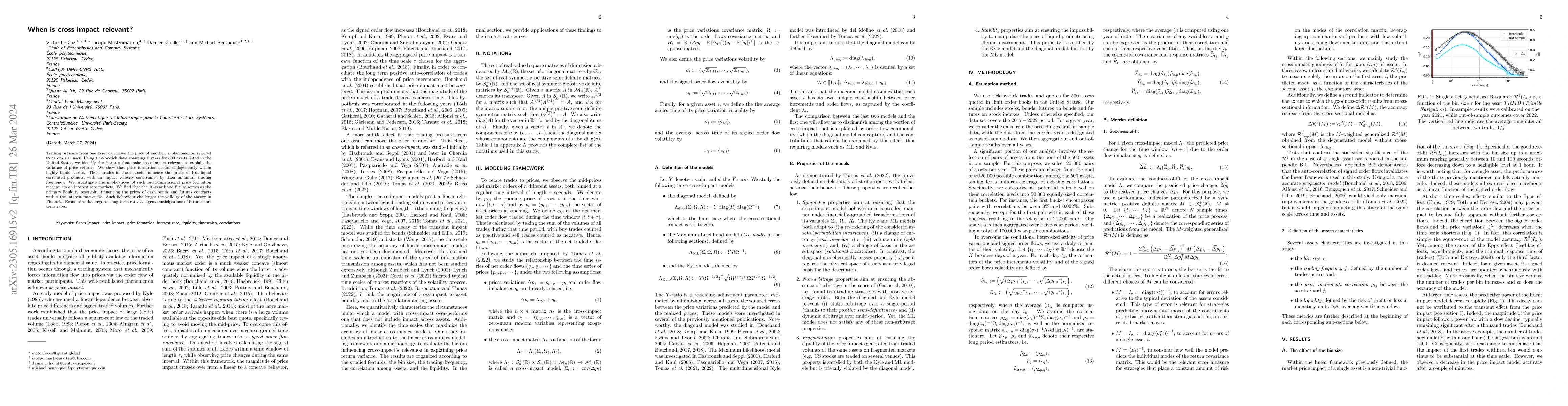

Trading pressure from one asset can move the price of another, a phenomenon

referred to as cross impact. Using tick-by-tick data spanning 5 years for 500

assets listed in the United States, we identify the features that make

cross-impact relevant to explain the variance of price returns. We show that

price formation occurs endogenously within highly liquid assets. Then, trades

in these assets influence the prices of less liquid correlated products, with

an impact velocity constrained by their minimum trading frequency. We

investigate the implications of such a multidimensional price formation

mechanism on interest rate markets. We find that the 10-year bond future serves

as the primary liquidity reservoir, influencing the prices of cash bonds and

futures contracts within the interest rate curve. Such behaviour challenges the

validity of the theory in Financial Economics that regards long-term rates as

agents anticipations of future short term rates.

Discussion 0