Academic Profile

Statistics

Similar Authors

Papers on arXiv

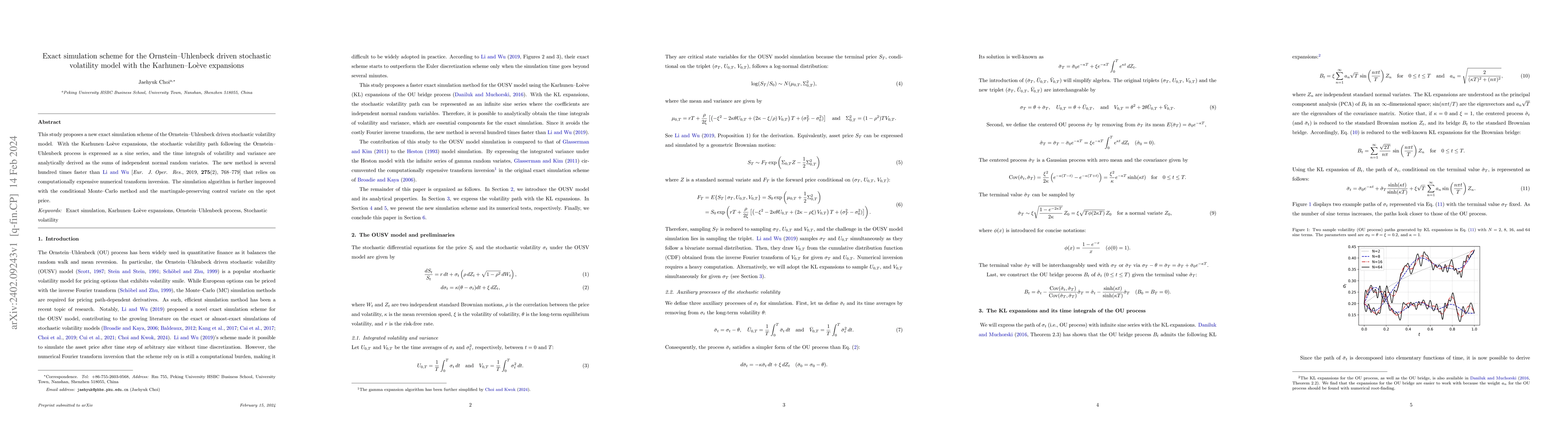

This study proposes a new exact simulation scheme of the Ornstein-Uhlenbeck driven stochastic volatility model. With the Karhunen-Lo\`eve expansions, the stochastic volatility path following the Orn...

Traditional art pricing models often lack fine measurements of painting content. This paper proposes a new content measurement: the Shannon information quantity measured by the singular value decomp...

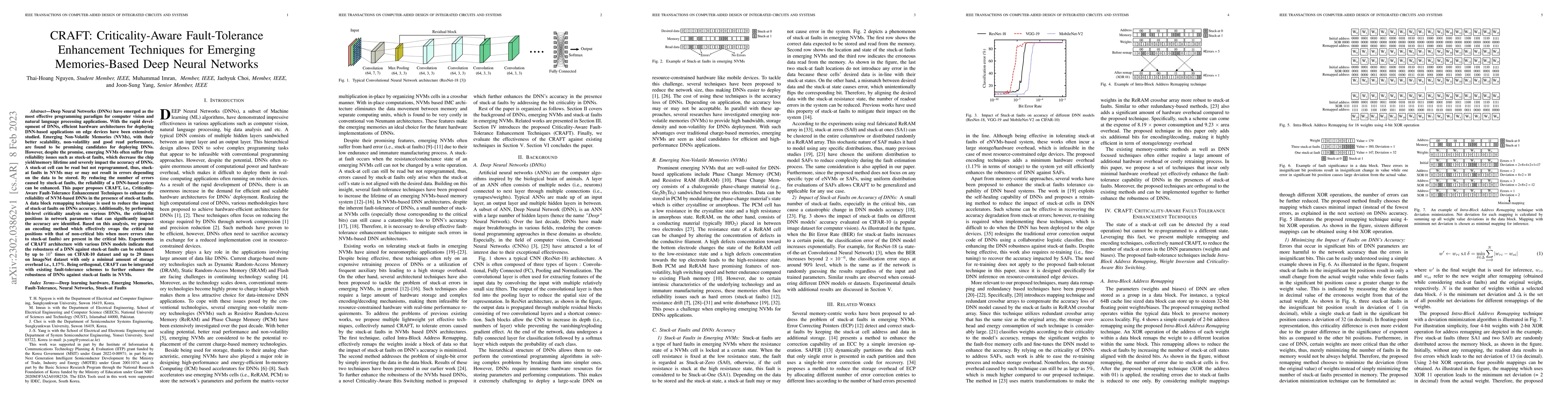

Deep Neural Networks (DNNs) have emerged as the most effective programming paradigm for computer vision and natural language processing applications. With the rapid development of DNNs, efficient ha...

Exact simulation schemes under the Heston stochastic volatility model (e.g., Broadie-Kaya and Glasserman-Kim) suffer from computationally expensive modified Bessel function evaluations. We propose a...

The stochastic-alpha-beta-rho (SABR) model has been widely adopted in options trading. In particular, the normal ($\beta=0$) SABR model is a popular model choice for interest rates because it allows...

Risk parity, also known as equal risk contribution, has recently gained increasing attention as a portfolio allocation method. However, solving portfolio weights must resort to numerical methods as ...

This paper proposes a lightweight method to attract users and increase views of the video by presenting personalized artistic media -- i.e, static thumbnails and animated GIFs. This method analyzes ...

This paper examines the effect of the political network of Chinese municipal leaders on the pricing of municipal corporate bonds. Using municipal leaders' working experience to measure the political...

To cope with the negative oil futures price caused by the COVID-19 recession, global commodity futures exchanges temporarily switched the option model from Black--Scholes to Bachelier in 2020. This ...

The literature on using yield curves to forecast recessions customarily uses 10-year--three-month Treasury yield spread without verification on the pair selection. This study investigates whether th...

The least squares Monte Carlo (LSM) algorithm proposed by Longstaff and Schwartz (2001) is widely used for pricing Bermudan options. The LSM estimator contains undesirable look-ahead bias, and the c...

We propose an efficient and reliable simulation scheme for the stochastic-alpha-beta-rho (SABR) model. The two challenges of the SABR simulation lie in sampling (i) the integrated variance conditional...