Academic Profile

Statistics

Similar Authors

Papers on arXiv

Twenty five years ago, several authors proposed to model the forward interest rate curve (FRC) as an elastic string along which idiosyncratic shocks propagate, accounting for the peculiar structure ...

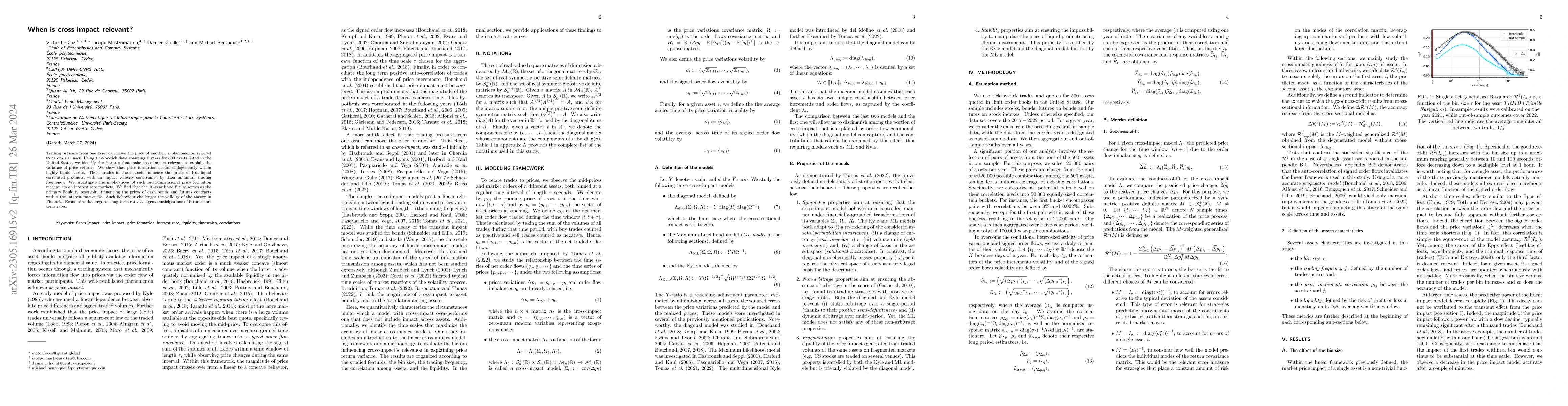

Trading pressure from one asset can move the price of another, a phenomenon referred to as cross impact. Using tick-by-tick data spanning 5 years for 500 assets listed in the United States, we ident...

We propose a minimal model of the secured interbank network able to shed light on recent money markets puzzles. We find that excess liquidity emerges due to the interactions between the reserves and l...

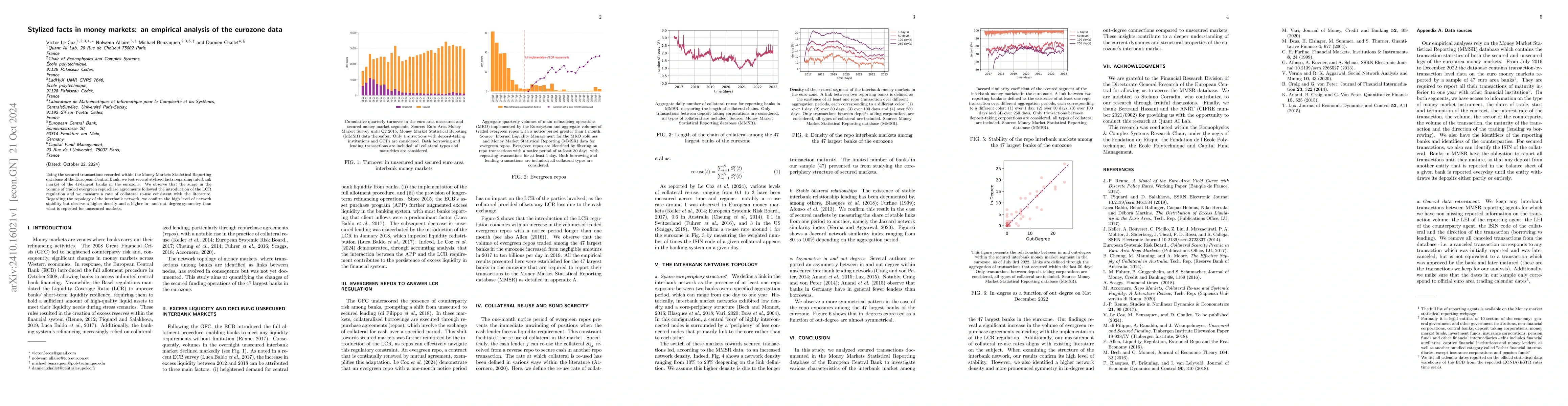

Using the secured transactions recorded within the Money Markets Statistical Reporting database of the European Central Bank, we test several stylized facts regarding interbank market of the 47 larges...

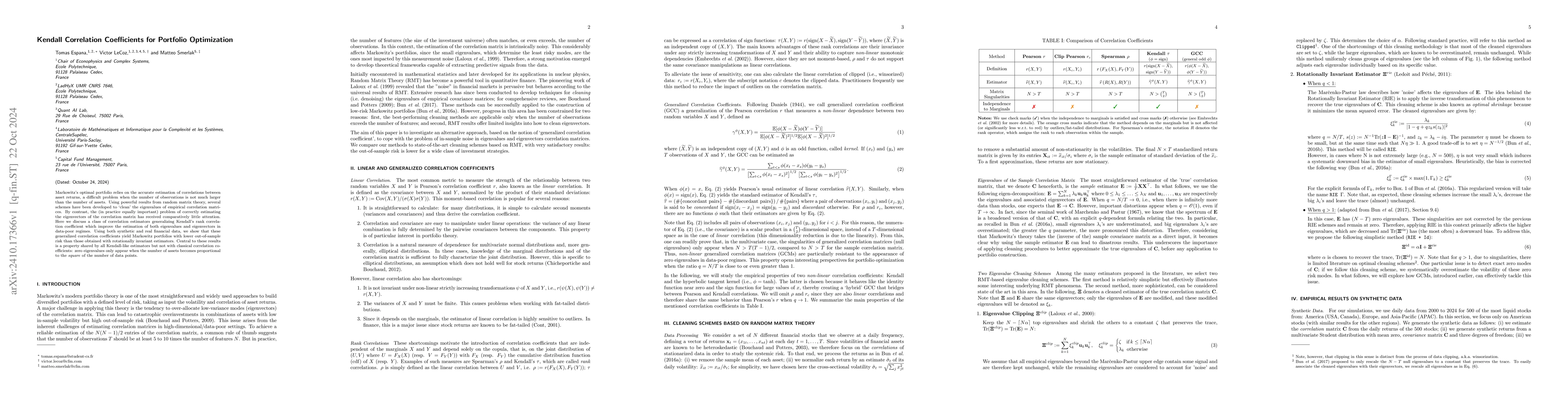

Markowitz's optimal portfolio relies on the accurate estimation of correlations between asset returns, a difficult problem when the number of observations is not much larger than the number of assets....

The phenomenology of the forward rate curve (FRC) can be accurately understood by the fluctuations of a stiff elastic string (Le Coz and Bouchaud, 2024). By relating the exogenous shocks driving such ...