Academic Profile

Statistics

Similar Authors

Papers on arXiv

Equity auctions display several distinctive characteristics in contrast to continuous trading. As the auction time approaches, the rate of events accelerates causing a substantial liquidity buildup ...

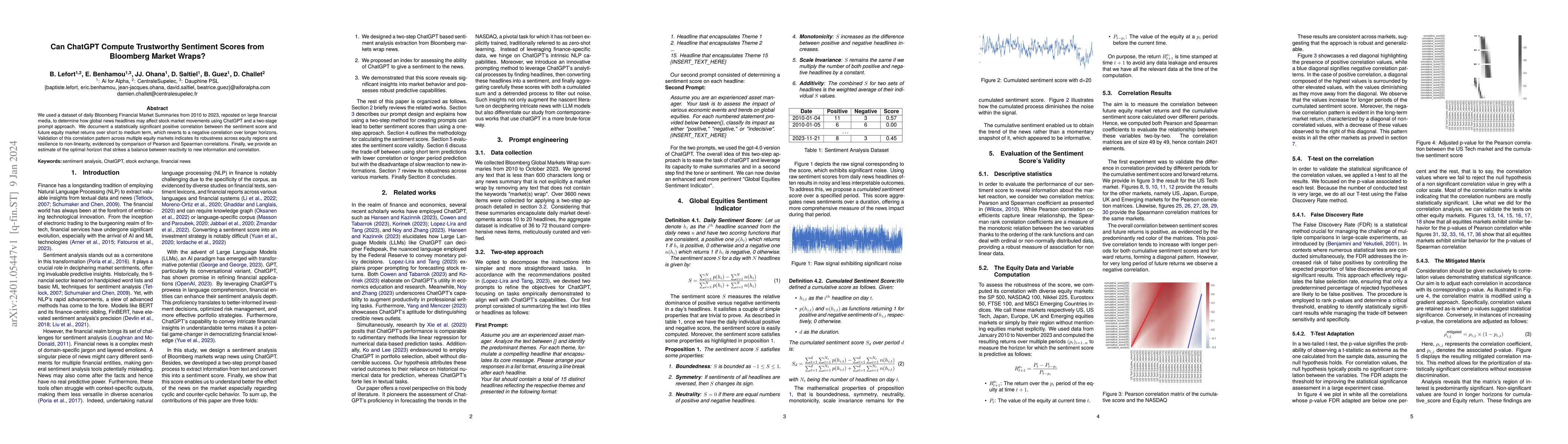

We used a dataset of daily Bloomberg Financial Market Summaries from 2010 to 2023, reposted on large financial media, to determine how global news headlines may affect stock market movements using C...

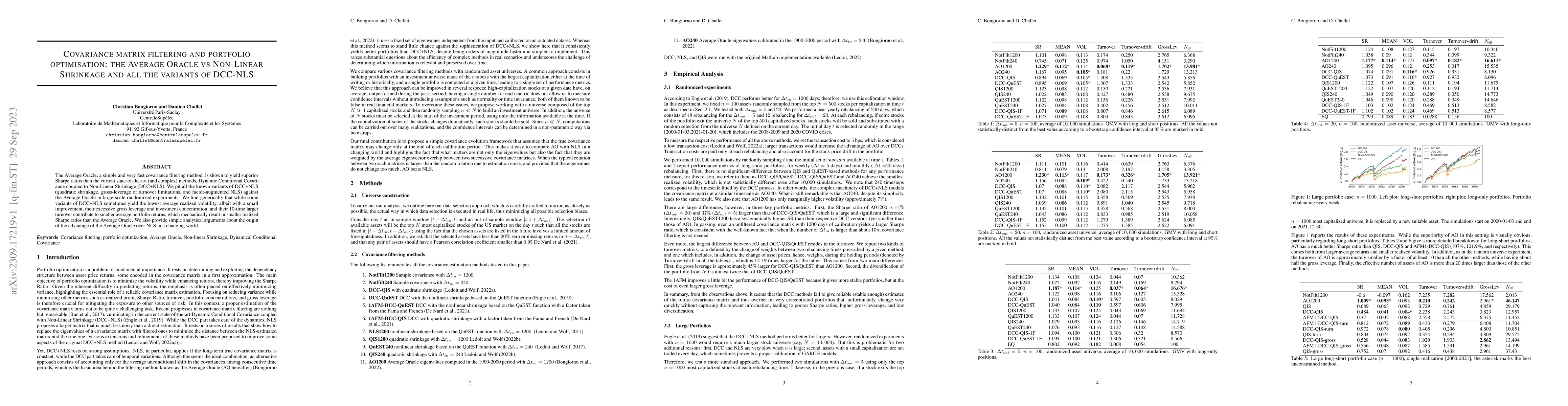

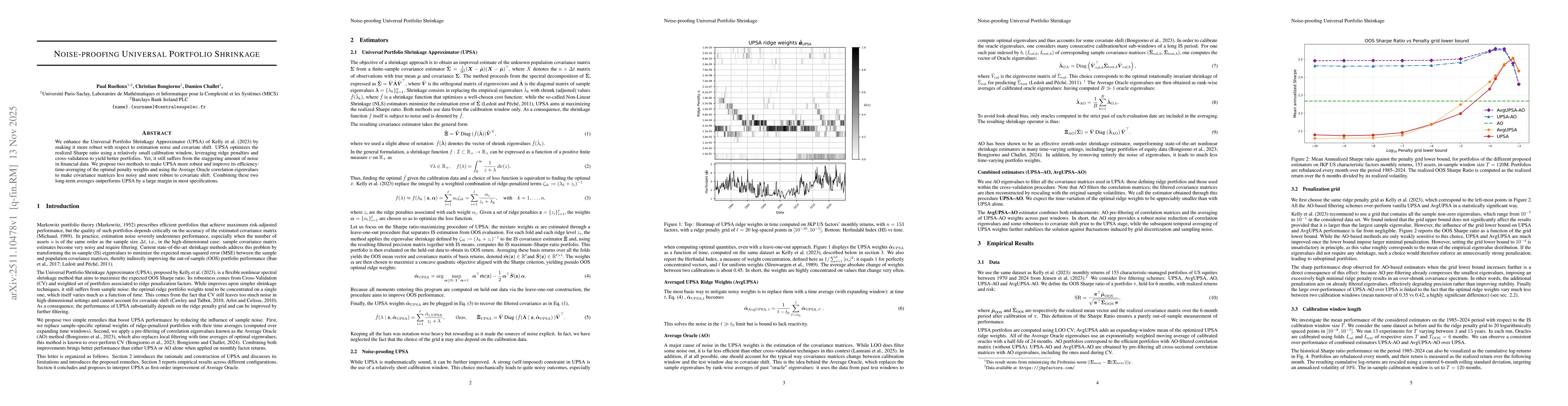

The Average Oracle, a simple and very fast covariance filtering method, is shown to yield superior Sharpe ratios than the current state-of-the-art (and complex) methods, Dynamic Conditional Covarian...

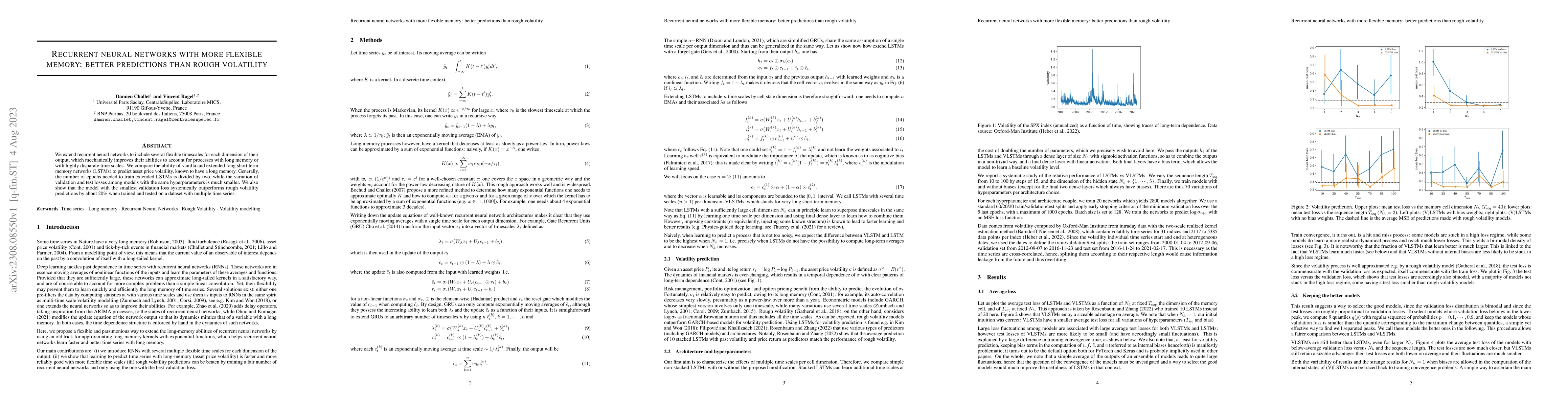

We extend recurrent neural networks to include several flexible timescales for each dimension of their output, which mechanically improves their abilities to account for processes with long memory o...

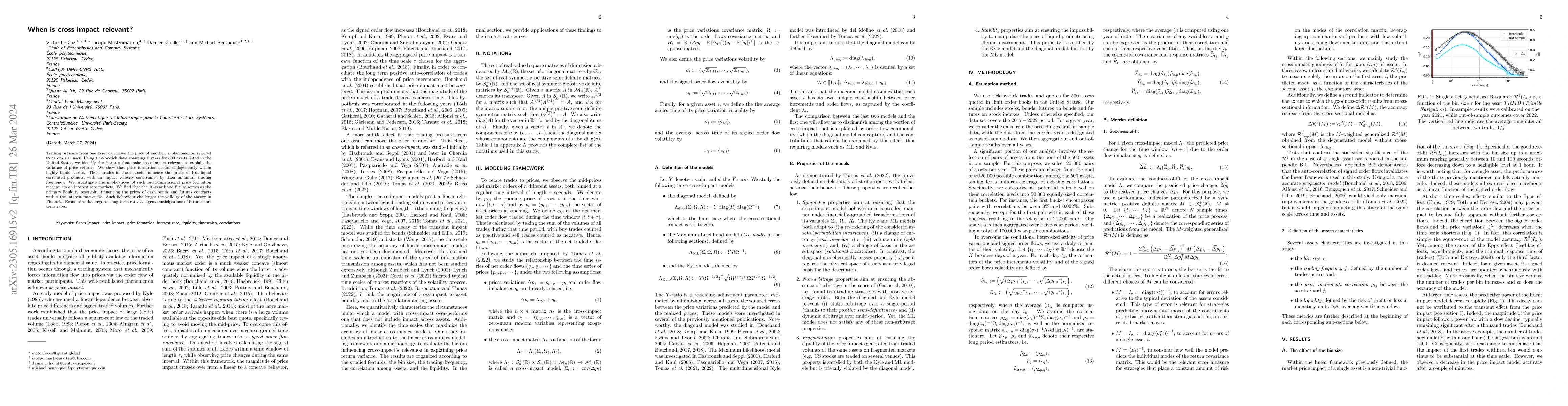

Trading pressure from one asset can move the price of another, a phenomenon referred to as cross impact. Using tick-by-tick data spanning 5 years for 500 assets listed in the United States, we ident...

Using high-quality data, we report several statistical regularities of equity auctions in the Paris stock exchange. First, the average order book density is linear around the auction price at the ti...

Symbolic transfer entropy is a powerful non-parametric tool to detect lead-lag between time series. Because a closed expression of the distribution of Transfer Entropy is not known for finite-size s...

We systematically investigate the links between price returns and Environment, Social and Governance (ESG) scores in the European equity market. Using interpretable machine learning, we examine whet...

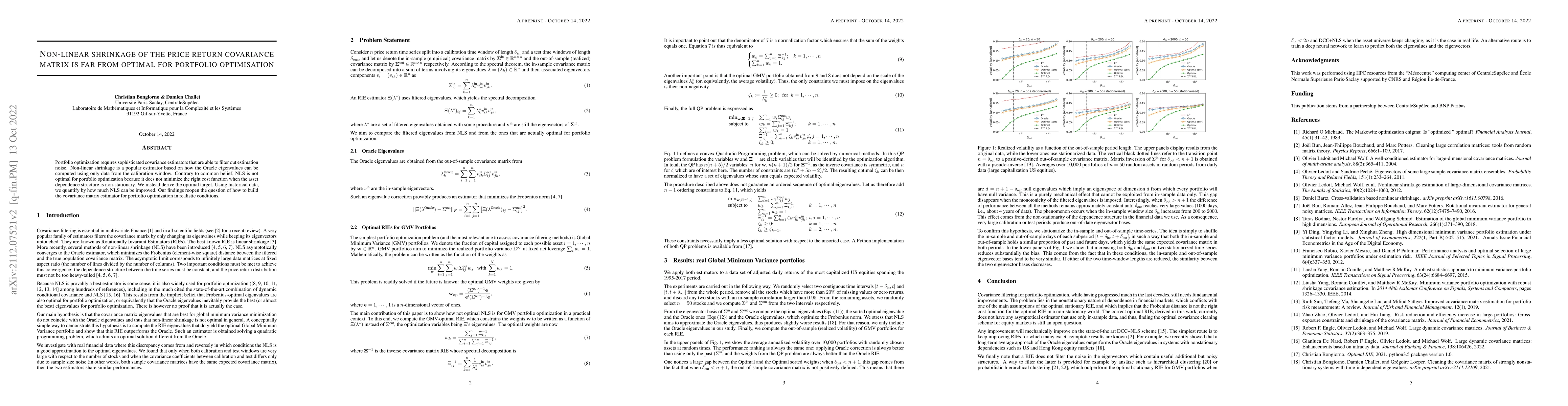

Portfolio optimization requires sophisticated covariance estimators that are able to filter out estimation noise. Non-linear shrinkage is a popular estimator based on how the Oracle eigenvalues can ...

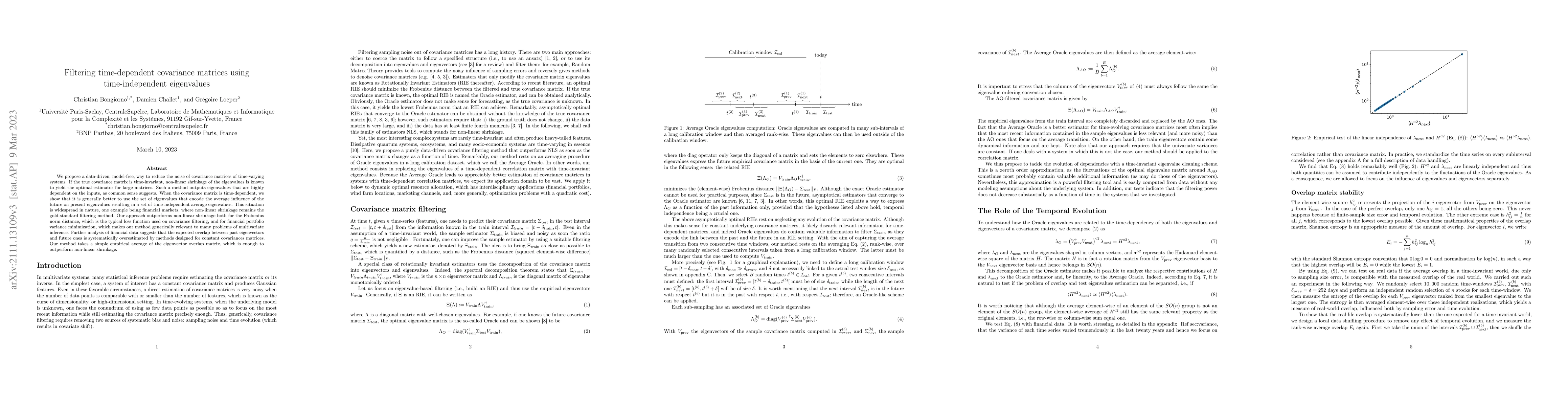

We propose a data-driven way to reduce the noise of covariance matrices of nonstationary systems. In the case of stationary systems, asymptotic approaches were proved to converge to the optimal solu...

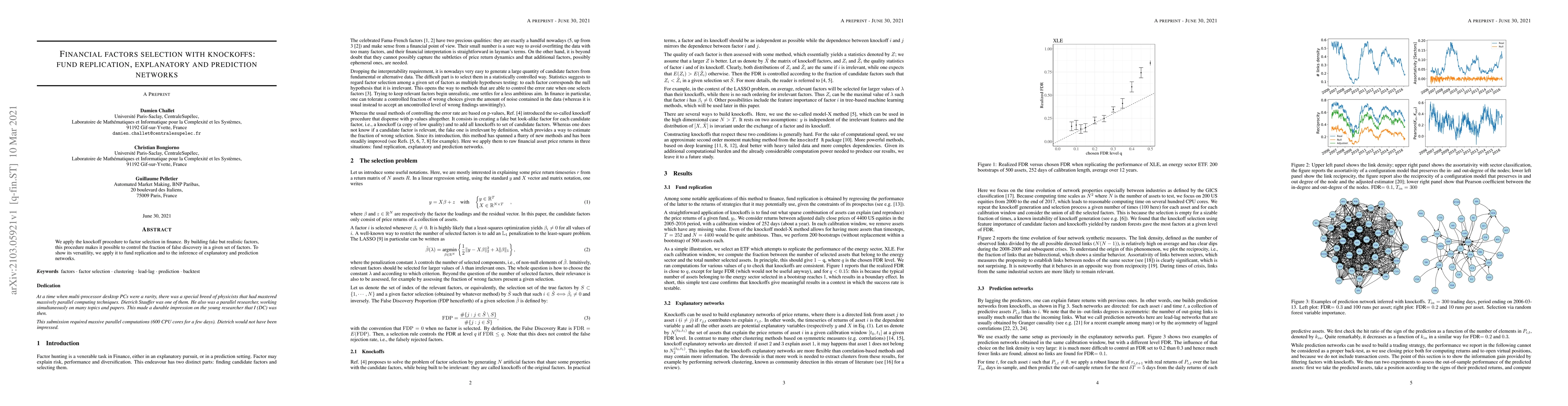

We apply the knockoff procedure to factor selection in finance. By building fake but realistic factors, this procedure makes it possible to control the fraction of false discovery in a given set of ...

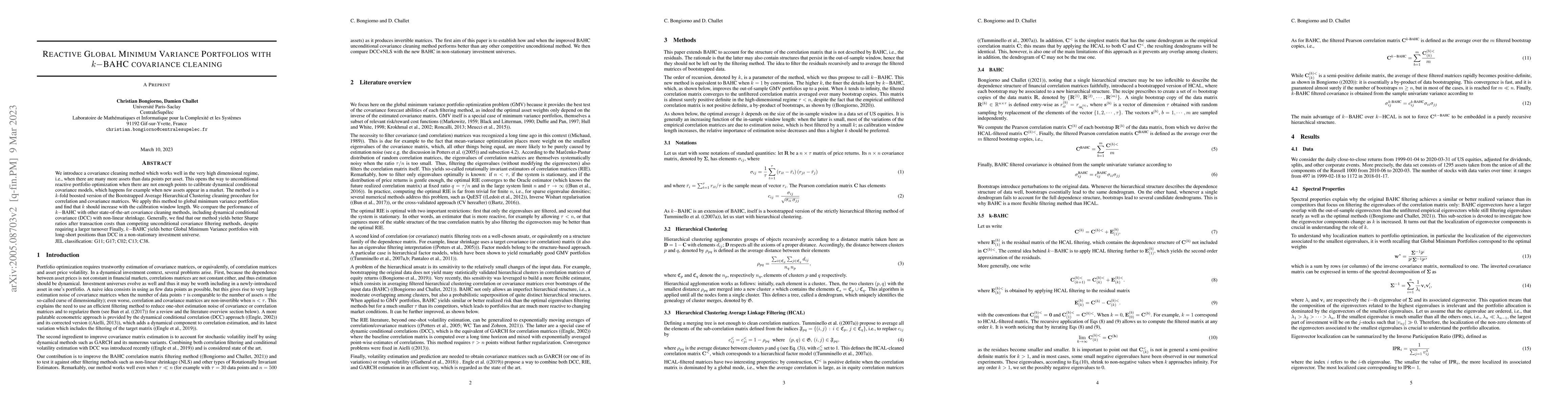

We introduce a $k$-fold boosted version of our Boostrapped Average Hierarchical Clustering cleaning procedure for correlation and covariance matrices. We then apply this method to global minimum var...

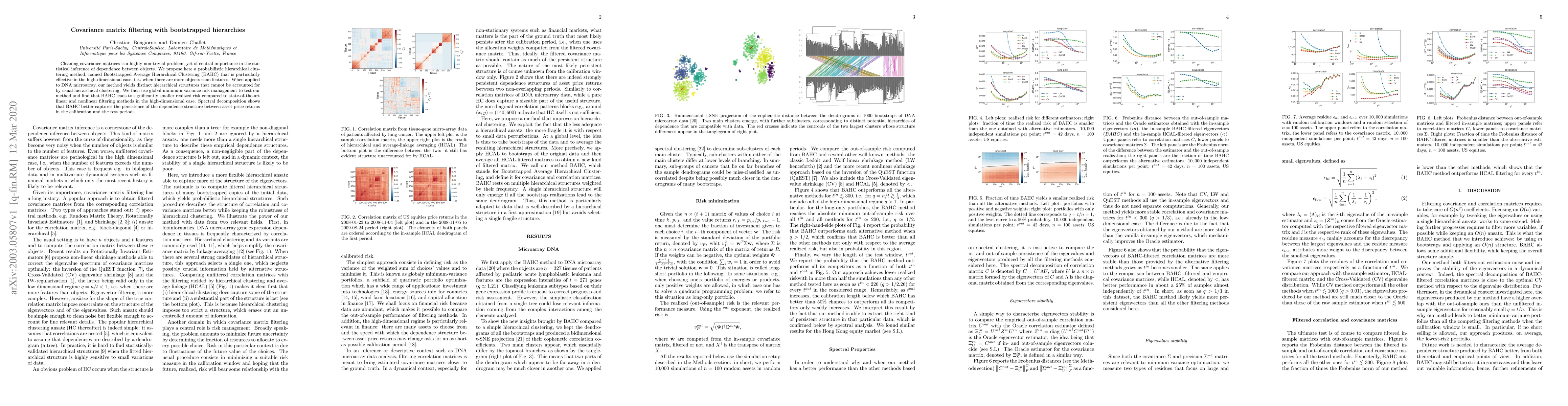

Statistical inference of the dependence between objects often relies on covariance matrices. Unless the number of features (e.g. data points) is much larger than the number of objects, covariance ma...

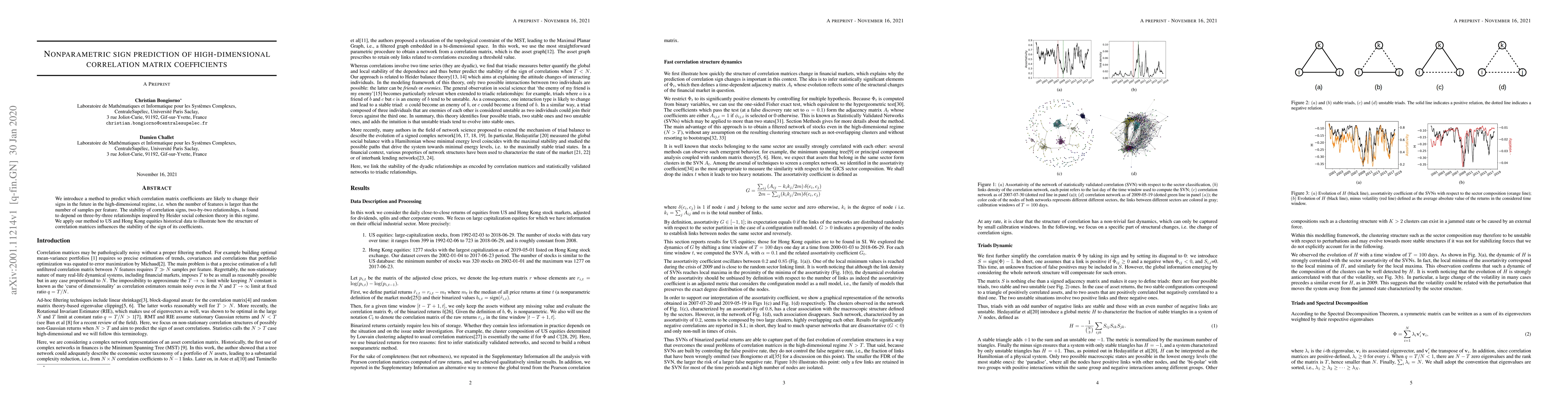

We introduce a method to predict which correlation matrix coefficients are likely to change their signs in the future in the high-dimensional regime, i.e. when the number of features is larger than ...

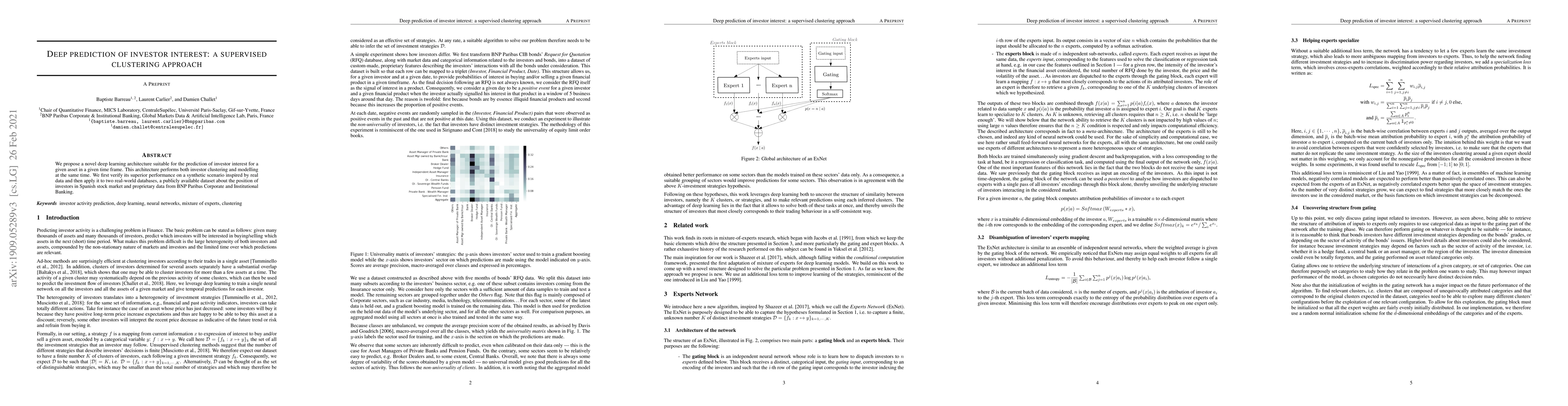

We propose a novel deep learning architecture suitable for the prediction of investor interest for a given asset in a given time frame. This architecture performs both investor clustering and modell...

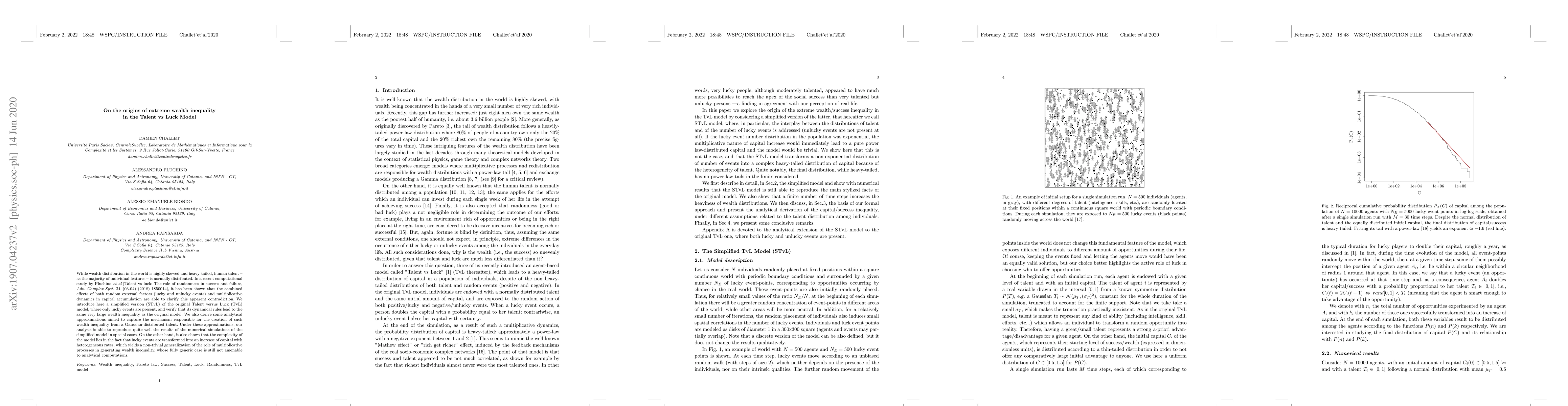

While wealth distribution in the world is highly skewed and heavy-tailed, human talent - as the majority of individual features - is normally distributed. In a recent computational study by Pluchino...

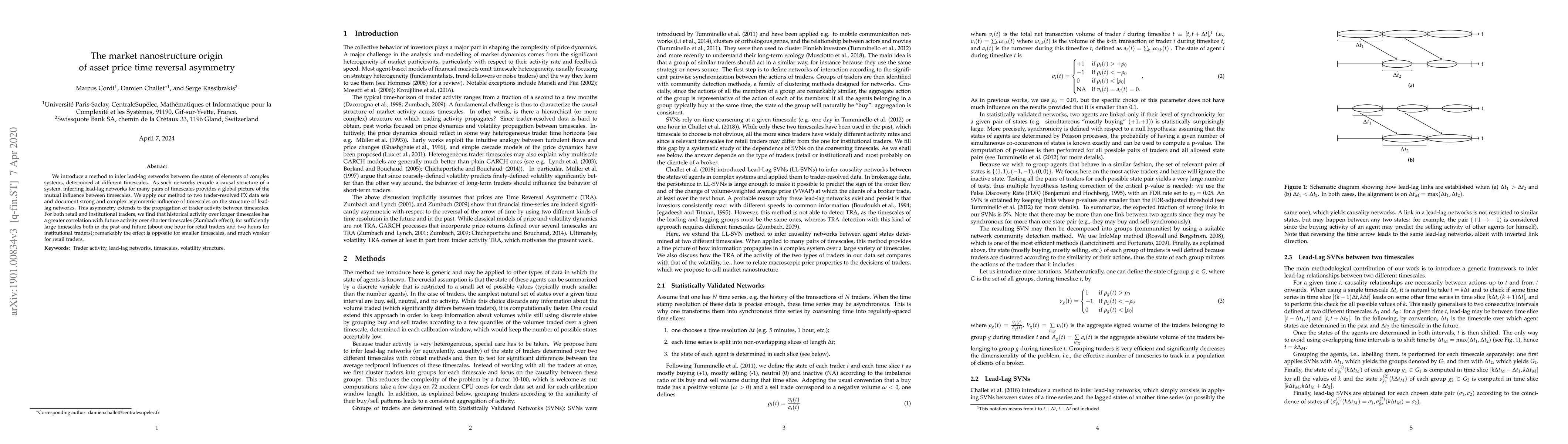

We introduce a framework to infer lead-lag networks between the states of elements of complex systems, determined at different timescales. As such networks encode the causal structure of a system, i...

We propose a minimal model of the secured interbank network able to shed light on recent money markets puzzles. We find that excess liquidity emerges due to the interactions between the reserves and l...

Using the secured transactions recorded within the Money Markets Statistical Reporting database of the European Central Bank, we test several stylized facts regarding interbank market of the 47 larges...

Reinforcement learning works best when the impact of the agent's actions on its environment can be perfectly simulated or fully appraised from available data. Some systems are however both hard to sim...

Decentralized lending protocols within the decentralized finance ecosystem enable the lending and borrowing of crypto-assets without relying on traditional intermediaries. Interest rates in these prot...

This paper investigates real-time detection of spoofing activity in limit order books, focusing on cryptocurrency centralized exchanges. We first introduce novel order flow variables based on multi-sc...

We enhance the Universal Portfolio Shrinkage Approximator (UPSA) of Kelly et al. (2023) by making it more robust with respect to estimation noise and covariate shift. UPSA optimizes the realized Sharp...

We study the optimal liquidation of a large position on Uniswap v2 and Uniswap v3 in discrete time. The instantaneous price impact is derived from the AMM pricing rule. Transient impact is modeled to ...