Academic Profile

Statistics

Similar Authors

Papers on arXiv

Large language models (LLMs) are now widely used in various fields, including finance. However, Japanese financial-specific LLMs have not been proposed yet. Hence, this study aims to construct a Jap...

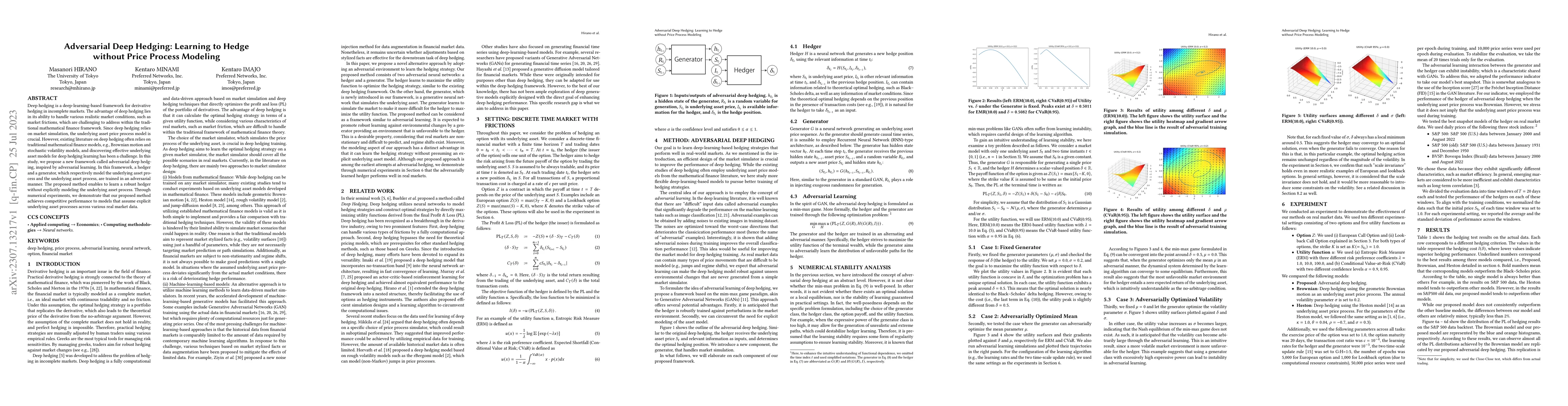

Deep hedging is a deep-learning-based framework for derivative hedging in incomplete markets. The advantage of deep hedging lies in its ability to handle various realistic market conditions, such as...

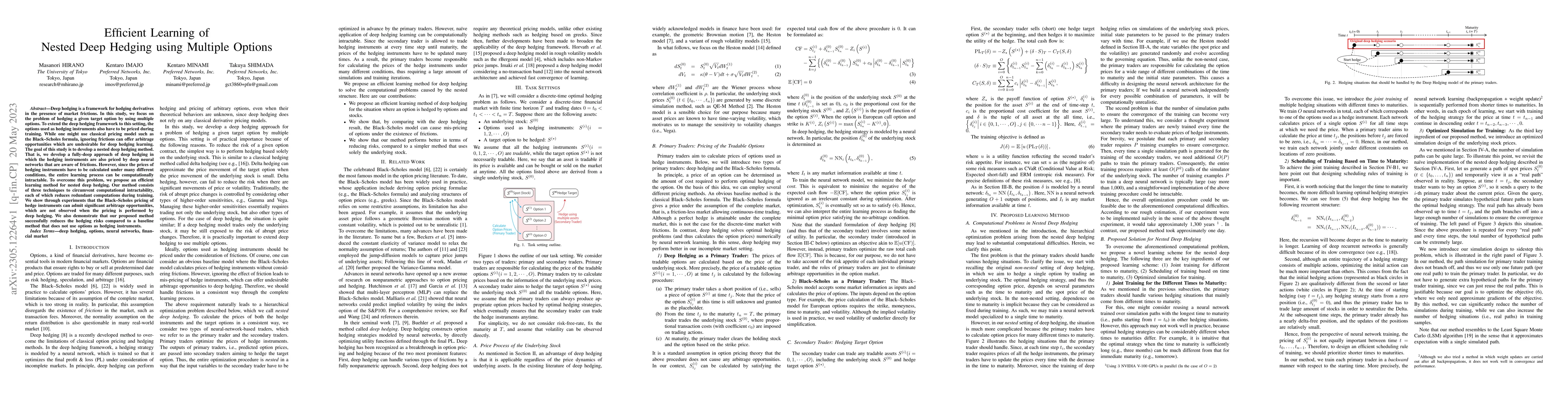

Deep hedging is a framework for hedging derivatives in the presence of market frictions. In this study, we focus on the problem of hedging a given target option by using multiple options. To extend ...

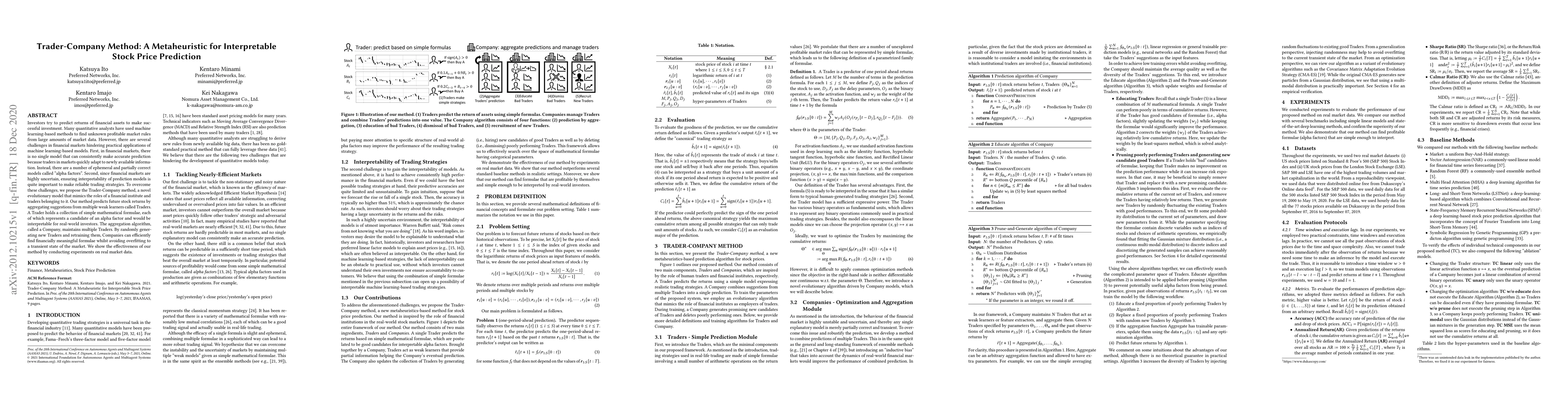

Machine learning is an increasingly popular tool with some success in predicting stock prices. One promising method is the Trader-Company~(TC) method, which takes into account the dynamism of the st...

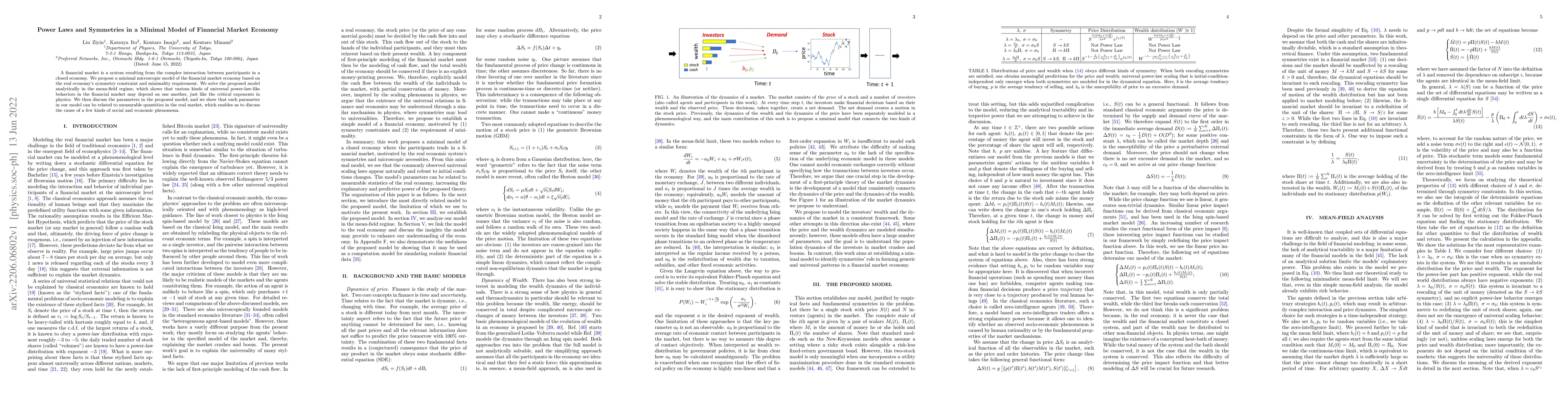

A financial market is a system resulting from the complex interaction between participants in a closed economy. We propose a minimal microscopic model of the financial market economy based on the re...

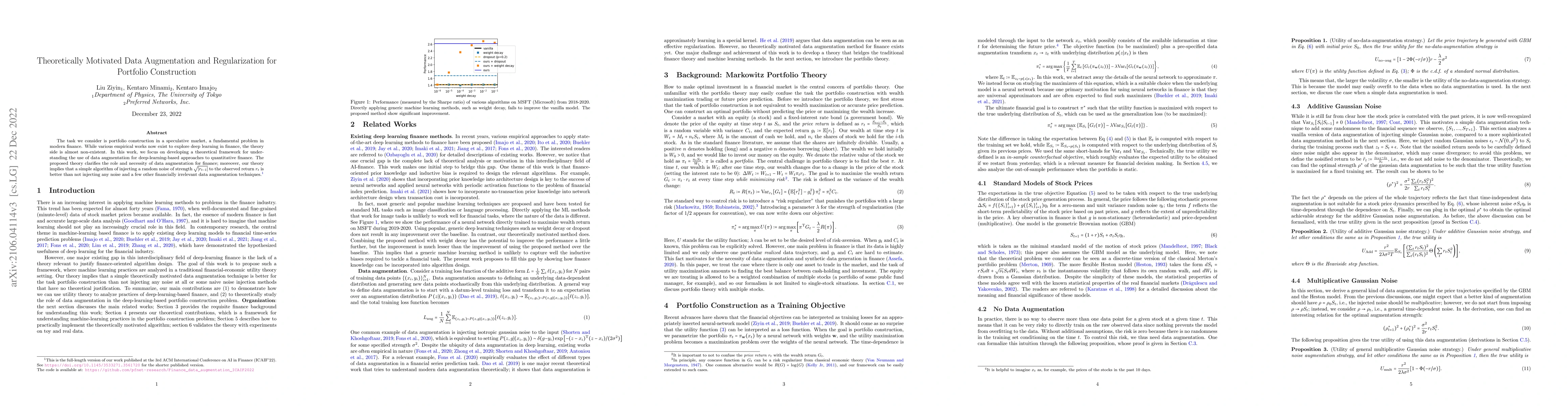

The task we consider is portfolio construction in a speculative market, a fundamental problem in modern finance. While various empirical works now exist to explore deep learning in finance, the theo...

Deep hedging (Buehler et al. 2019) is a versatile framework to compute the optimal hedging strategy of derivatives in incomplete markets. However, this optimal strategy is hard to train due to actio...

Investors try to predict returns of financial assets to make successful investment. Many quantitative analysts have used machine learning-based methods to find unknown profitable market rules from l...

Recent developments in deep learning techniques have motivated intensive research in machine learning-aided stock trading strategies. However, since the financial market has a highly non-stationary ...

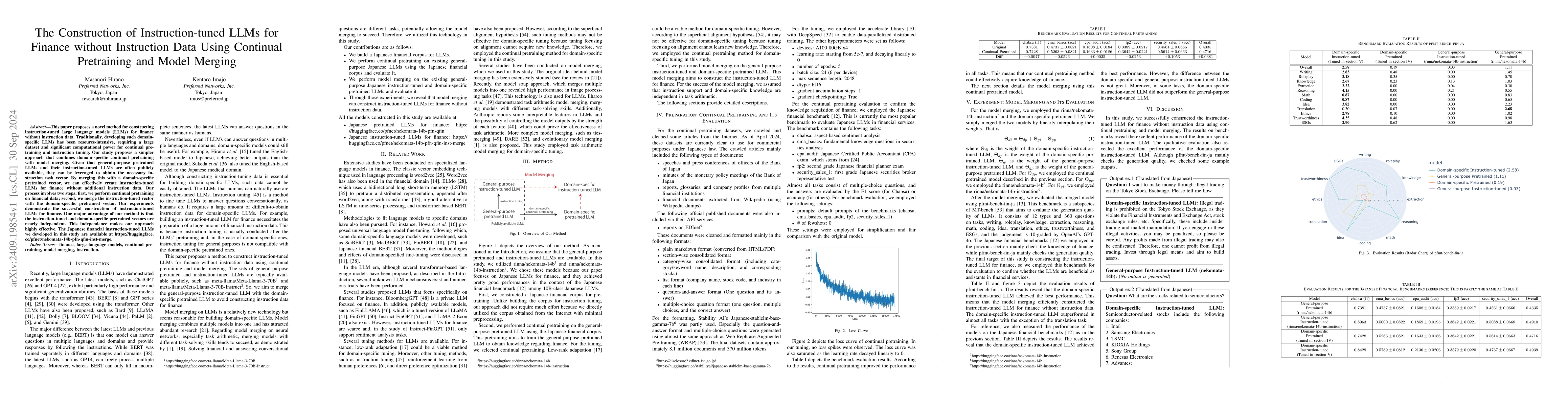

This paper proposes a novel method for constructing instruction-tuned large language models (LLMs) for finance without instruction data. Traditionally, developing such domain-specific LLMs has been re...

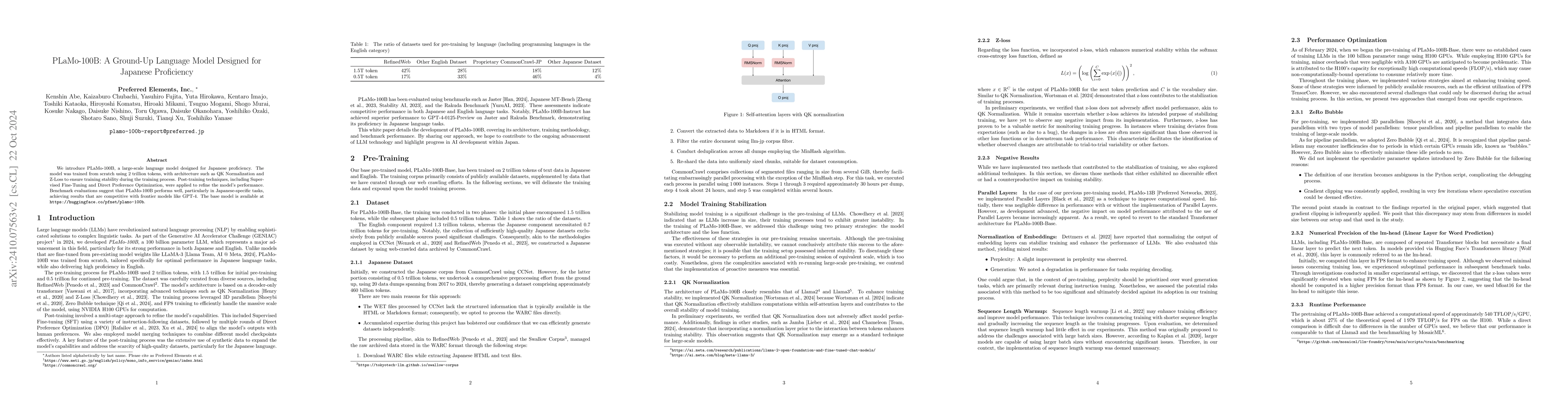

We introduce PLaMo-100B, a large-scale language model designed for Japanese proficiency. The model was trained from scratch using 2 trillion tokens, with architecture such as QK Normalization and Z-Lo...

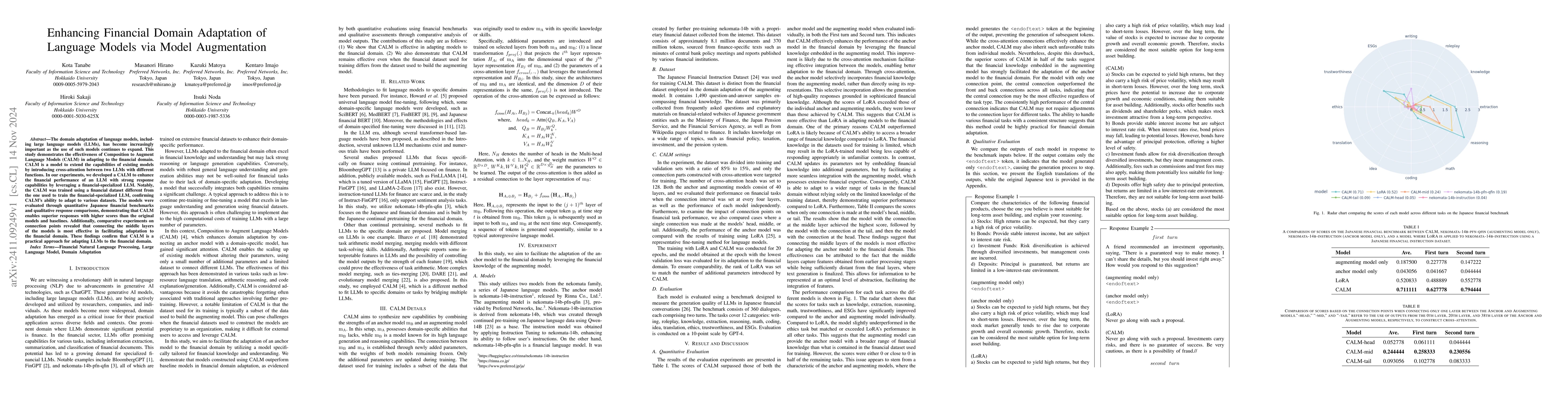

The domain adaptation of language models, including large language models (LLMs), has become increasingly important as the use of such models continues to expand. This study demonstrates the effective...

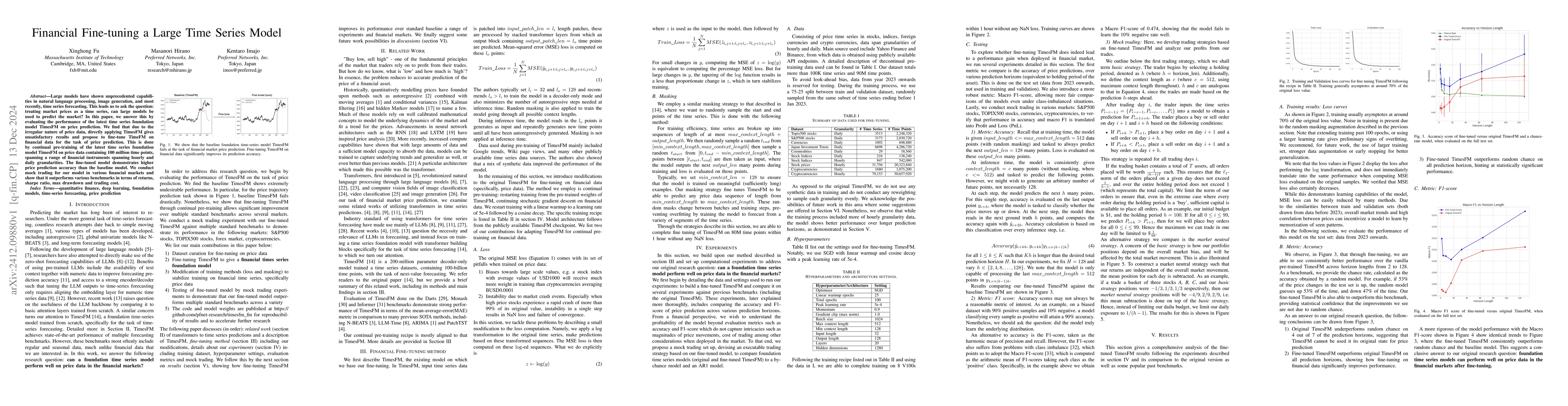

Large models have shown unprecedented capabilities in natural language processing, image generation, and most recently, time series forecasting. This leads us to ask the question: treating market pric...

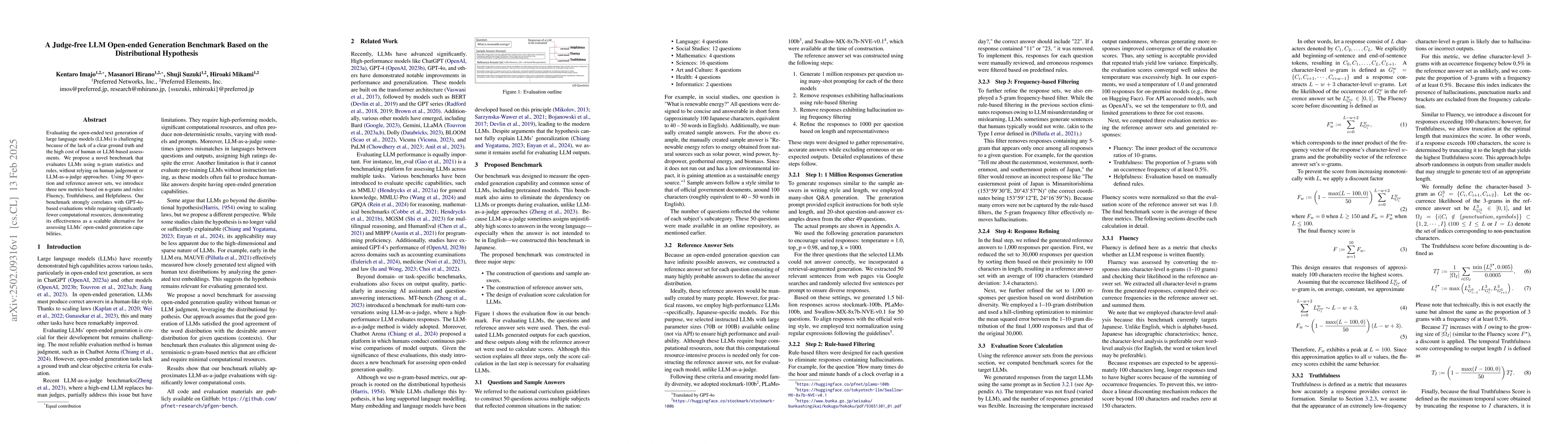

Evaluating the open-ended text generation of large language models (LLMs) is challenging because of the lack of a clear ground truth and the high cost of human or LLM-based assessments. We propose a n...

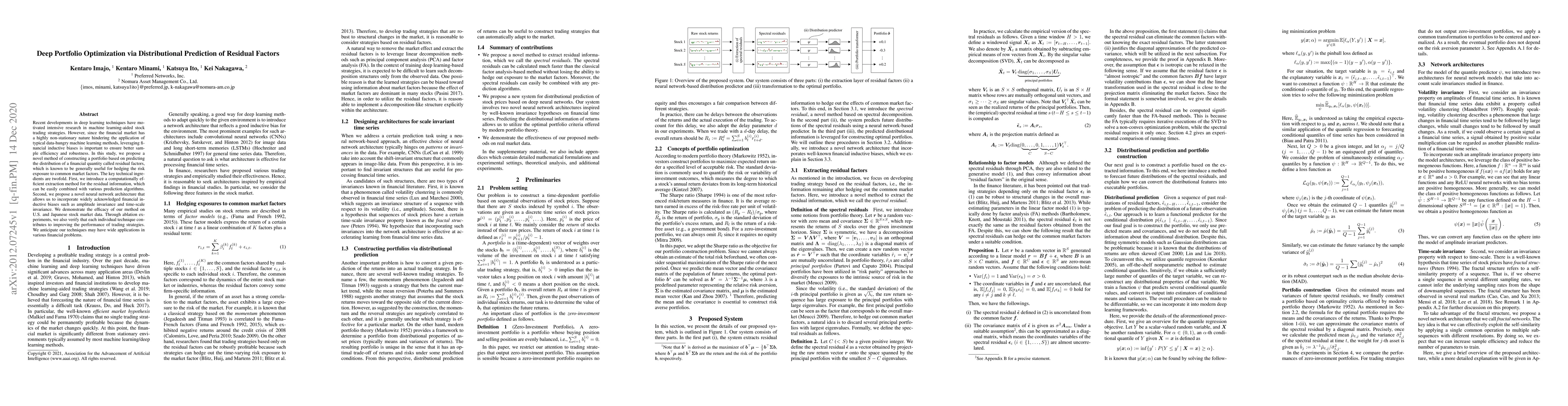

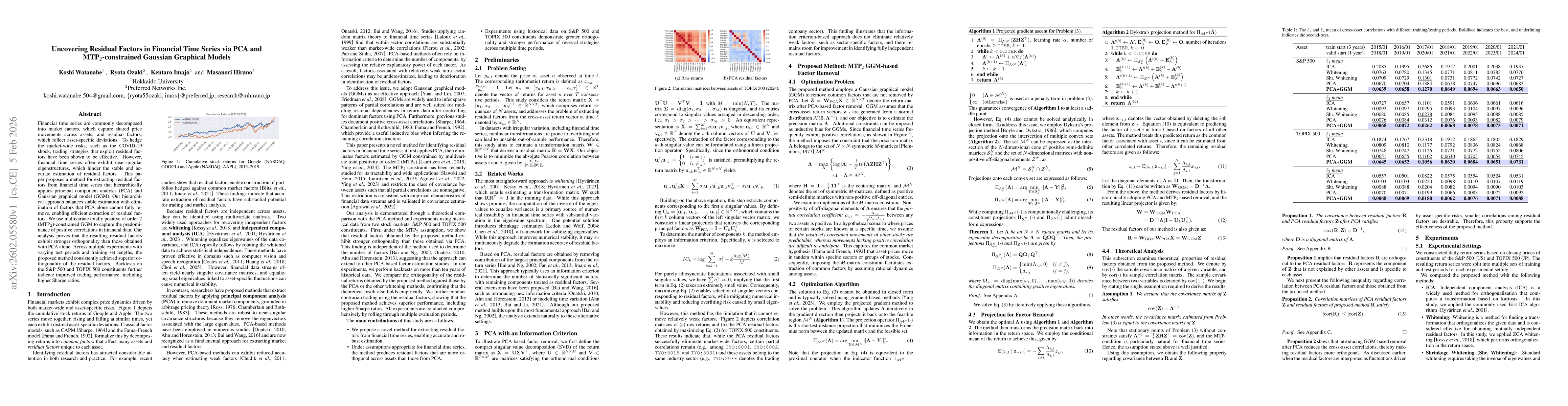

Financial time series are commonly decomposed into market factors, which capture shared price movements across assets, and residual factors, which reflect asset-specific deviations. To hedge the marke...