Academic Profile

Statistics

Similar Authors

Papers on arXiv

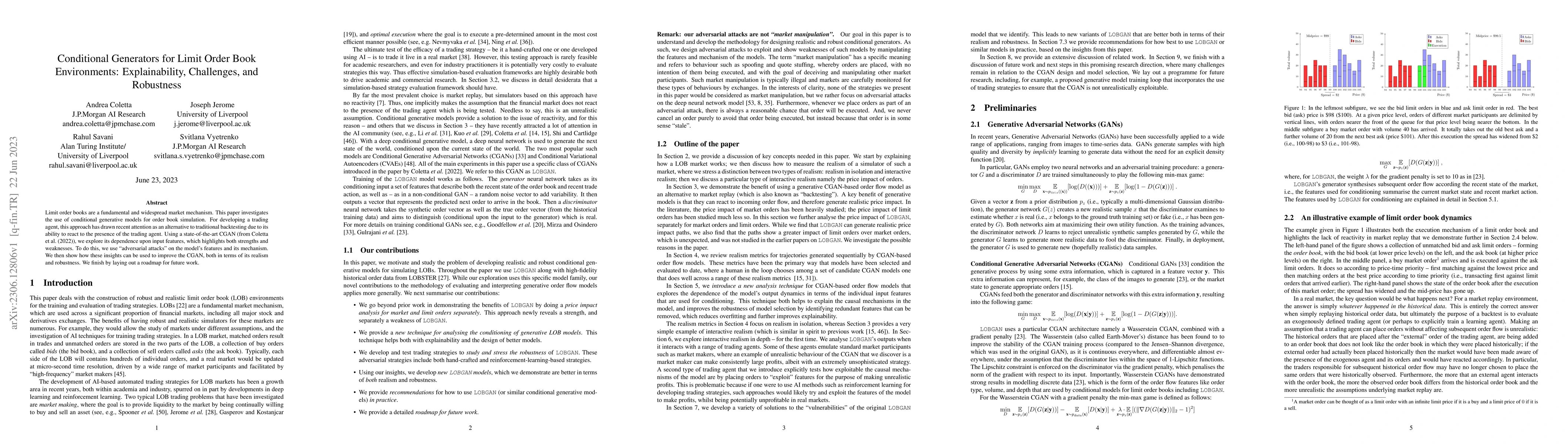

Limit order books are a fundamental and widespread market mechanism. This paper investigates the use of conditional generative models for order book simulation. For developing a trading agent, this ...

Within the mathematical finance literature there is a rich catalogue of mathematical models for studying algorithmic trading problems -- such as market-making and optimal execution -- in limit order...

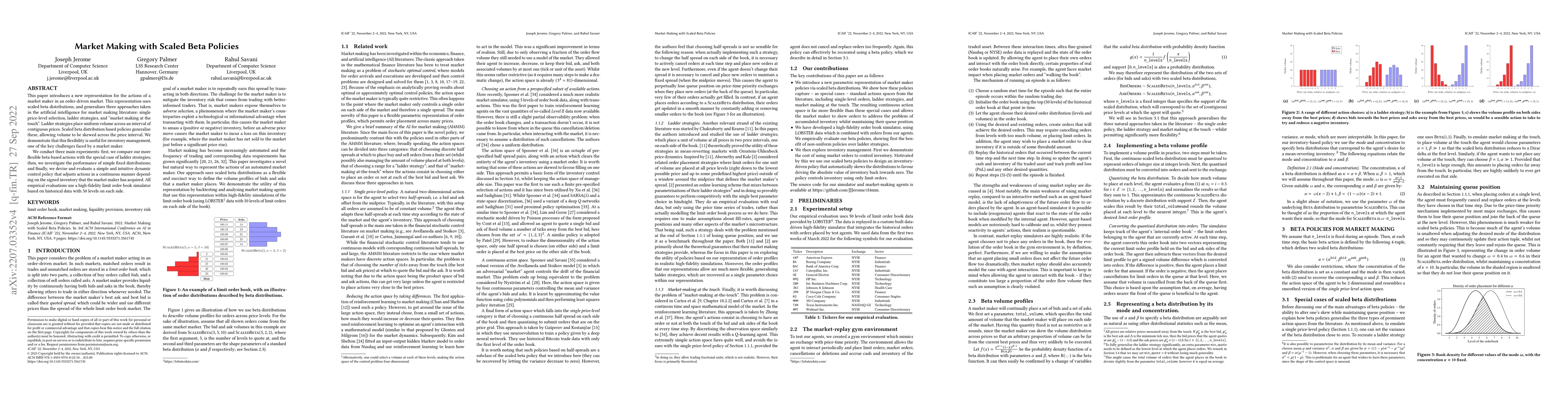

This paper introduces a new representation for the actions of a market maker in an order-driven market. This representation uses scaled beta distributions, and generalises three approaches taken in ...

In this article, we consider the optimal investment-consumption problem for an agent with preferences governed by Epstein--Zin stochastic differential utility (EZ-SDU) who invests in a constant-para...

In this article we consider the optimal investment-consumption problem for an agent with preferences governed by Epstein-Zin stochastic differential utility who invests in a constant-parameter Black...

In this article we consider the infinite-horizon Merton investment-consumption problem in a constant-parameter Black - Scholes - Merton market for an agent with constant relative risk aversion R. Th...