Academic Profile

Statistics

Similar Authors

Papers on arXiv

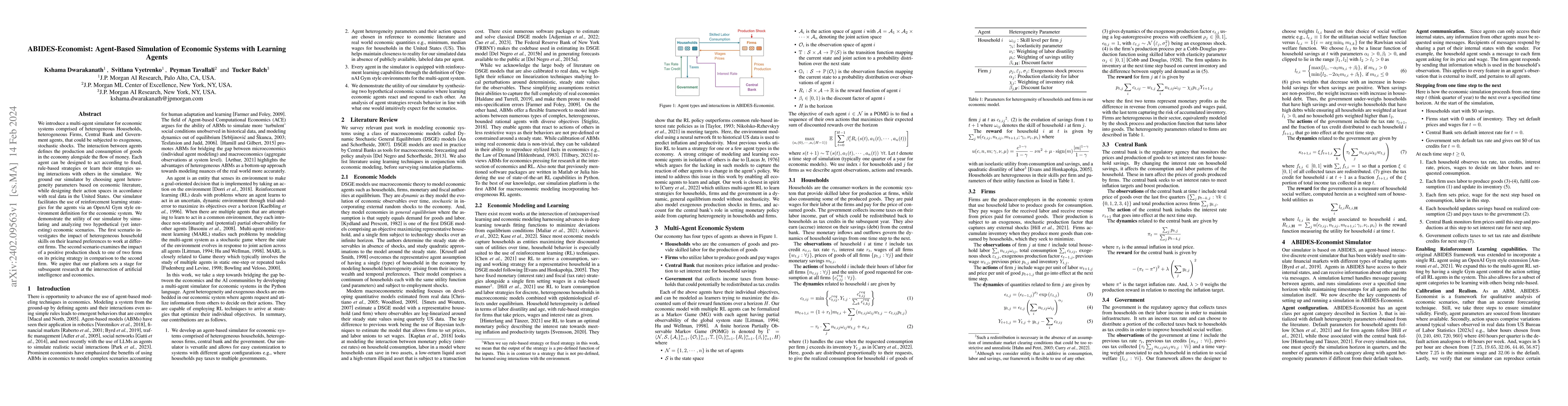

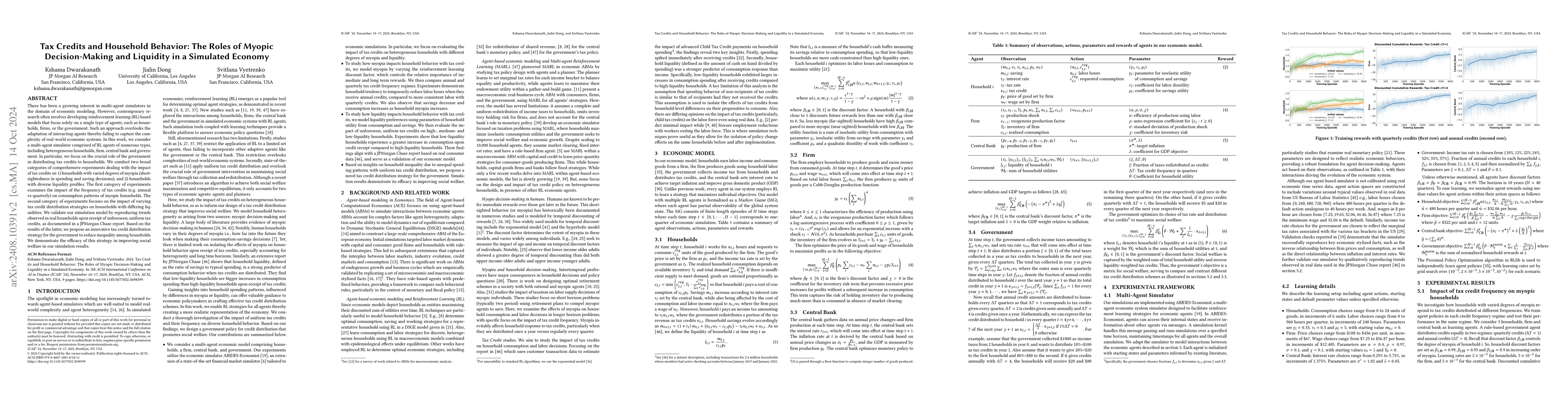

We introduce a multi-agent simulator for economic systems comprised of heterogeneous Households, heterogeneous Firms, Central Bank and Government agents, that could be subjected to exogenous, stocha...

Modeling subrational agents, such as humans or economic households, is inherently challenging due to the difficulty in calibrating reinforcement learning models or collecting data that involves huma...

Is transparency always beneficial in complex systems such as traffic networks and stock markets? How is transparency defined in multi-agent systems, and what is its optimal degree at which social we...

We study how experience with asset price bubbles changes the trading strategies of reinforcement learning (RL) traders and ask whether the change in trading strategies helps to prevent future bubble...

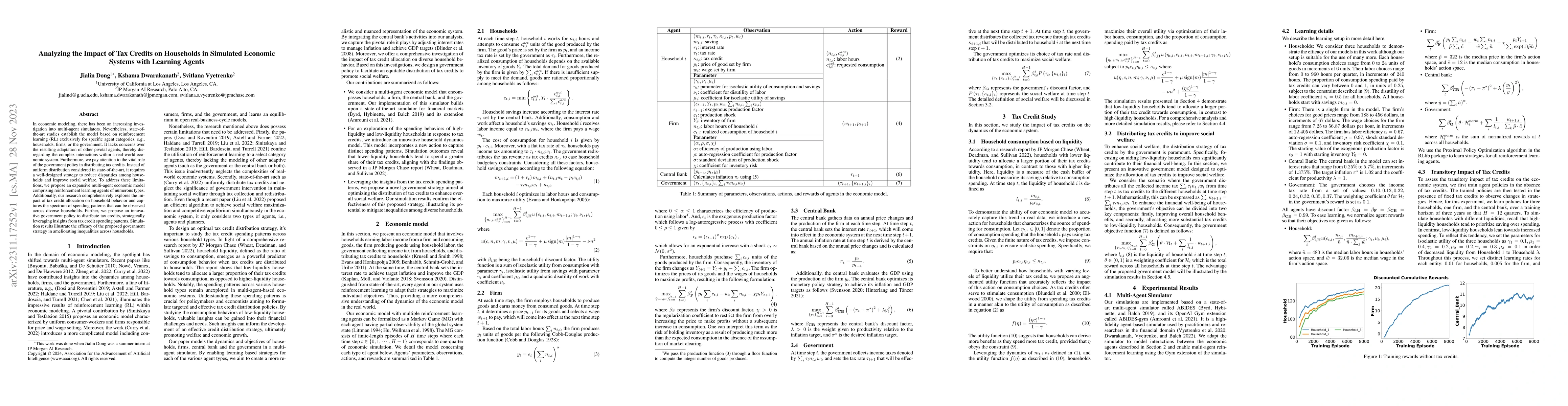

In economic modeling, there has been an increasing investigation into multi-agent simulators. Nevertheless, state-of-the-art studies establish the model based on reinforcement learning (RL) exclusiv...

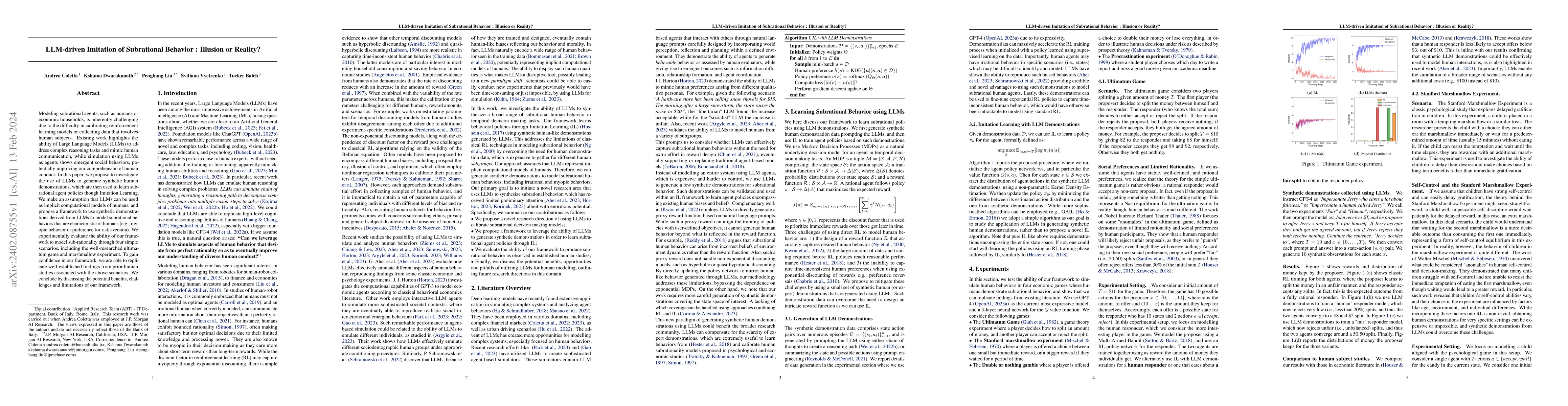

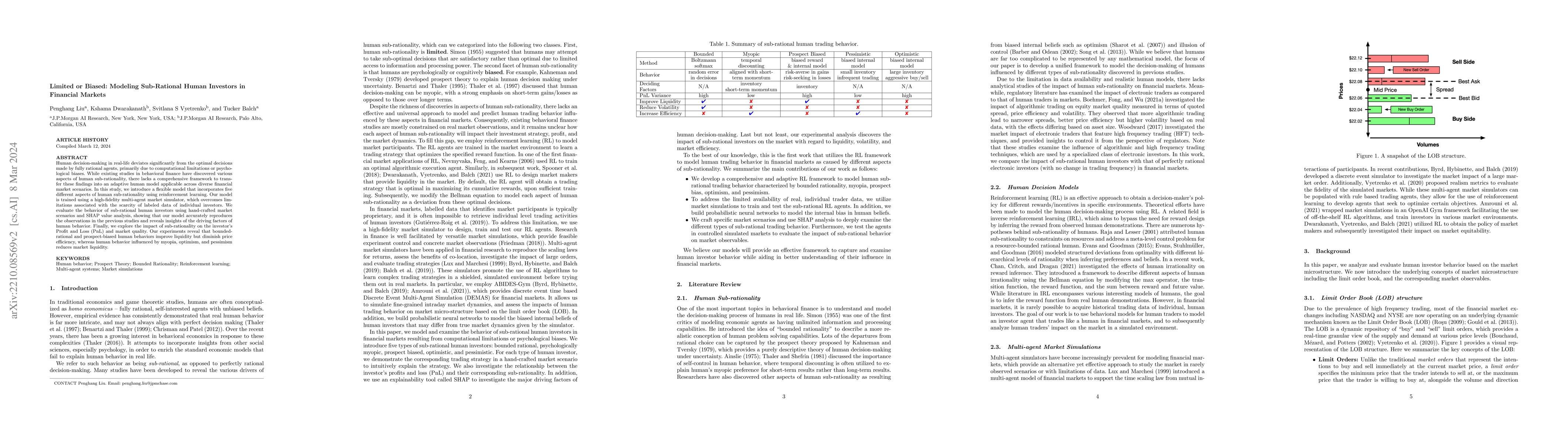

Human decision-making in real-life deviates significantly from the optimal decisions made by fully rational agents, primarily due to computational limitations or psychological biases. While existing...

We consider a trading marketplace that is populated by traders with diverse trading strategies and objectives. The marketplace allows the suppliers to list their goods and facilitates matching betwe...

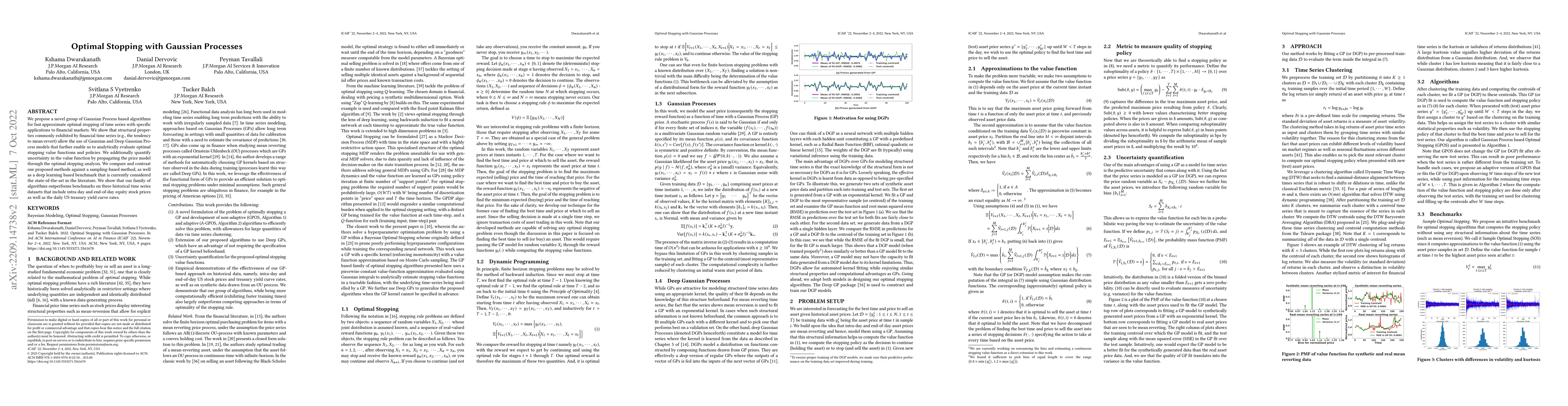

We propose a novel group of Gaussian Process based algorithms for fast approximate optimal stopping of time series with specific applications to financial markets. We show that structural properties...

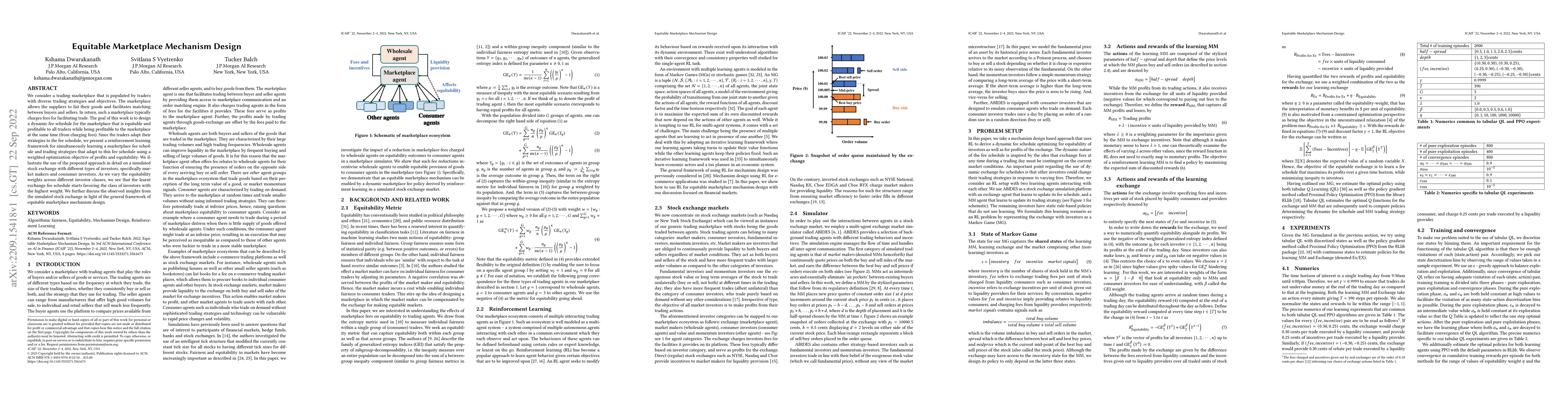

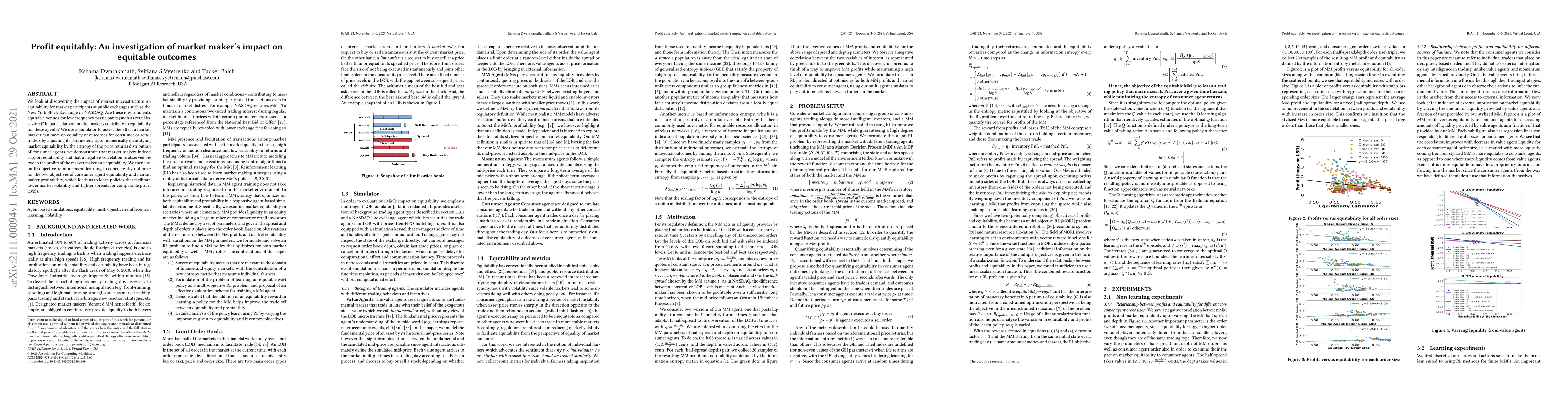

We look at discovering the impact of market microstructure on equitability for market participants at public exchanges such as the New York Stock Exchange or NASDAQ. Are these environments equitable...

There has been a growing interest in multi-agent simulators in the domain of economic modeling. However, contemporary research often involves developing reinforcement learning (RL) based models that f...

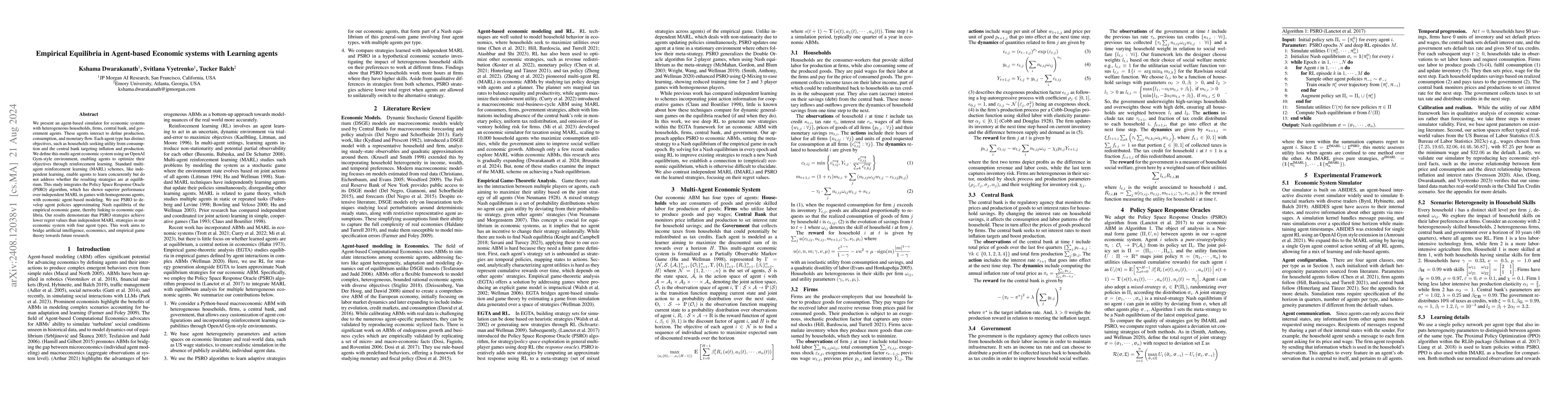

We present an agent-based simulator for economic systems with heterogeneous households, firms, central bank, and government agents. These agents interact to define production, consumption, and monetar...