papers on arXiv

Portfolio managers' orders trade off return and trading cost predictions. Return predictions rely on alpha models, whereas price impact models quantify trading costs. This paper studies what happens...

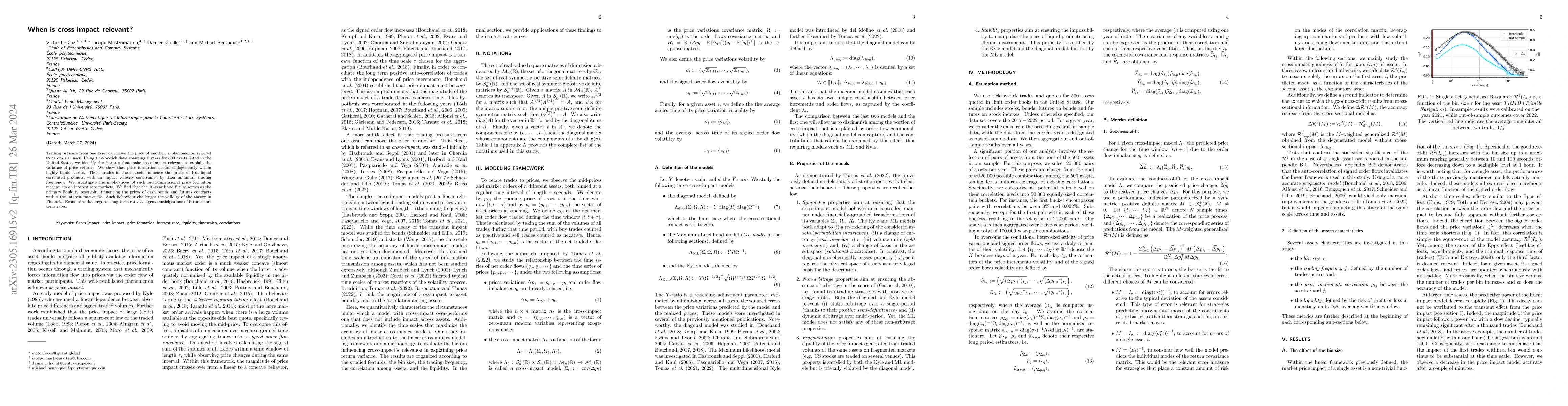

Trading pressure from one asset can move the price of another, a phenomenon referred to as cross impact. Using tick-by-tick data spanning 5 years for 500 assets listed in the United States, we ident...

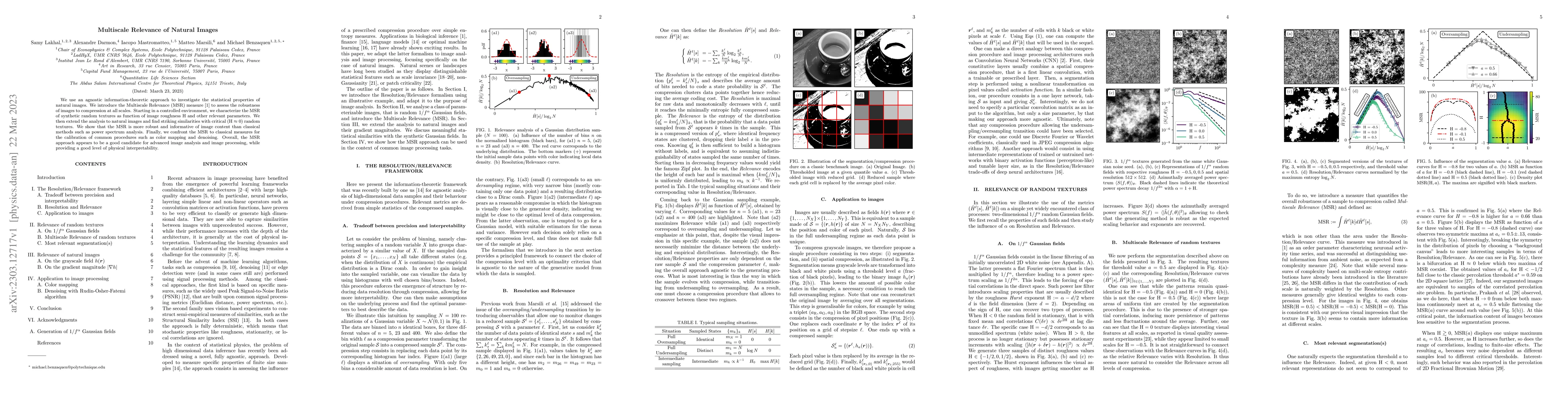

We use an agnostic information-theoretic approach to investigate the statistical properties of natural images. We introduce the Multiscale Relevance (MSR) measure to assess the robustness of images ...

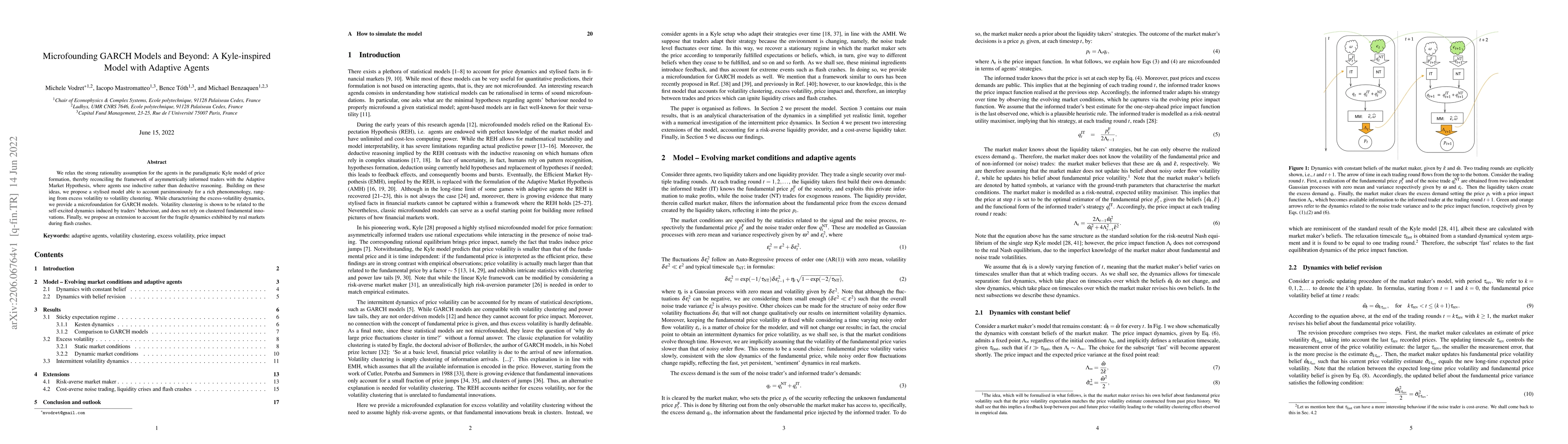

We relax the strong rationality assumption for the agents in the paradigmatic Kyle model of price formation, thereby reconciling the framework of asymmetrically informed traders with the Adaptive Ma...

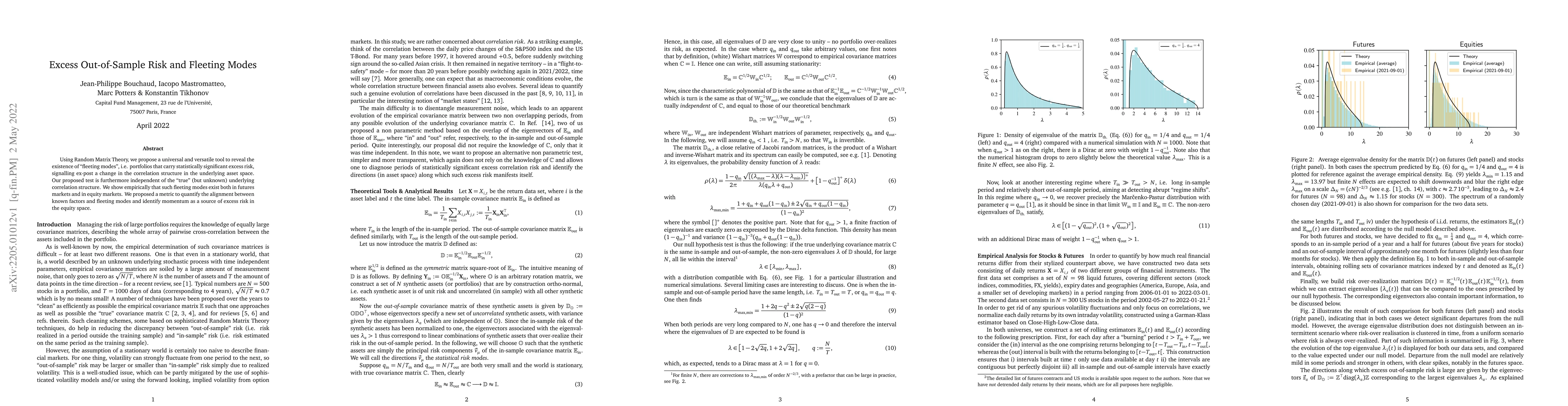

Using Random Matrix Theory, we propose a universal and versatile tool to reveal the existence of "fleeting modes", i.e. portfolios that carry statistically significant excess risk, signalling ex-pos...

We compare the predictions of the stationary Kyle model, a microfounded multi-step linear price impact model in which market prices forecast fundamentals through information encoded in the order flo...

Trading a financial asset pushes its price as well as the prices of other assets, a phenomenon known as cross-impact. The empirical estimation of this effect on complex financial instruments, such a...

We provide an economically sound micro-foundation to linear price impact models, by deriving them as the equilibrium of a suitable agent-based system. Our setup generalizes the well-known Kyle model...

Trading a financial instrument pushes its price and those of other assets, a phenomenon known as cross-impact. To be of use, cross-impact models must fit data and be well-behaved so they can be appl...

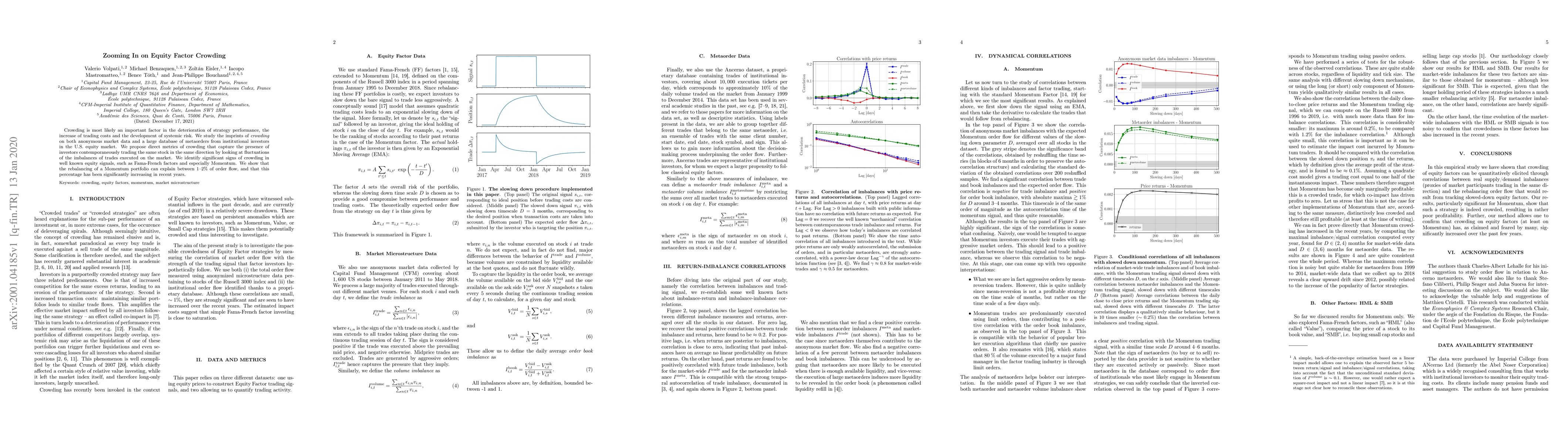

Crowding is most likely an important factor in the deterioration of strategy performance, the increase of trading costs and the development of systemic risk. We study the imprints of \emph{crowding}...

The phenomenology of the forward rate curve (FRC) can be accurately understood by the fluctuations of a stiff elastic string (Le Coz and Bouchaud, 2024). By relating the exogenous shocks driving such ...