Academic Profile

Statistics

Similar Authors

Papers on arXiv

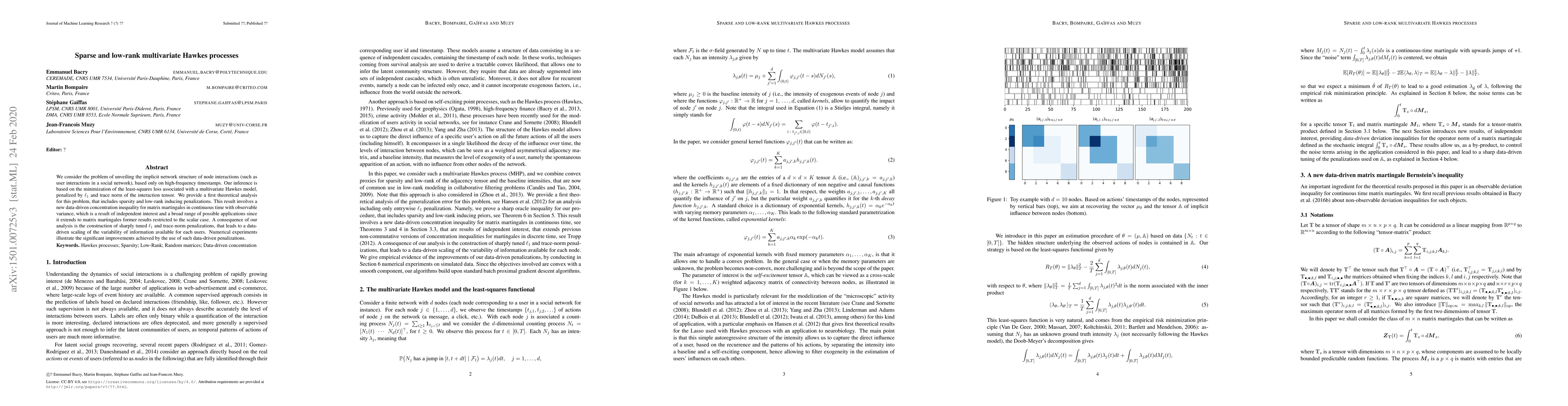

We consider the problem of unveiling the implicit network structure of node interactions (such as user interactions in a social network), based only on high-frequency timestamps. Our inference is ba...

We consider the problem of short-term forecasting of surface wind speed probability distribution. Our approach consists in predicting the parameters of a given probability density function by traini...

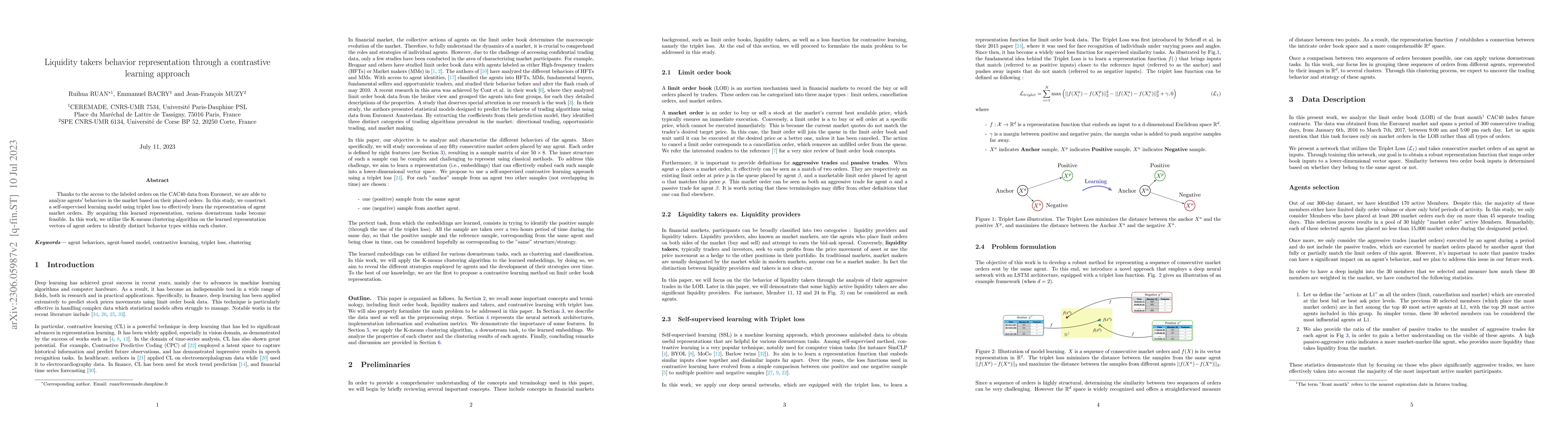

Thanks to the access to the labeled orders on the CAC40 data from Euronext, we are able to analyze agents' behaviors in the market based on their placed orders. In this study, we construct a self-su...

The bid-ask spread, which is defined by the difference between the best selling price and the best buying price in a Limit Order Book at a given time, is a crucial factor in the analysis of financia...

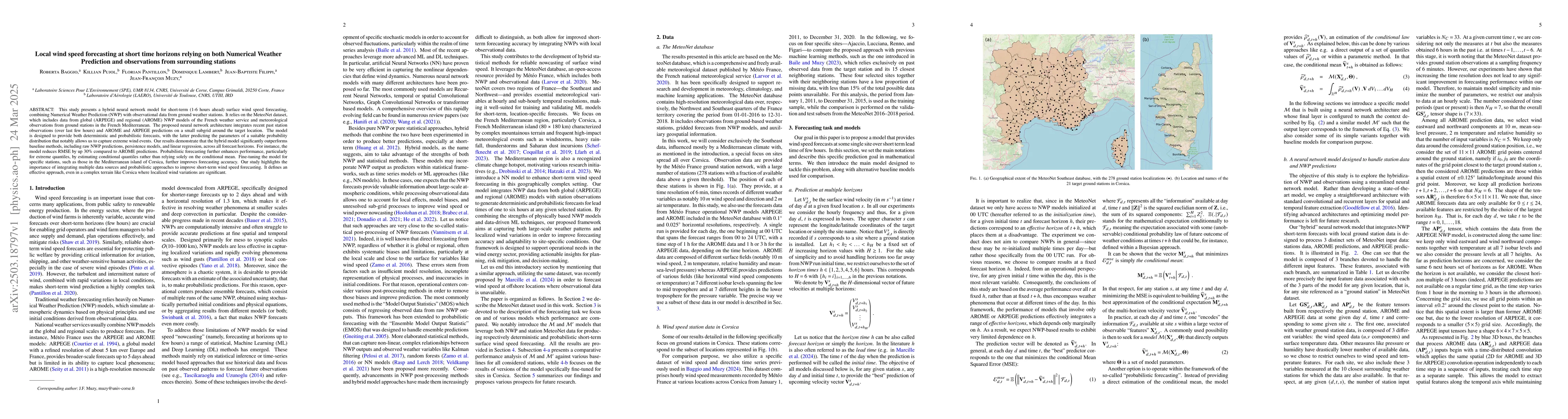

In this paper, we address the issue of short-term wind speed prediction at a given site. We show that, when one uses spatiotemporal information as provided by wind data of neighboring stations, one ...

We introduce a family of random measures $M_{H,T} (d t)$, namely log S-fBM, such that, for $H>0$, $M_{H,T}(d t) = e^{\omega_{H,T}(t)} d t$ where $\omega_{H,T}(t)$ is a Gaussian process that can be c...

Tick sizes not only influence the granularity of the price formation process but also affect market agents' behavior. We investigate the disparity in the microstructural properties of the Limit Order ...

This study presents a hybrid neural network model for short-term (1-6 hours ahead) surface wind speed forecasting, combining Numerical Weather Prediction (NWP) with observational data from ground weat...

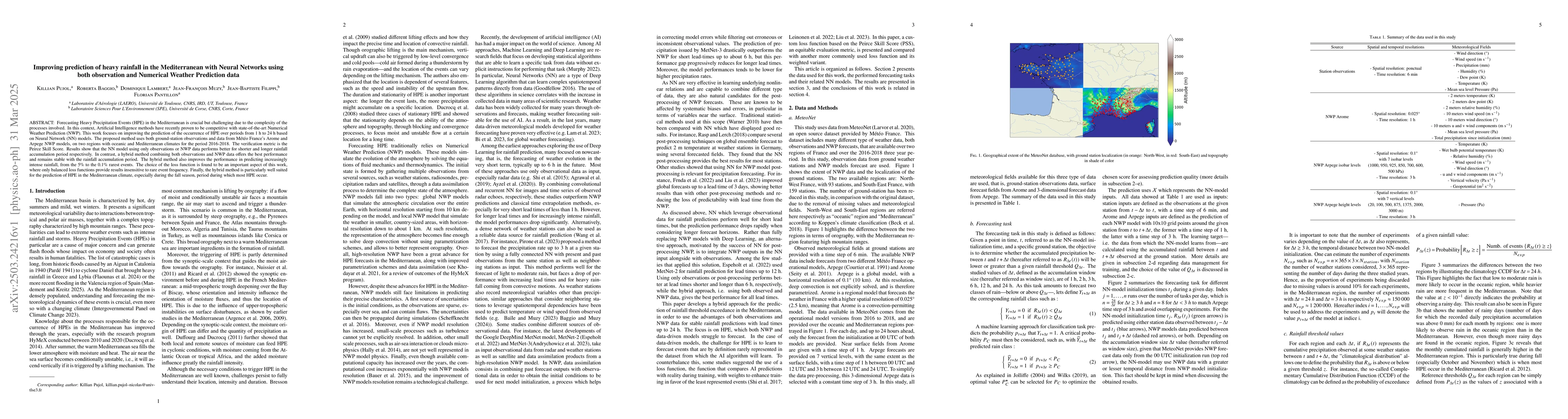

Forecasting Heavy Precipitation Events (HPE) in the Mediterranean is crucial but challenging due to the complexity of the processes involved. In this context, Artificial Intelligence methods have rece...

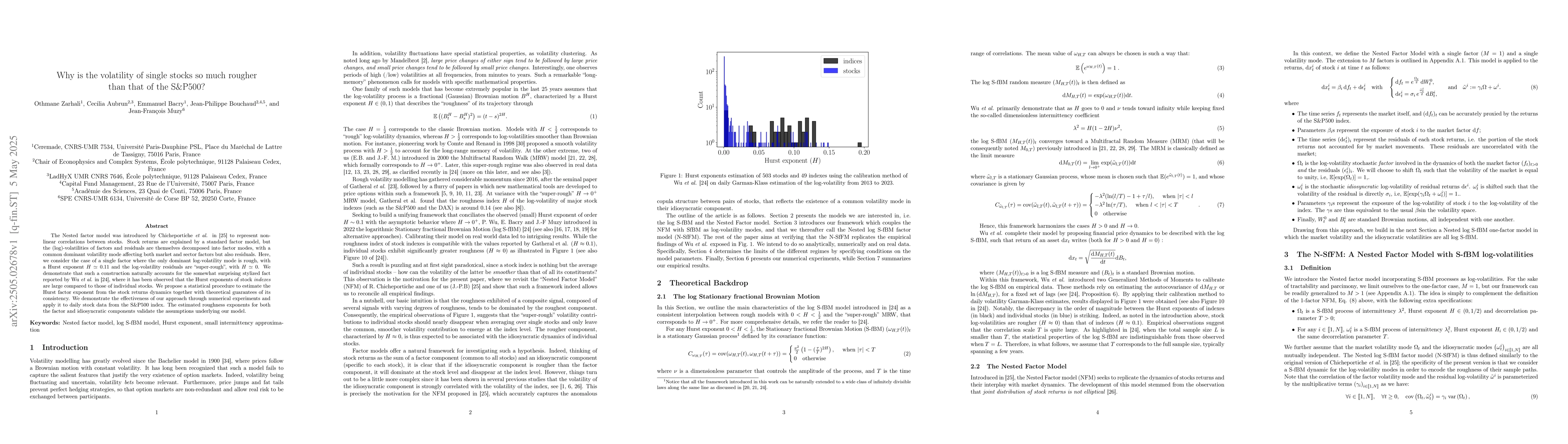

The Nested factor model was introduced by Chicheportiche et al. to represent non-linear correlations between stocks. Stock returns are explained by a standard factor model, but the (log)-volatilities ...

This paper introduces KANFormer, a novel deep-learning-based model for predicting the time-to-fill of limit orders by leveraging both market- and agent-level information. KANFormer combines a Dilated ...

We introduce the multivariate Log S-fBM model (mLog S-fBM), extending the univariate framework proposed by Wu \textit{et al.} to the multidimensional setting. We define the multidimensional Stationary...

This study compares two methodological approaches for predicting, at a given site, threshold exceedances of atmospheric variables such as temperature and wind speed: (i) direct probabilistic methods, ...