Academic Profile

Statistics

Similar Authors

Papers on arXiv

Option pricing, a fundamental problem in finance, often requires solving non-linear partial differential equations (PDEs). When dealing with multi-asset options, such as rainbow options, these PDEs ...

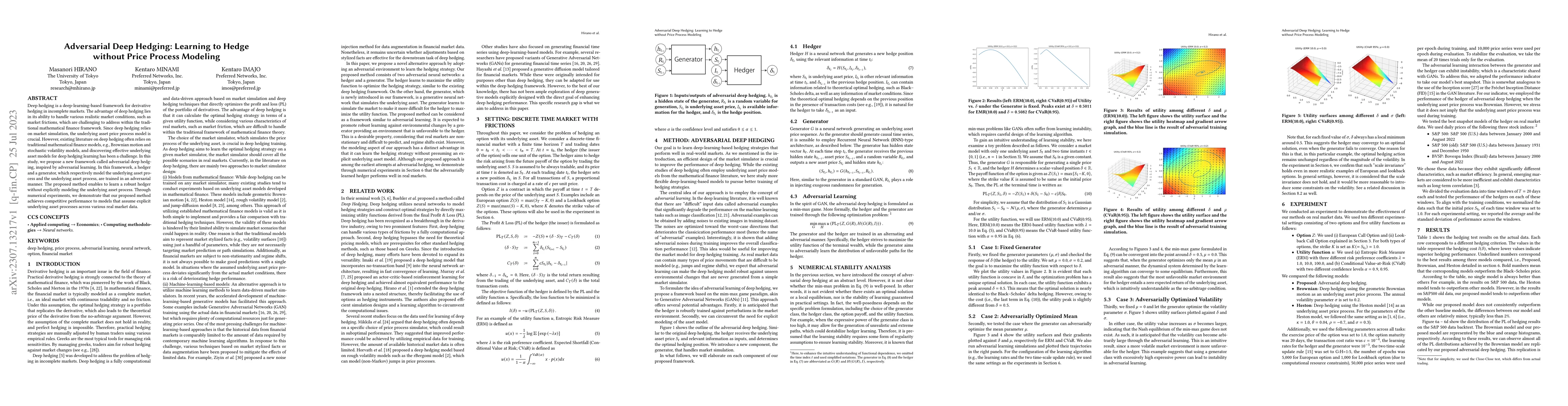

Deep hedging is a deep-learning-based framework for derivative hedging in incomplete markets. The advantage of deep hedging lies in its ability to handle various realistic market conditions, such as...

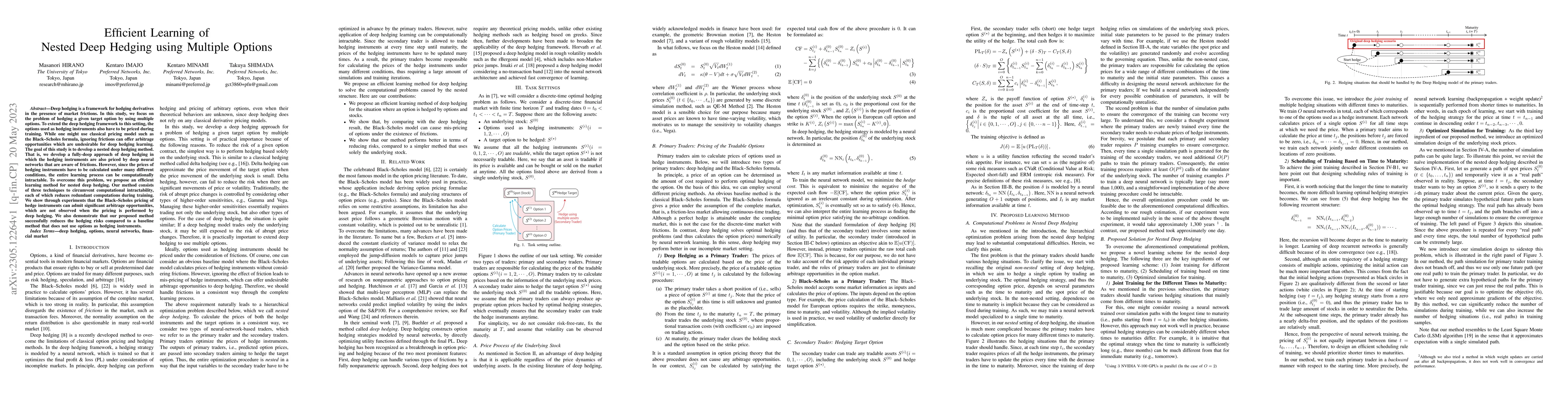

Deep hedging is a framework for hedging derivatives in the presence of market frictions. In this study, we focus on the problem of hedging a given target option by using multiple options. To extend ...

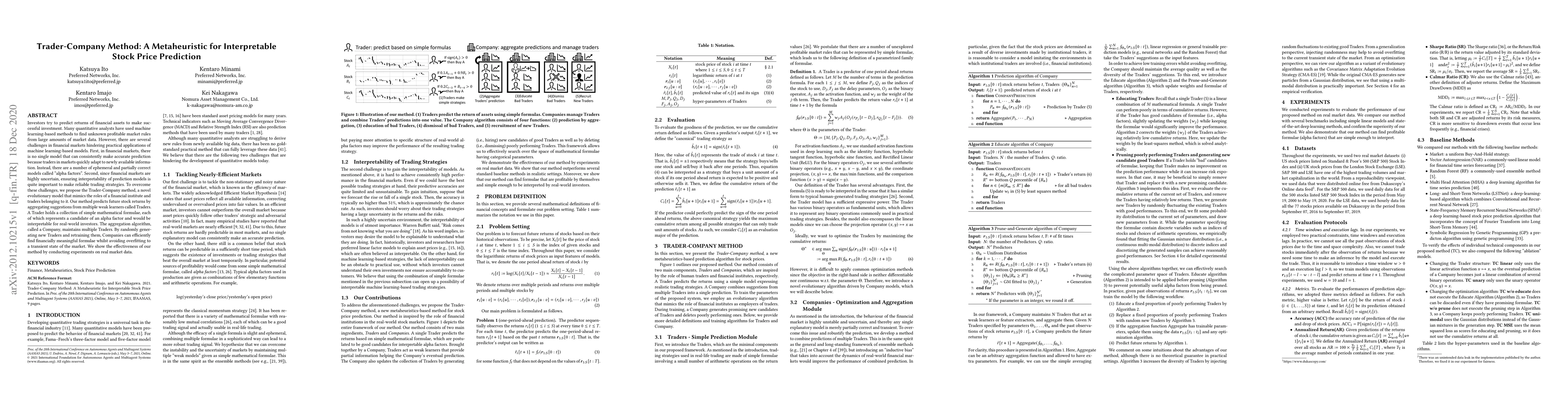

Machine learning is an increasingly popular tool with some success in predicting stock prices. One promising method is the Trader-Company~(TC) method, which takes into account the dynamism of the st...

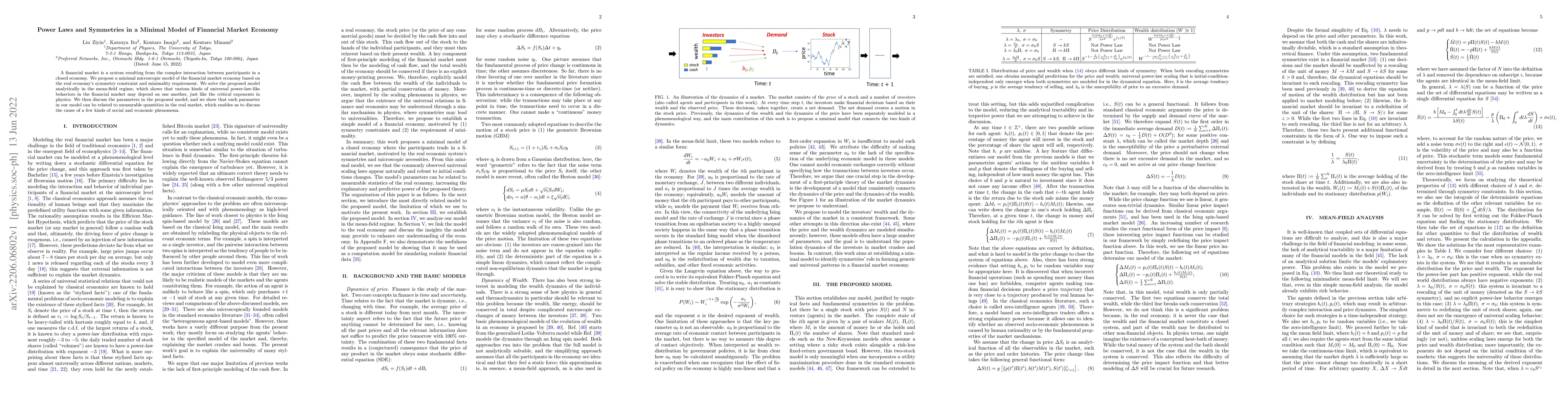

A financial market is a system resulting from the complex interaction between participants in a closed economy. We propose a minimal microscopic model of the financial market economy based on the re...

This paper provides a unified perspective for the Kullback-Leibler (KL)-divergence and the integral probability metrics (IPMs) from the perspective of maximum likelihood density-ratio estimation (DR...

In contrastive representation learning, data representation is trained so that it can classify the image instances even when the images are altered by augmentations. However, depending on the datase...

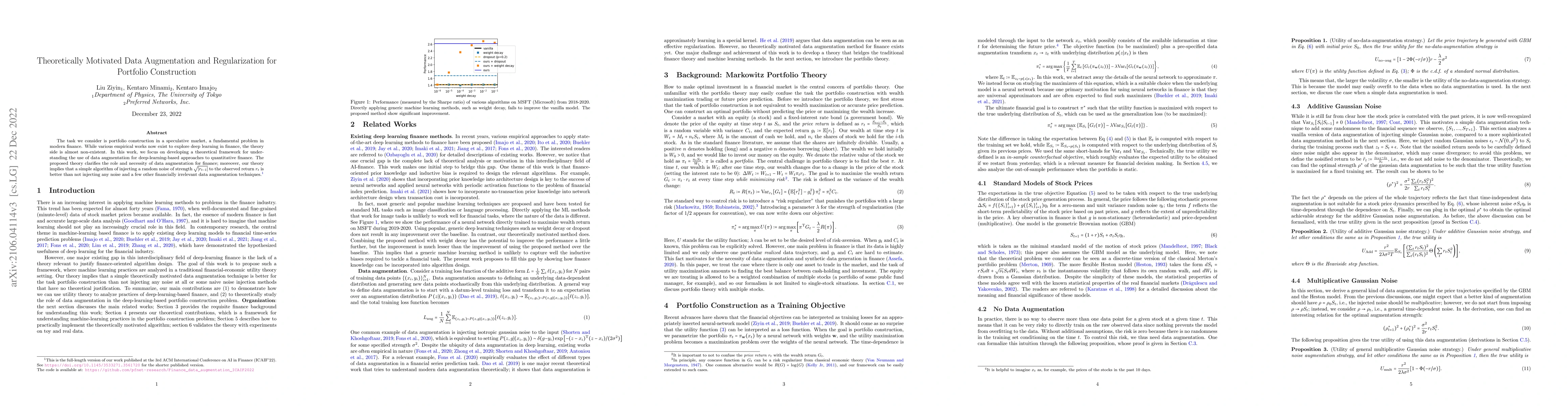

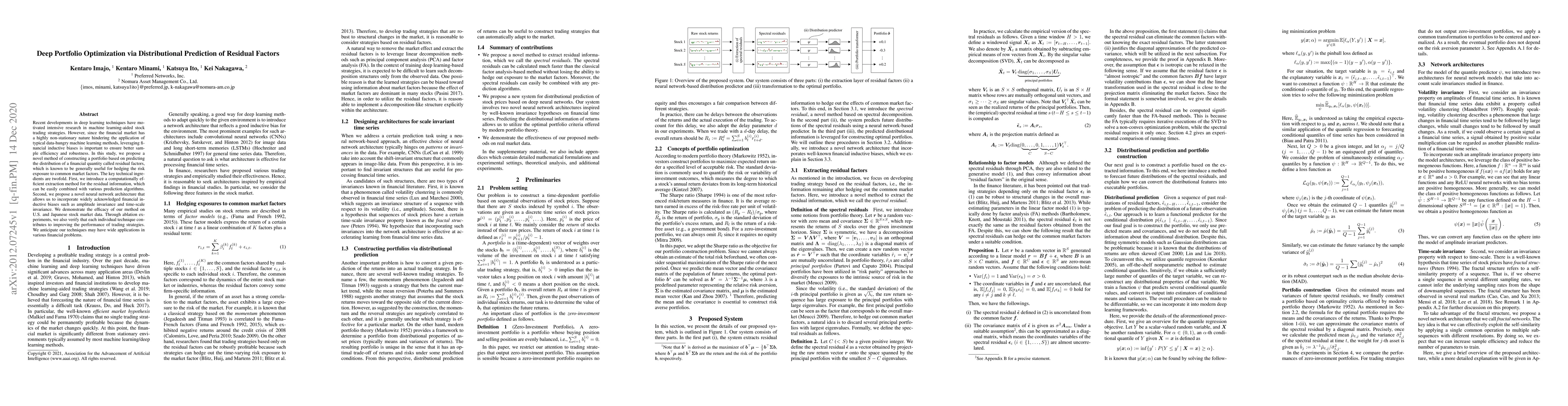

The task we consider is portfolio construction in a speculative market, a fundamental problem in modern finance. While various empirical works now exist to explore deep learning in finance, the theo...

Deep hedging (Buehler et al. 2019) is a versatile framework to compute the optimal hedging strategy of derivatives in incomplete markets. However, this optimal strategy is hard to train due to actio...

Investors try to predict returns of financial assets to make successful investment. Many quantitative analysts have used machine learning-based methods to find unknown profitable market rules from l...

Recent developments in deep learning techniques have motivated intensive research in machine learning-aided stock trading strategies. However, since the financial market has a highly non-stationary ...

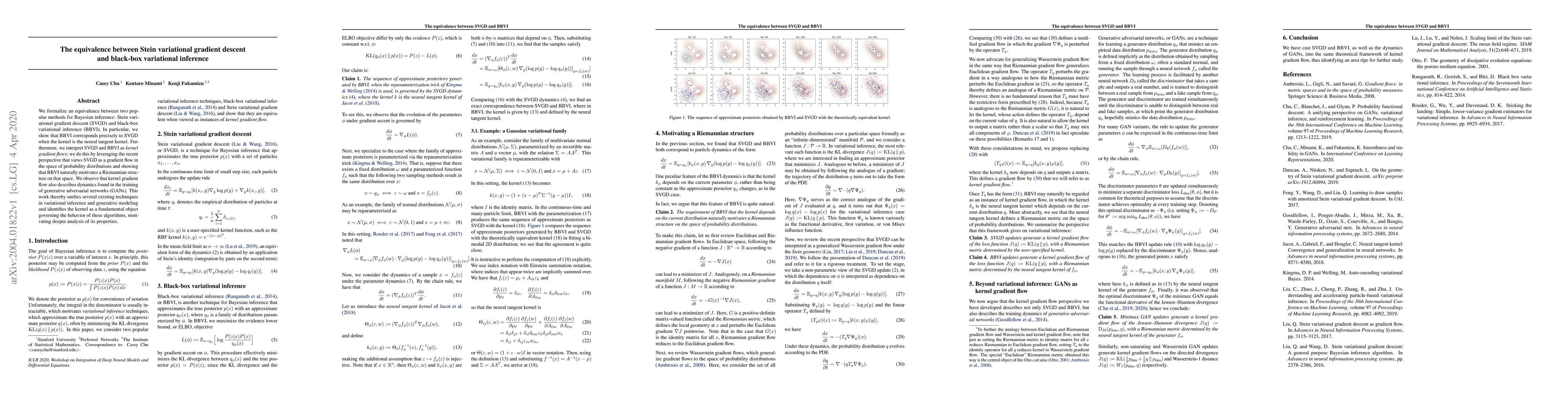

We formalize an equivalence between two popular methods for Bayesian inference: Stein variational gradient descent (SVGD) and black-box variational inference (BBVI). In particular, we show that BBVI...

Generative adversarial networks, or GANs, commonly display unstable behavior during training. In this work, we develop a principled theoretical framework for understanding the stability of various t...

We study the problem of estimating piecewise monotone vectors. This problem can be seen as a generalization of the isotonic regression that allows a small number of order-violating changepoints. We ...

The AI traders in financial markets have sparked significant interest in their effects on price formation mechanisms and market volatility, raising important questions for market stability and regulat...