Academic Profile

Statistics

Similar Authors

Papers on arXiv

Using Malliavin calculus techniques we obtain formulas for computing Greeks under different rough Volterra stochastic volatility models. In particular we obtain formulas for rough versions of Stein-...

In this paper we study nonlinear partial differential equations (PDEs) that are used to model different value adjustments denoted generally as xVA. These adjustments are nowadays commonly added to t...

Rough Volterra volatility models are a progressive and promising field of research in derivative pricing. Although rough fractional stochastic volatility models already proved to be superior in real...

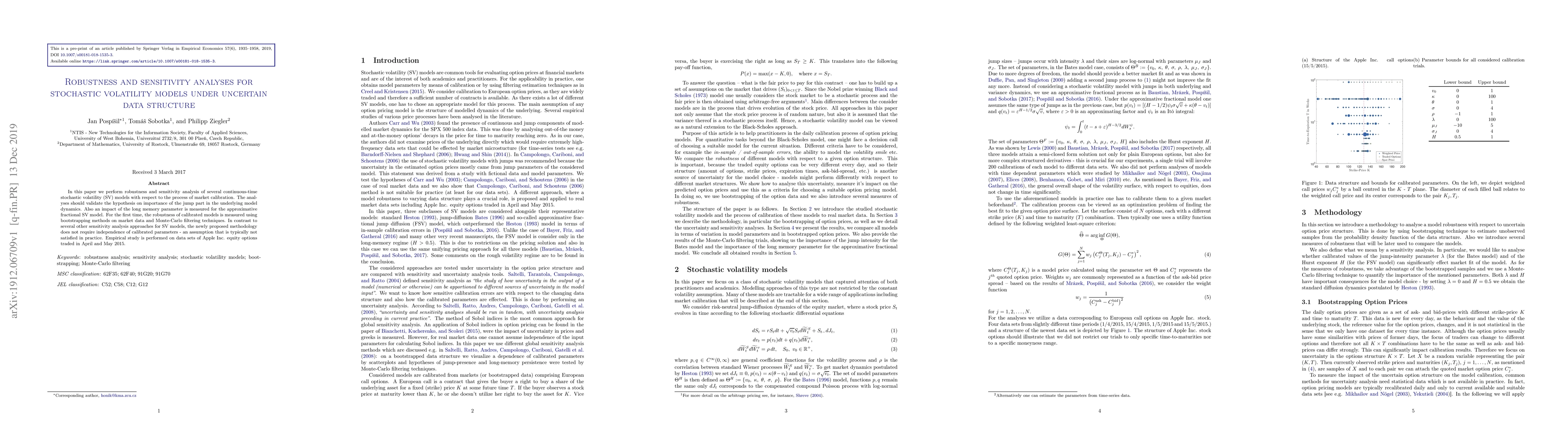

In this paper, we analyze the robustness and sensitivity of various continuous-time rough Volterra stochastic volatility models in relation to the process of market calibration. Model robustness is ...

In this paper we study partial differential equations (PDEs) that can be used to model value adjustments. Different value adjustments denoted generally as xVA are nowadays added to the risk-free fin...

In this paper we perform robustness and sensitivity analysis of several continuous-time stochastic volatility (SV) models with respect to the process of market calibration. The analyses should valid...

In this paper we study both analytic and numerical solutions of option pricing equations using systems of orthogonal polynomials. Using a Galerkin-based method, we solve the parabolic partial difere...

Isogeometric analysis is a recently developed computational approach that integrates finite element analysis directly into design described by non-uniform rational B-splines (NURBS). In this paper w...

The research presented in this article provides an alternative option pricing approach for a class of rough fractional stochastic volatility models. These models are increasingly popular between aca...

In this paper we derive a generic decomposition of the option pricing formula for models with finite activity jumps in the underlying asset price process (SVJ models). This is an extension of the we...

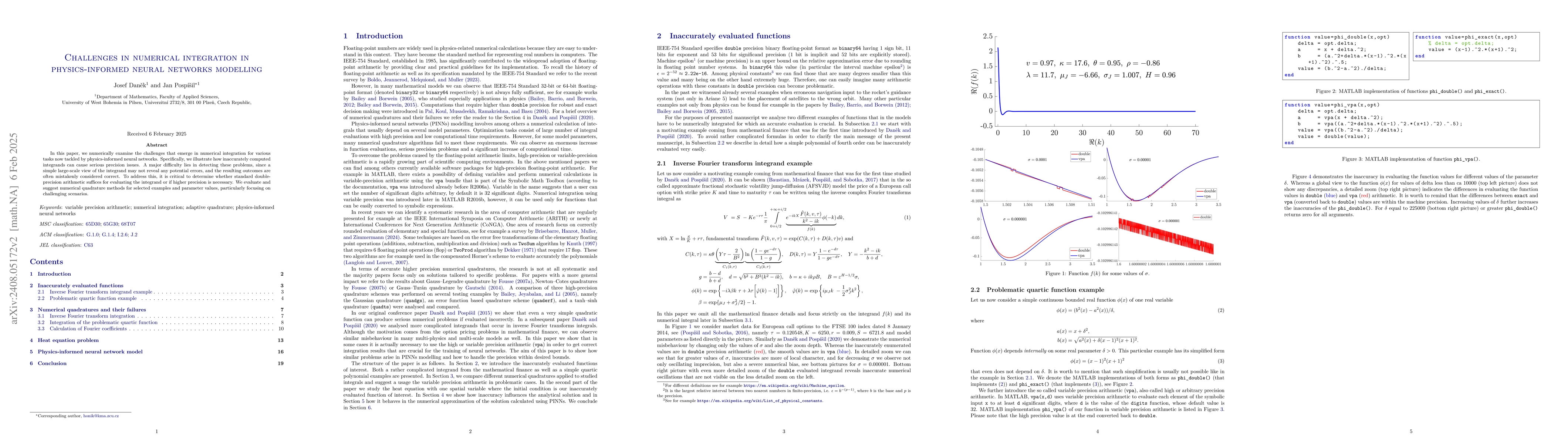

In this paper we numerically analyse problems that arise in numerical integration used in various problems that are nowadays being solved by physics-informed neural networks. In particular we show how...