Academic Profile

Statistics

Similar Authors

Papers on arXiv

Let $X=(X_t, t\geq 0)$ be a superprocess in a random environment described by a Gaussian noise $W=\{W(t,x), t\geq 0, x\in \mathbb{R}^d\}$ white in time and colored in space with correlation kernel $...

In this paper, we first prove that the mean-field stochastic linear quadratic (MFSLQ) control problem with random coefficients has a unique optimal control and derive a preliminary stochastic maximu...

A linear quadratic (LQ) stochastic optimization system involving large population, which is driven by forward-backward stochastic differential equation (FBSDE), is investigated in this paper. Agents...

This paper studies a class of continuous-time linear quadratic (LQ) mean-field game problems. We develop two system transformation data-driven algorithms to approximate the decentralized strategies ...

In this article, we consider a weighted mean-field control problem with jump-diffusion as its state process. The main difficulty is from the non-Lipschitz property of the coefficients. We overcome t...

Let $X=(X_t, t\geq 0)$ be a superprocess in a random environment described by a Gaussian noise $W^g=\{W^g(t,x), t\geq 0, x\in \mathbb{R}^d\}$ white in time and colored in space with correlation kern...

In this paper, we study a stochastic optimal control problem for a Markovian regime switching system, where the coefficients of the state equation and the cost functional are uncertain. First, we ob...

We prove a scaling limit theorem for two-type Galton-Waston branching processes with interaction. The limit theorem gives rise to a class of mixed state branching processes with interaction using to...

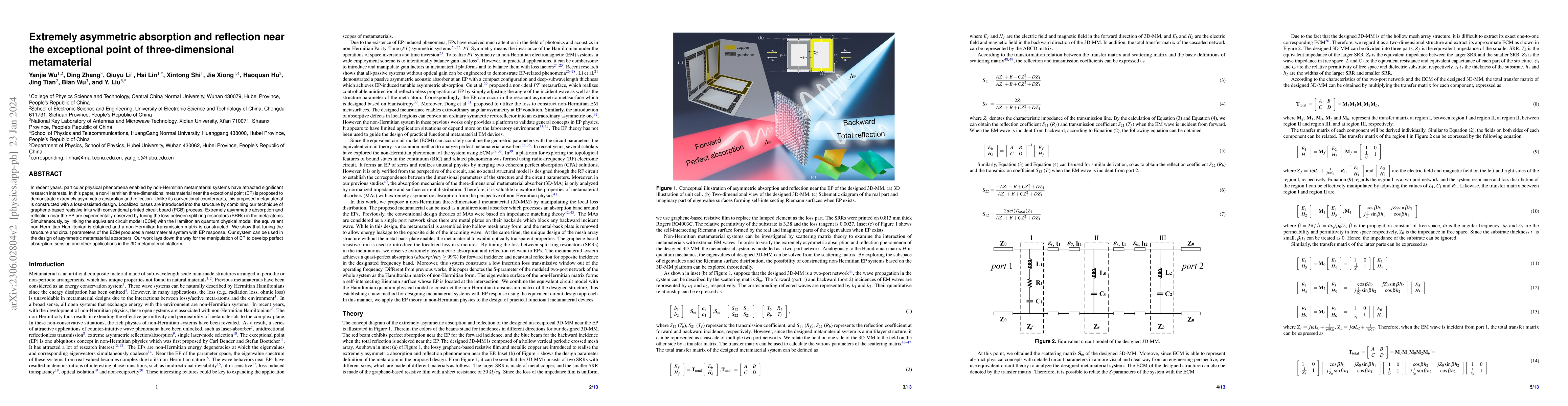

In recent years, particular physical phenomena enabled by non-Hermitian metamaterial systems have attracted significant research interests. In this paper, a non-Hermitian three-dimensional metamater...

This paper is concerned with a partially observed hybrid optimal control problem, where continuous dynamics and discrete events coexist and in particular, the continuous dynamics can be observed whi...

In this paper a martingale problem for super-Brownian motion with interactive branching is derived. The uniqueness of the solution to the martingale problem is obtained by using the pathwise uniquen...

Let $\{Z_n\}_{n\geq 0 }$ be a critical or subcritical $d$-dimensional branching random walk started from a Poisson random measure whose intensity measure is the Lebesugue measure on $\mathbb{R}^d$. ...

This paper is devoted to a global stochastic maximum principle for conditional mean-field forward-backward stochastic differential equations (FBSDEs, for short) with regime switching. The control do...

We study the optimal control problem for a weighted mean-field system. A new feature of the control problem is that the coefficients depend on the state process as well as its weighted measure and t...

In this paper, we study the multi-dimensional mean-field backward stochastic differential equations (BSDEs, for short) with quadratic growth. Under small terminal value, the existence and uniqueness...

In this paper, we consider a linear quadratic (LQ) leader-follower stochastic differential game for regime switching diffusions with mean-field interactions. One of the salient features of this pape...

In this paper, a class of non-Markovian forward-backward doubly stochastic systems is studied. By using the technique of functional It\^o (or path-dependent) calculus, the relationship between the s...

In this paper, we initiate the study of backward doubly stochastic differential equations (BDSDEs, for short) with quadratic growth. The existence, comparison, and stability results for one-dimensio...

Let $\{X_t\}_{t\geq0}$ be a $d$-dimensional critical super-Brownian motion started from a Poisson random measure whose intensity is the Lebesgue measure. Denote by $R_t:=\sup\{u>0: X_t(\{x\in\mathbb...

In this paper, we study a non-linear filtering problem in the presence of signal model uncertainty. The model ambiguity is characterized by a class of probability measures from which the true one is...

A general backward stochastic linear-quadratic optimal control problem is studied, in which both the state equation and the cost functional contain the nonhomogeneous terms. The main feature of the ...

The paper studies a class of quadratic optimal control problems for partially observable linear dynamical systems. In contrast to the full information case, the control is required to be adapted to ...

This paper proposes a class of neural ordinary differential equations parametrized by provably input-to-state stable continuous-time recurrent neural networks. The model dynamics are defined by cons...

This paper thoroughly investigates stochastic linear-quadratic optimal control problems with the Markovian regime switching system, where the coefficients of the state equation and the weighting mat...

Human Activity Recognition (HAR) plays a critical role in a wide range of real-world applications, and it is traditionally achieved via wearable sensing. Recently, to avoid the burden and discomfort...

This paper studies a nonlinear filtering problem over an infinite time interval. The signal to be estimated is driven by a stochastic partial differential equation involves unknown parameters. Based...

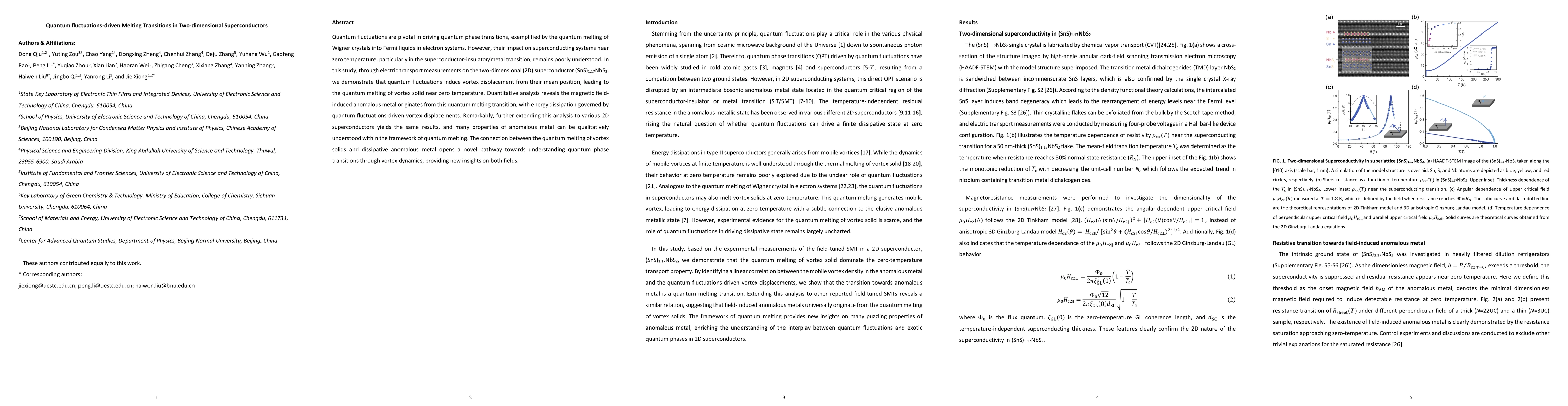

Fermi liquid theory forms the basis for our understanding of the majority of metals, which is manifested in the description of transport properties that the electrical resistivity goes as temperatur...

This paper is concerned with a backward stochastic linear-quadratic (LQ, for short) optimal control problem with deterministic coefficients. The weighting matrices are allowed to be indefinite, and ...

In this paper a martingale problem for super-Brownian motion with interactive branching is derived. The uniqueness of the solution to the martingale problem is obtained by using the pathwise uniquen...

A system of mutually interacting superprocesses with migration is constructed as the limit of a sequence of branching particle systems arising from population models. The uniqueness in law of the su...

This paper deals with partially-observed optimal control problems for the state governed by stochastic differential equation with delay. We develop a stochastic maximum principle for this kind of op...

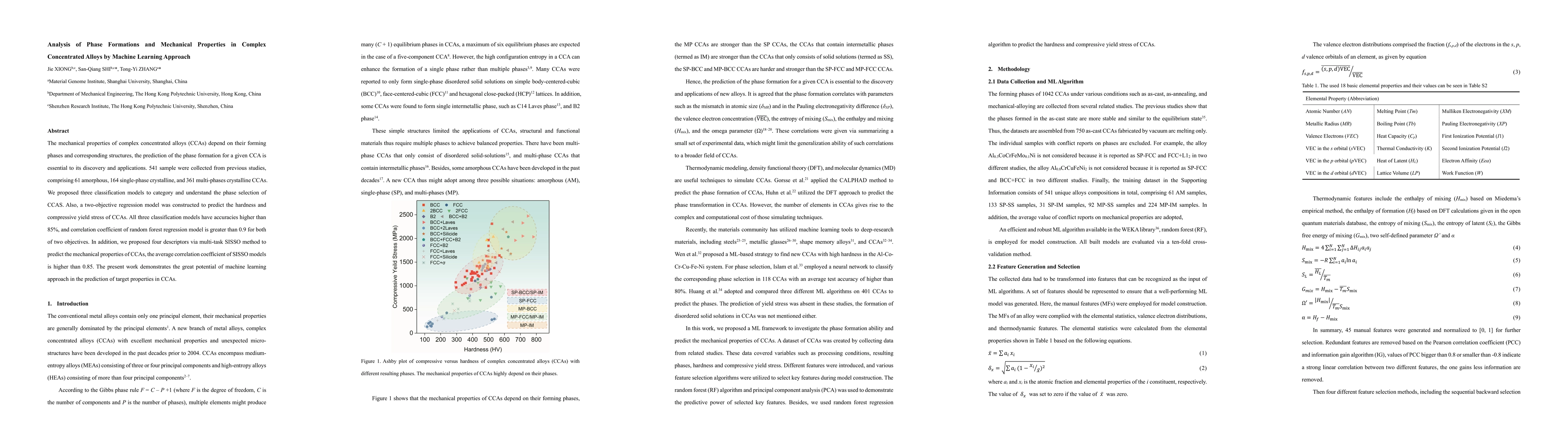

The mechanical properties of complex concentrated alloys (CCAs) depend on their forming phases and corresponding structures, the prediction of the phase formation for a given CCA is essential to its...

In this paper we establish the strong existence, pathwise uniqueness and a comparison theorem to a stochastic partial differential equation driven by Gaussian colored noise with non-Lipschitz drift,...

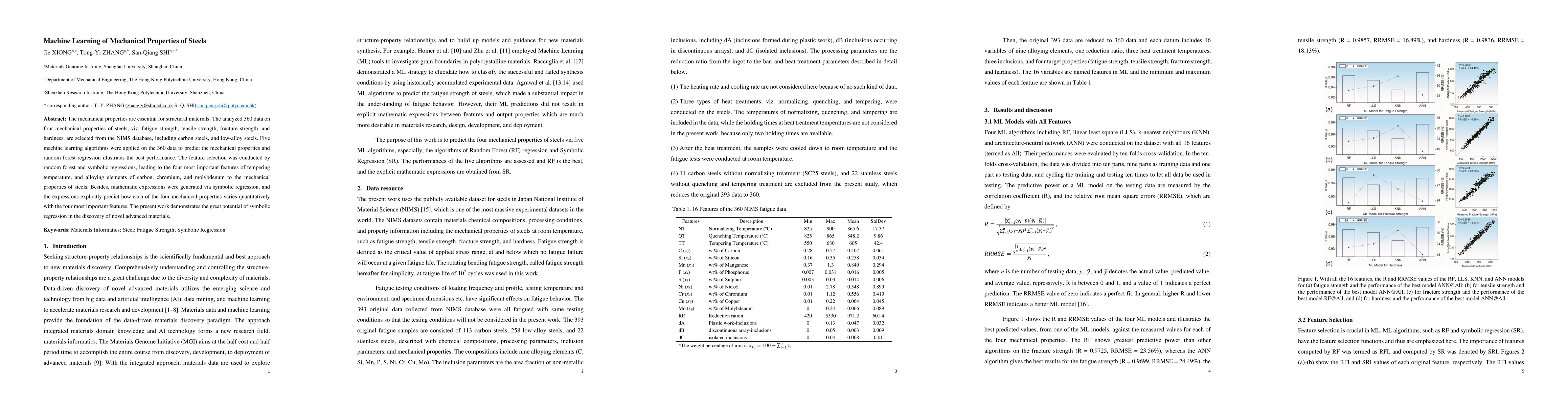

The mechanical properties are essential for structural materials. The analyzed 360 data on four mechanical properties of steels, viz. fatigue strength, tensile strength, fracture strength, and hardn...

We study a two-dimensional process $(X, Y)$ arising as the unique nonnegative solution to a pair of stochastic differential equations driven by independent Brownian motions and compensated spectrall...

Backward doubly stochastic Volterra integral equations (BDSVIEs, for short) are introduced and studied systematically. Well-posedness of BDSVIEs in the sense of introduced M-solutions is established...

This paper is concerned with a constrained stochastic linear-quadratic optimal control problem, in which the terminal state is fixed and the initial state is constrained to lie in a stochastic linea...

After decades of explorations, suffering from low critical temperature and subtle nature, whether a metallic ground state exists in a two-dimensional system beyond Anderson localization is still a m...

We consider a system of two stochastic differential equations (SDEs) with negative two-way interactions driven by Brownian motions and spectrally positive $\alpha$-stable random measures. Such a SDE s...

Despite a long history of Nernst effect in superconductors, a satisfactory theory on its amplitude in vortex liquid phase is still absent. The central quantity of vortex Nernst signals is the entropy ...

Recent years have witnessed the use of pervasive wireless signals (e.g., Wi-Fi, RFID, and mmWave) for sensing purposes. Due to its non-intrusive characteristic, wireless sensing plays an important rol...

In this paper, we study an optimal stopping problem in the presence of model uncertainty and regime switching. The max-min formulation for robust control and the dynamic programming approach are adopt...

This paper investigates a linear quadratic stochastic optimal control (LQSOC) problem with partial information. Firstly, by introducing two Riccati equations and a backward stochastic differential equ...

This paper investigates a zero-sum stochastic linear-quadratic (SLQ, for short) Stackelberg differential game problem, where the coefficients of the state equation and the weighting matrices in the pe...

This paper investigates a two-person non-homogeneous linear-quadratic stochastic differential game (LQ-SDG, for short) in an infinite horizon for a system regulated by a time-invariant Markov chain. B...

We apply a Lindeberg principle under the Markov process setting to approximate the Wright-Fisher model with neutral $r$-alleles using a diffusion process, deriving an error rate based on a function cl...

Quantum fluctuations are pivotal in driving quantum phase transitions, exemplified by the quantum melting of Wigner crystals into Fermi liquids in electron systems. However, their impact on supercondu...

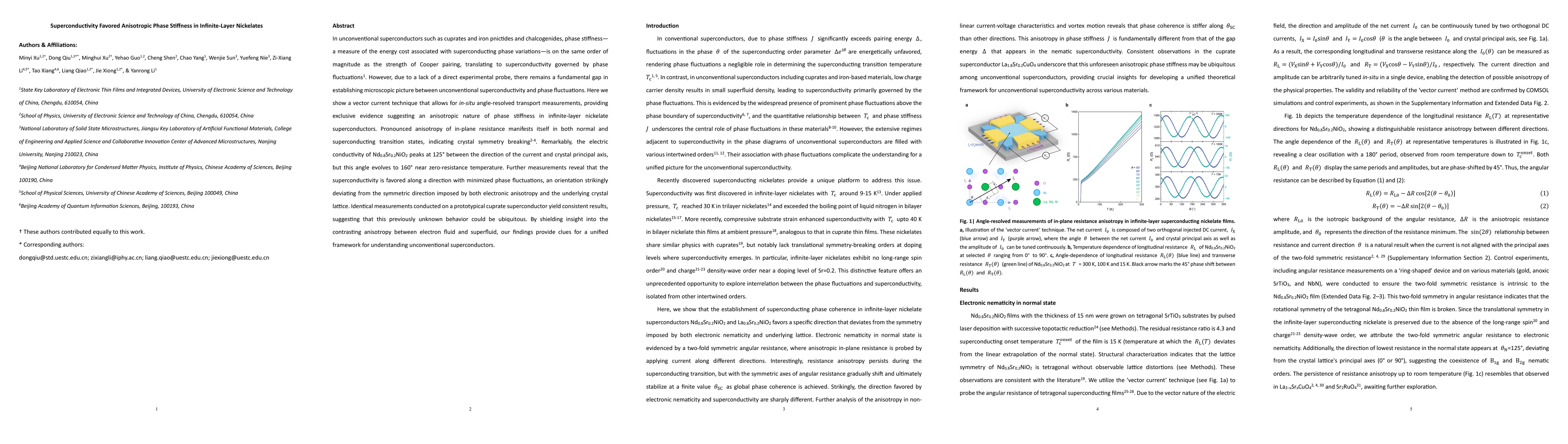

In unconventional superconductors such as cuprates and iron pnictides and chalcogenides, phase stiffness - a measure of the energy cost associated with superconducting phase variations - is on the sam...

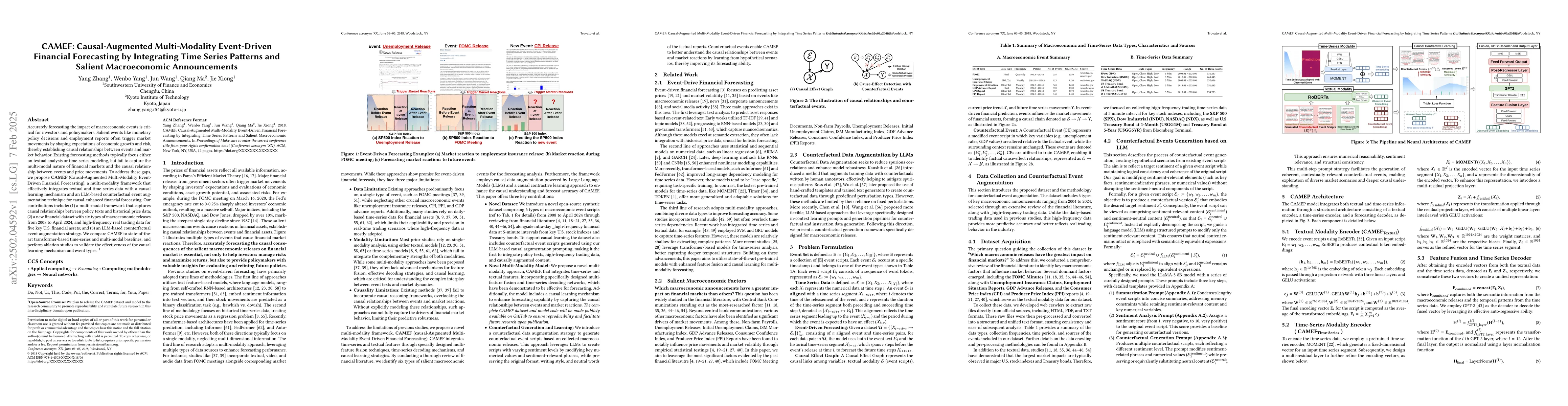

Accurately forecasting the impact of macroeconomic events is critical for investors and policymakers. Salient events like monetary policy decisions and employment reports often trigger market movement...

This paper develops a comparison theorem for viscosity solutions of a new class of Hamilton-Jacobi-Bellman (HJB) equations, which is used to solve the separated problem governed by the K-S equation in...

In this paper, we study the linear-quadratic control problem for mean-field backward stochastic differential equations (MF-BSDE) with random coefficients. We first derive a preliminary stochastic maxi...

This paper studies a stochastic mean-field linear-quadratic optimal control problem with random coefficients. The state equation is a general linear stochastic differential equation with mean-field te...

In this article, we consider a stochastic linear quadratic control problem with partial observation. A near optimal control in the weak formulation is characterized. The main features of this paper ar...

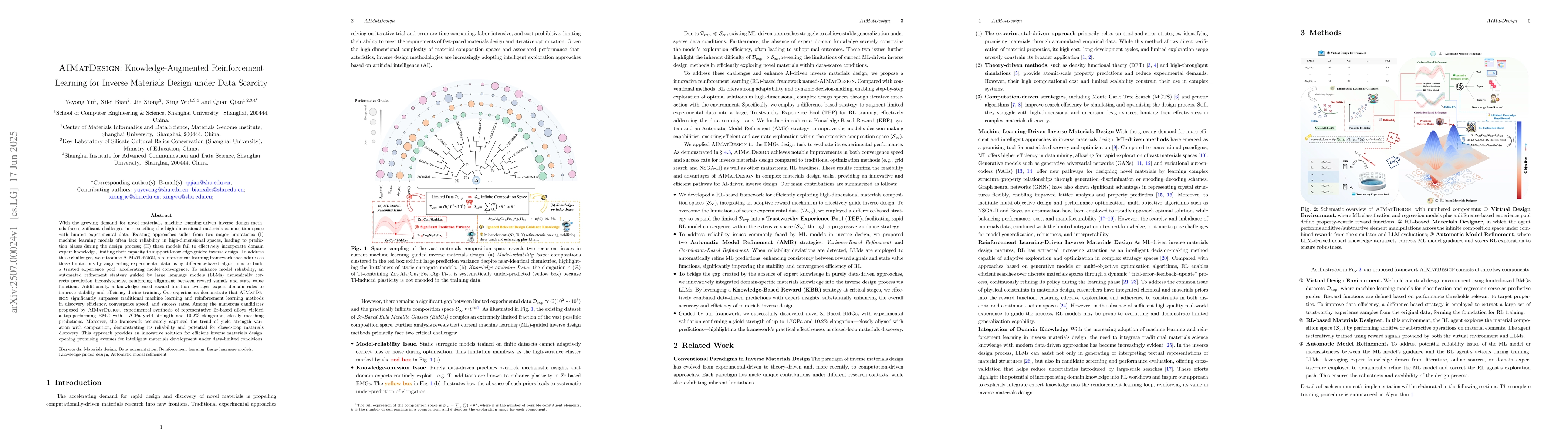

With the growing demand for novel materials, machine learning-driven inverse design methods face significant challenges in reconciling the high-dimensional materials composition space with limited exp...

We study equilibrium feedback strategies for a family of dynamic mean-variance problems with competition among a large group of agents. We assume that the time horizon is random and each agent's risk ...

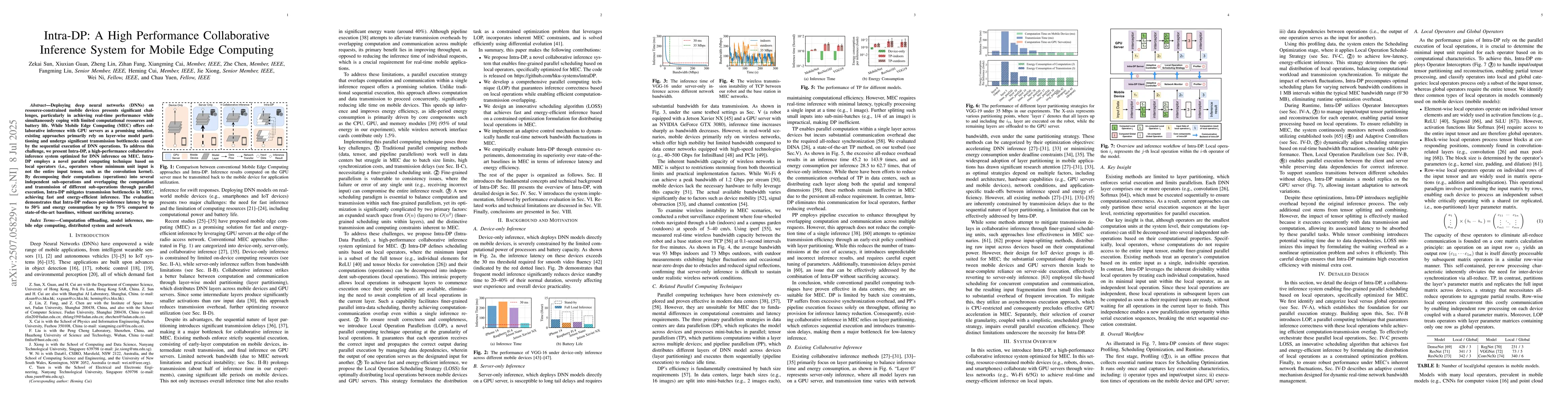

Deploying deep neural networks (DNNs) on resource-constrained mobile devices presents significant challenges, particularly in achieving real-time performance while simultaneously coping with limited c...

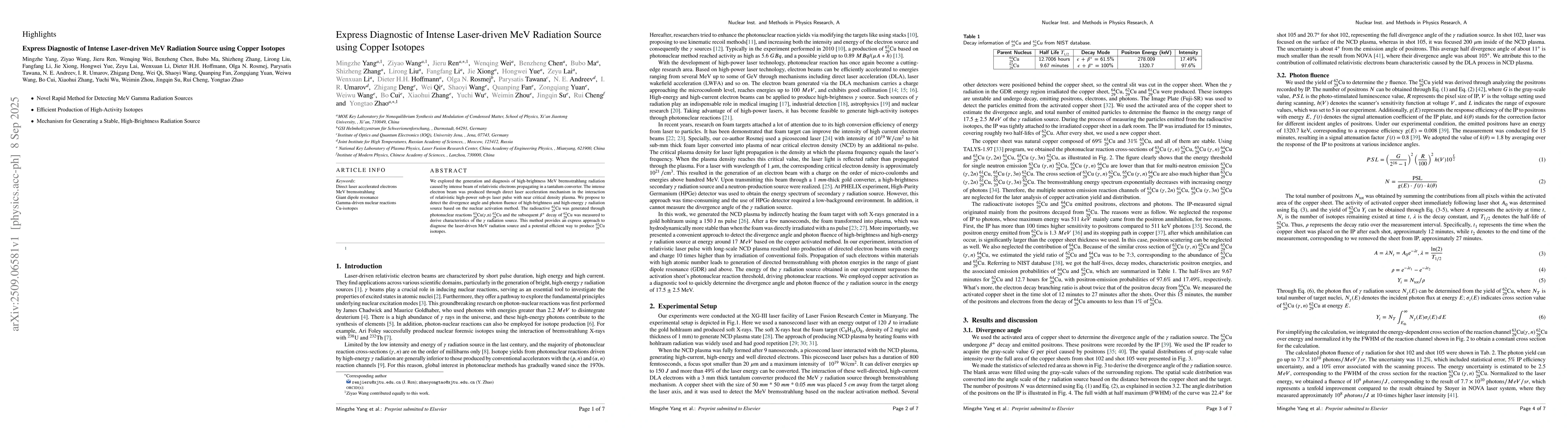

We explored the generation and diagnosis of high-brightness MeV bremsstrahlung radiation caused by intense beam of relativistic electrons propagating in a tantalum converter. The intense electron beam...

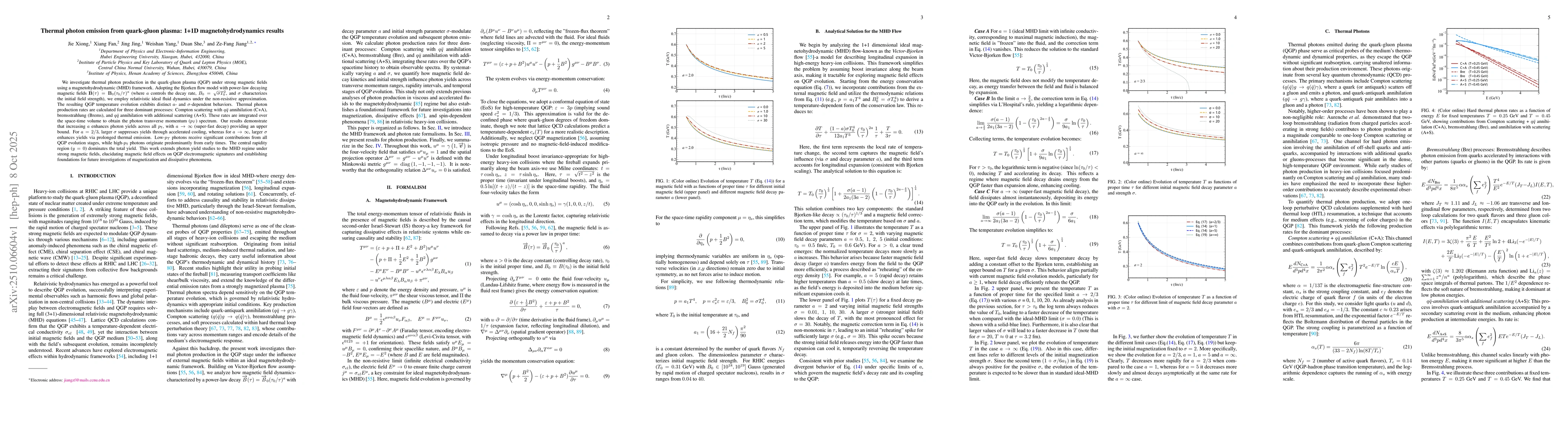

We investigate thermal photon production in the quark-gluon plasma (QGP) under strong magnetic fields using a magnetohydrodynamic (MHD) framework. Adopting the Bjorken flow model with power-law decayi...

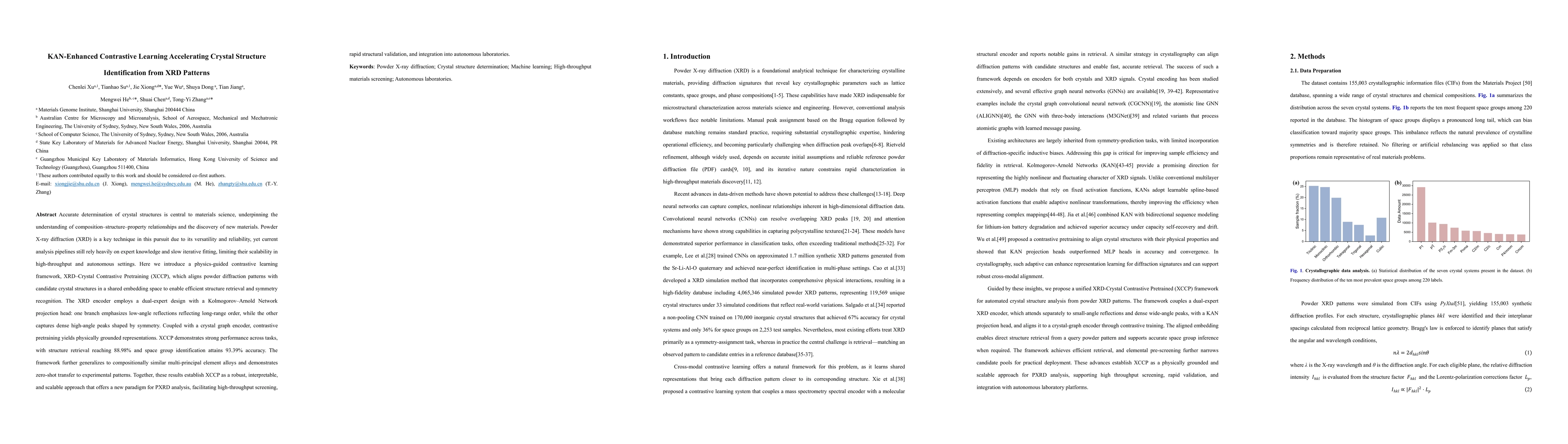

Accurate determination of crystal structures is central to materials science, underpinning the understanding of composition-structure-property relationships and the discovery of new materials. Powder ...

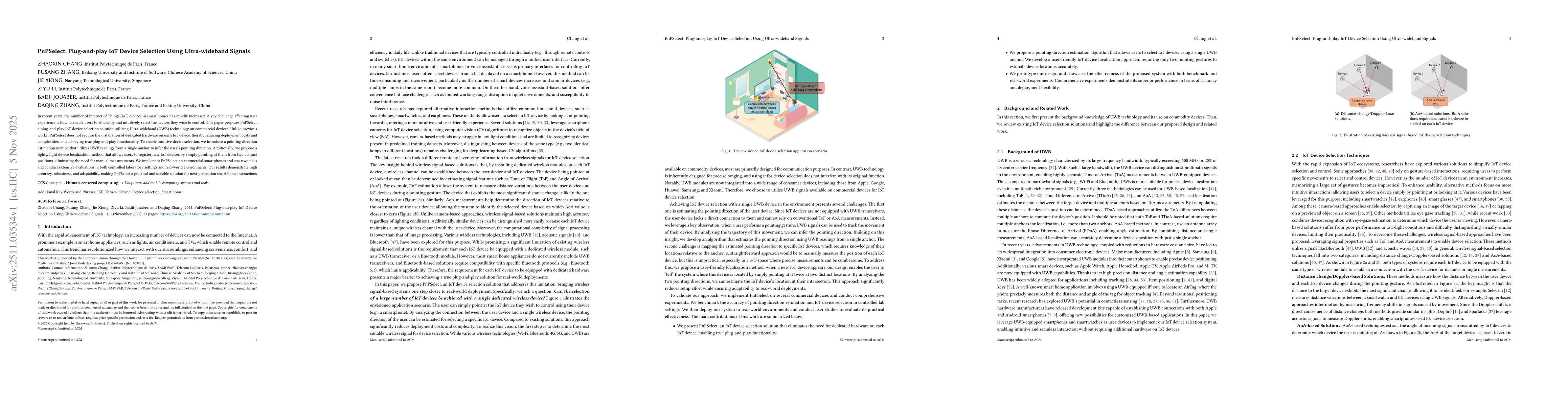

In recent years, the number of Internet of Things (IoT) devices in smart homes has rapidly increased. A key challenge affecting user experience is how to enable users to efficiently and intuitively se...

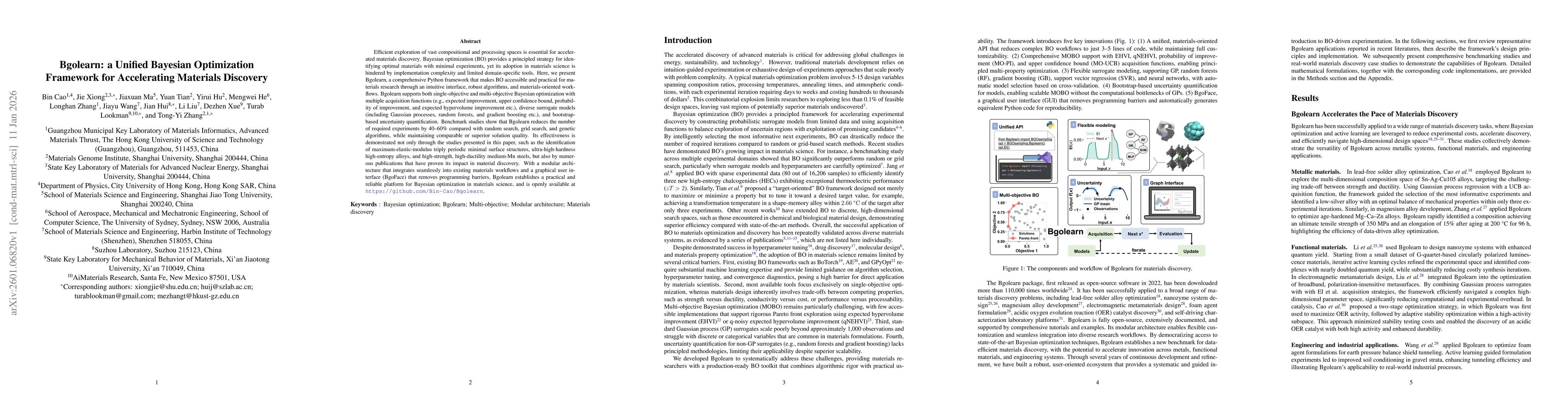

Efficient exploration of vast compositional and processing spaces is essential for accelerated materials discovery. Bayesian optimization (BO) provides a principled strategy for identifying optimal ma...

This paper investigates a cone-constrained two-player zero-sum stochastic linear-quadratic (SLQ) differential game for stochastic differential equations (SDEs) with regime switching and random coeffic...

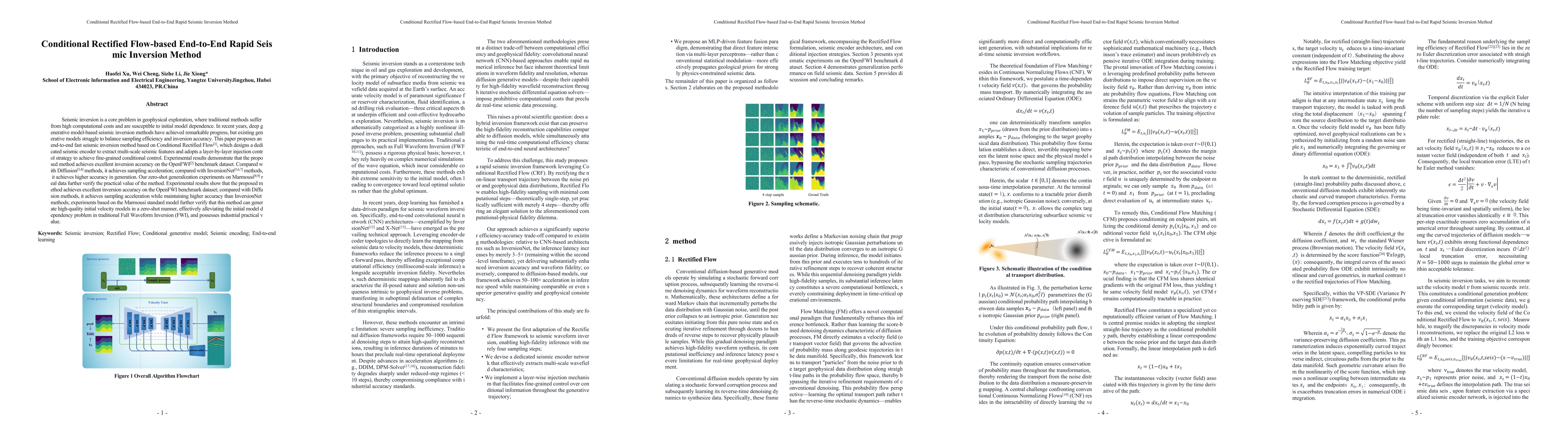

Seismic inversion is a core problem in geophysical exploration, where traditional methods suffer from high computational costs and are susceptible to initial model dependence. In recent years, deep ge...

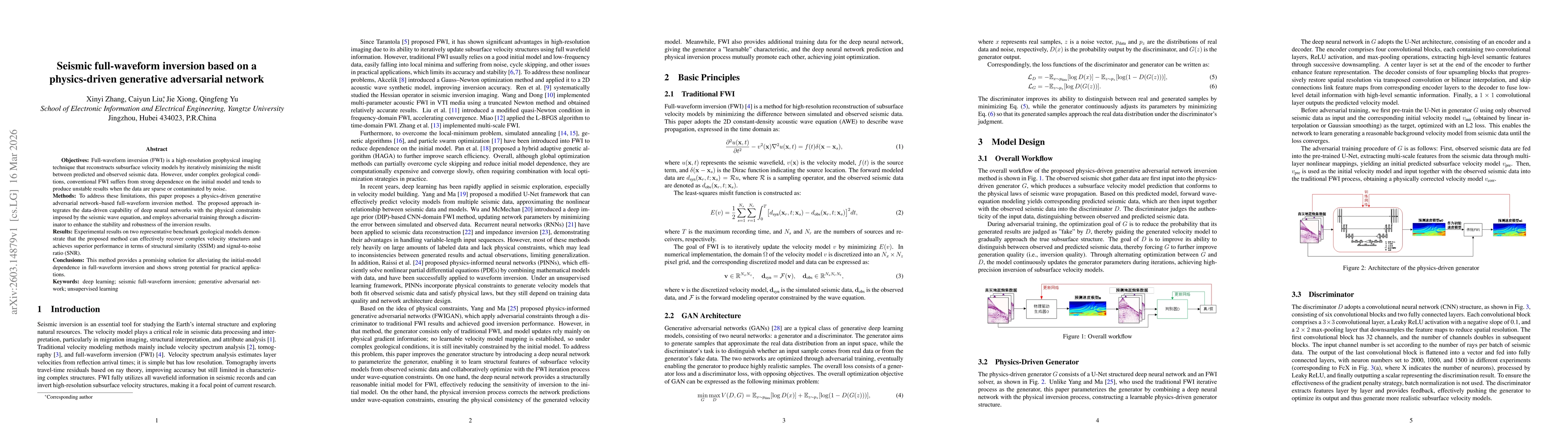

Objectives: Full-waveform inversion (FWI) is a high-resolution geophysical imaging technique that reconstructs subsurface velocity models by iteratively minimizing the misfit between predicted and obs...

Implicit Neural Representations (INRs) have emerged as a powerful paradigm for representing continuous signals independently of grid resolution. In this paper, we propose a high-fidelity neural compre...

In this paper, we study a two-dimensional process arising as the unique nonnegative solution to a system of two stochastic differential equations (SDEs) with mutually enhancing two-way interactions dr...

Seismic full-waveform inversion is a core technology for obtaining high-resolution subsurface model parameters. However, its highly nonlinear characteristics and strong dependence on the initial model...

Phase-field simulations provide mechanistic descriptions of microstructure evolution, but repeated high-fidelity integration over long horizons and broad parameter spaces remains computationally expen...

This paper studies finite-horizon stochastic linear-quadratic optimal control problems with random coefficients and Poisson jumps, where the weighting matrices may be random and indefinite. Under a un...

This paper studies a stochastic mean-field linear-quadratic Stackelberg differential game with random coefficients. The interaction between mean-field terms and random coefficients precludes the direc...

This paper derives a stochastic maximum principle (SMP) for partially observed jump-diffusion systems whose observations are multivariate counting processes with state-dependent intensities. By introd...

In this paper, we study the strong uniqueness problem for the mutually catalytic super-Markov chain, which is a two-dimensional degenerate stochastic differential equation with Hölder continuous coeff...

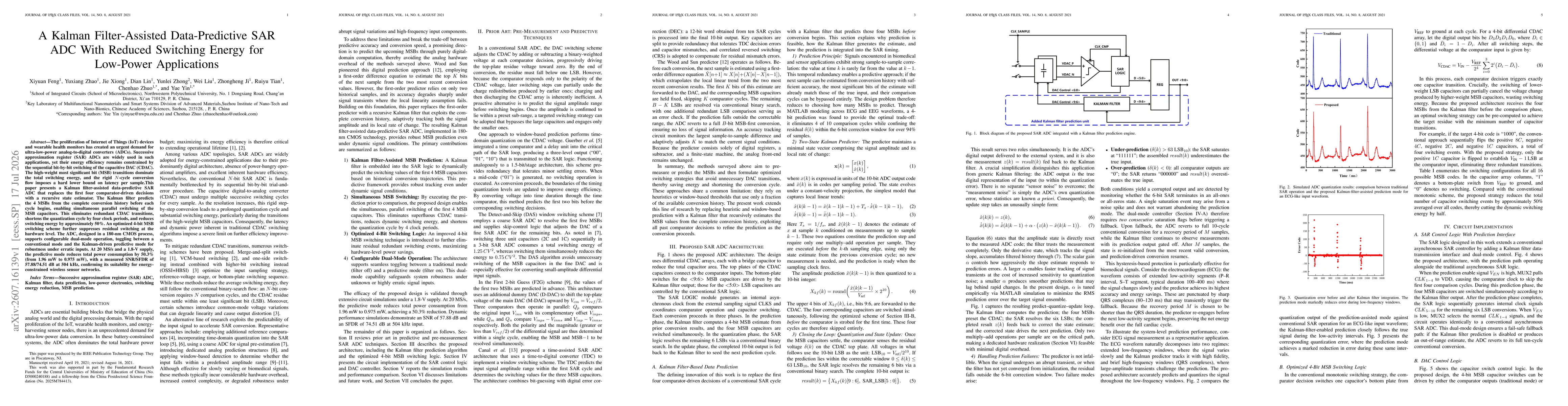

The proliferation of Internet of Things (IoT) devices and wearable health monitors has created an urgent demand for ultra-low-power analog-to-digital converters (ADCs). Successive approximation regist...