Academic Profile

Statistics

Similar Authors

Papers on arXiv

We prove the existence of a continuous-time Radner equilibrium with multiple agents and transaction costs. The agents are incentivized to trade towards a targeted number of shares throughout the tra...

In a continuous-time Kyle setting, we prove global existence of an equilibrium when the insider faces a terminal trading constraint. We prove that our equilibrium model produces output consistent wi...

We prove the existence of an incomplete Radner equilibrium in a model with exponential investors and an endogenous noise tracker. We analyze a coupled system of ODEs and reduce it to a system of two...

This paper presents an equilibrium model of dynamic trading, learning, and pricing by strategic investors with trading targets and price impact. Since trading targets are private, rebalancers and li...

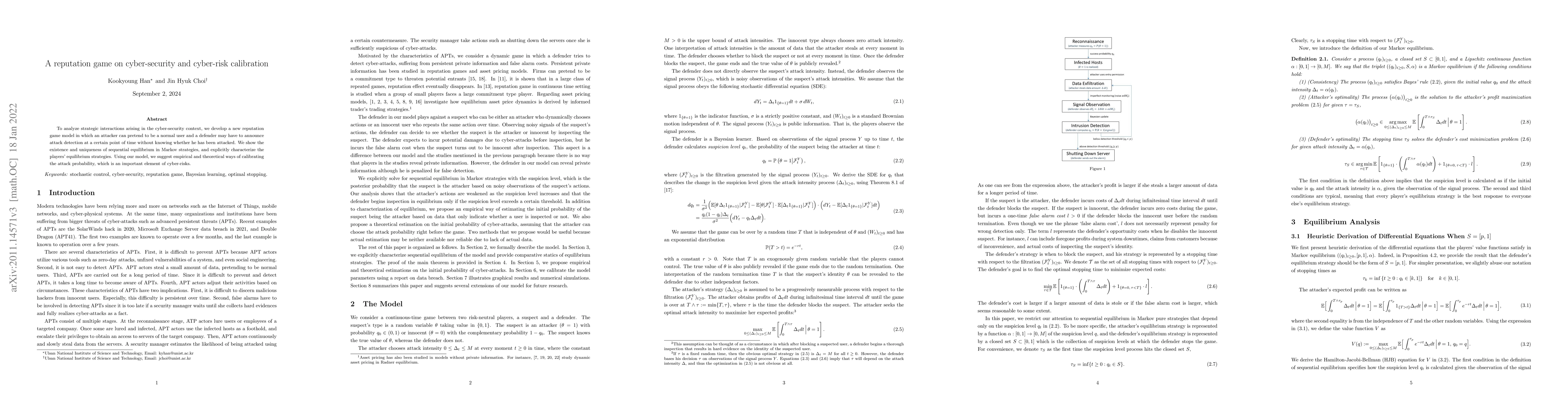

To analyze strategic interactions arising in the cyber-security context, we develop a new reputation game model in which an attacker can pretend to be a normal user and a defender may have to announ...

We solve in closed-form an equilibrium model in which a finite number of exponential investors continuously consume and trade with price-impact. Compared to the analogous Pareto-efficient equilibriu...

This paper presents a continuous-time model of intraday trading, pricing, and liquidity with dynamic TWAP and VWAP benchmarks. The model is solved in closed-form for the competitive equilibrium and ...

This paper investigates the optimal investment problem in a market with two types of illiquidity: transaction costs and search frictions. Extending the framework established by arXiv:2101.09936, we an...

We prove the existence of a Radner equilibrium in a model with population growth and analyze the effects on asset prices. A finite population of agents grows indefinitely at a Poisson rate, while rece...

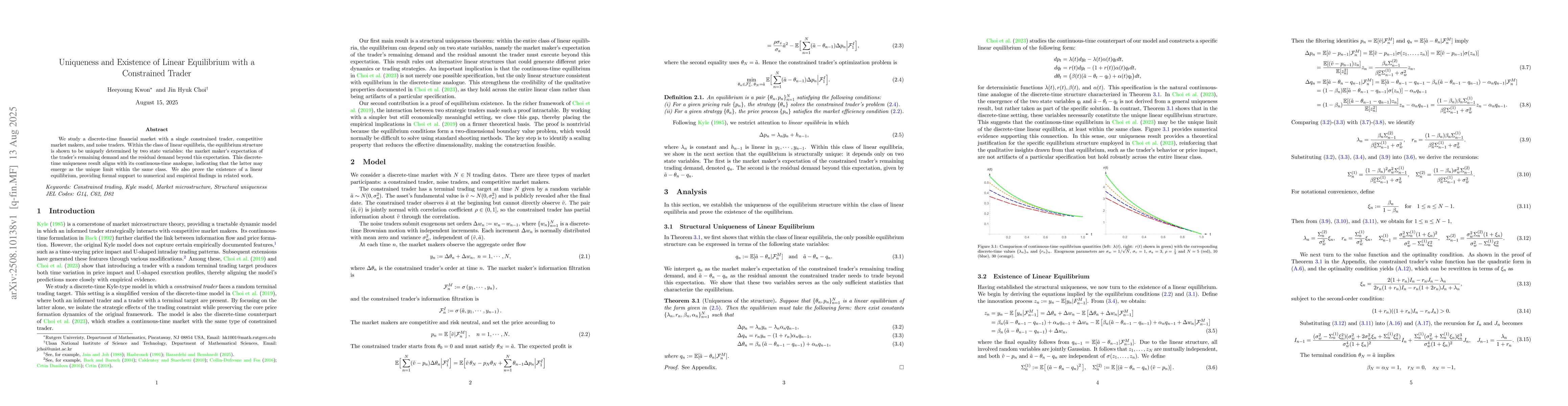

We study a discrete-time financial market with a single constrained trader, competitive market makers, and noise traders. Within the class of linear equilibria, the equilibrium structure is shown to b...

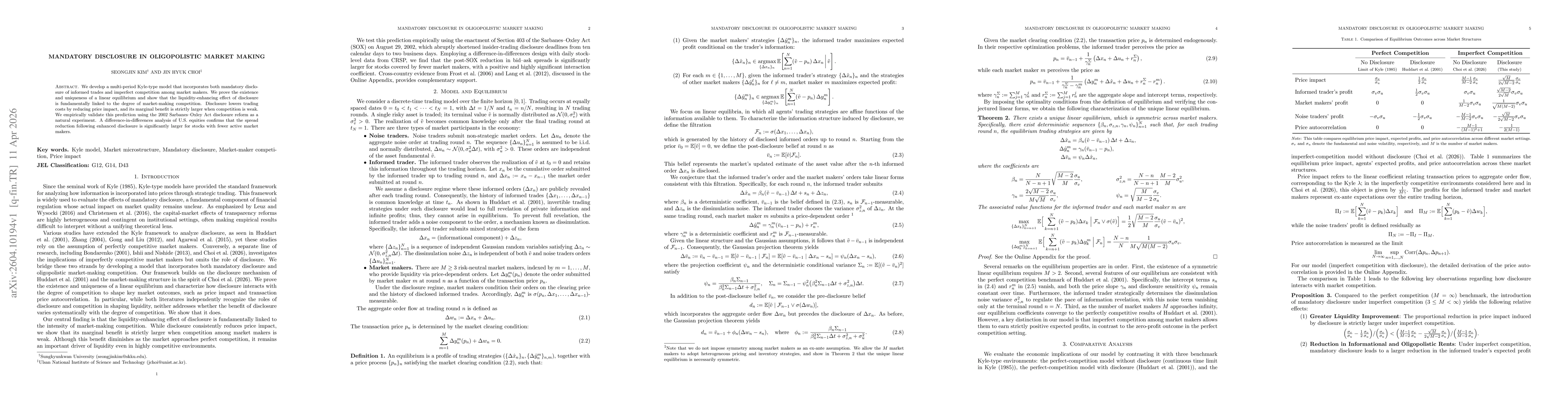

We develop a multi-period Kyle-type model that incorporates both mandatory disclosure of informed trades and imperfect competition among market makers. We prove the existence and uniqueness of a linea...