Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper studies an infinite horizon optimal tracking portfolio problem using capital injection in incomplete market models. We consider the benchmark process modelled by a geometric Brownian moti...

We study a De Finetti's optimal dividend and capital injection problem under a Markov additive model. The surplus process before dividend and capital injection is assumed to follow a spectrally posi...

This paper studies the existence and uniqueness of a classical solution to a type of Robin boundary problems on the nonnegative orthant. We propose a new decomposition-homogenization method for the ...

This paper studies a Merton's optimal portfolio and consumption problem in an extended formulation incorporating the tracking of a benchmark process described by a geometric Brownian motion. We cons...

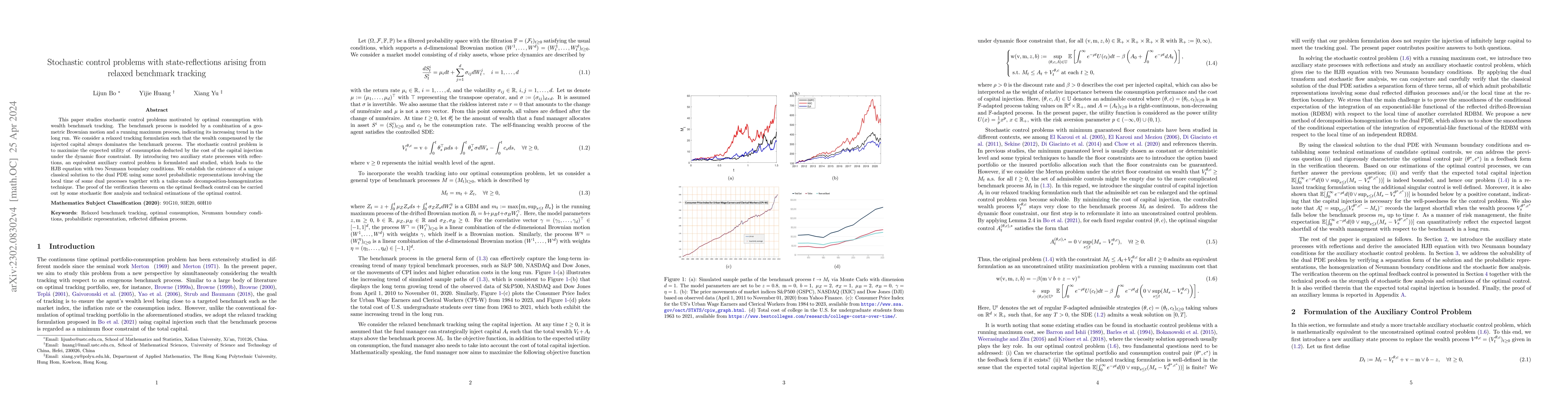

This paper studies stochastic control problems motivated by optimal consumption with wealth benchmark tracking. The benchmark process is modeled by a combination of a geometric Brownian motion and a...

In this paper we consider the De Finetti's optimal dividend and capital injection problem under a Markov additive model. We assume that the surplus process before dividends and capital injections fo...

This paper studies the equilibrium consumption under external habit formation in a large population of agents. We first formulate problems under two types of conventional habit formation preferences...

We study the forward investment performance process (FIPP) in an incomplete semimartingale market model with closed and convex portfolio constraints, when the investor's risk preferences are of the ...

This paper studies the n-player game and the mean field game under the CRRA relative performance on terminal wealth, in which the interaction occurs by peer competition. In the model with n agents, ...

This paper studies a systemic risk control problem by the central bank, which dynamically plans monetary supply to stabilize the interbank system with borrowing and lending activities. Facing both h...

This paper studies the finite horizon portfolio management by optimally tracking a ratcheting capital benchmark process. It is assumed that the fund manager can dynamically inject capital into the p...

This paper introduces a general class of Replicator-Mutator equations on a multi-dimensional fitness space. We establish a novel probabilistic representation of weak solutions of the equation by usi...

We study a class of sampled stochastic optimization problems, where the underlying state process has diffusive dynamics of the mean-field type. We establish the existence of optimal relaxed controls...

This paper studies continuous-time reinforcement learning for controlled jump-diffusion models by featuring the q-function (the continuous-time counterpart of Q-function) and the q-learning algorithms...

This paper studies an optimal consumption problem with both relaxed benchmark tracking and consumption drawdown constraint, leading to a stochastic control problem with dynamic state-control constrain...

This paper studies the extended mean field control problems under general dynamic expectation constraints and/or dynamic pathwise state-control and law constraints. We aim to pioneer the establishment...

This paper studies the extended mean-field control problems with state-control joint law dependence and Poissonian common noise. We develop the stochastic maximum principle (SMP) and establish the con...

We study the mean field game problem for a nervous system consisting of a large number of neurons with mean-field interaction. In this system, each neuron can modulate its spiking activity by controll...

This paper studies some mean-field control (MFC) problems with singular control under general dynamic state-control-law constraints. We first propose a customized relaxed control formulation to cope w...

This paper studies mean field game (MFG) of controls by featuring the joint distribution of the state and the control with the reflected state process along an exogenous stochastic reflection boundary...

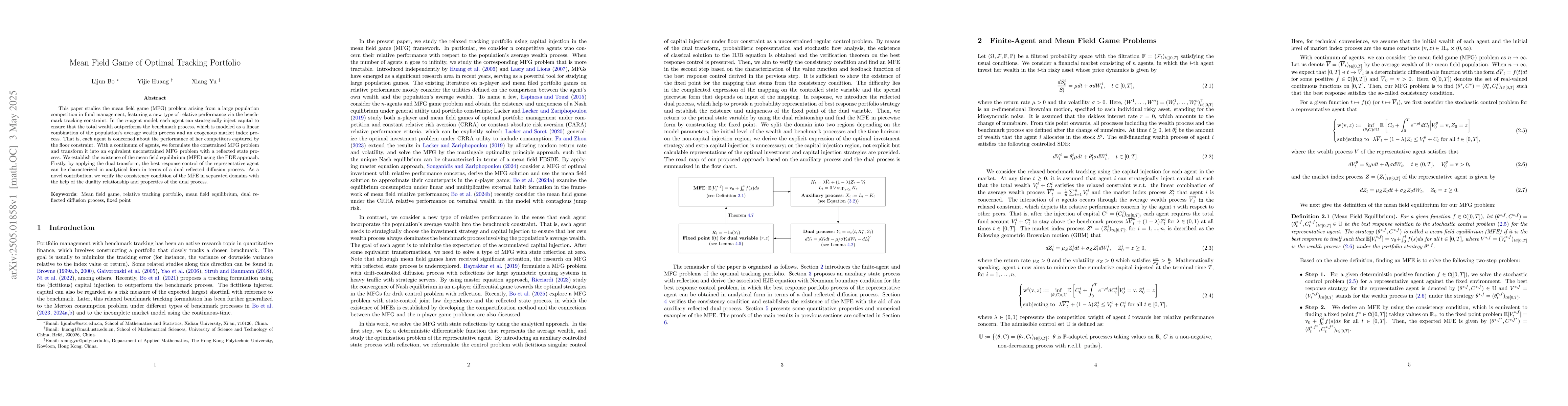

This paper studies the mean field game (MFG) problem arising from a large population competition in fund management, featuring a new type of relative performance via the benchmark tracking constraint....

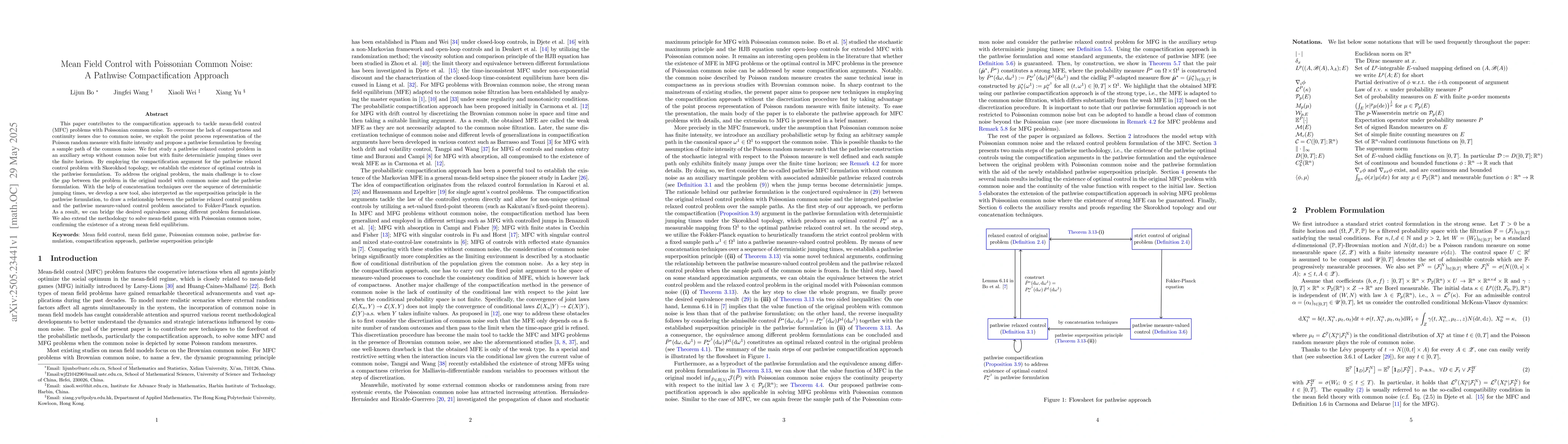

This paper contributes to the compactification approach to tackle mean-field control (MFC) problems with Poissonian common noise. To overcome the lack of compactness and continuity issues due to commo...

We investigate the optimal charging strategy for large-scale electric vehicles in smart grids using a finite-horizon framework within a mean field game approach. By proving the existence and uniquenes...

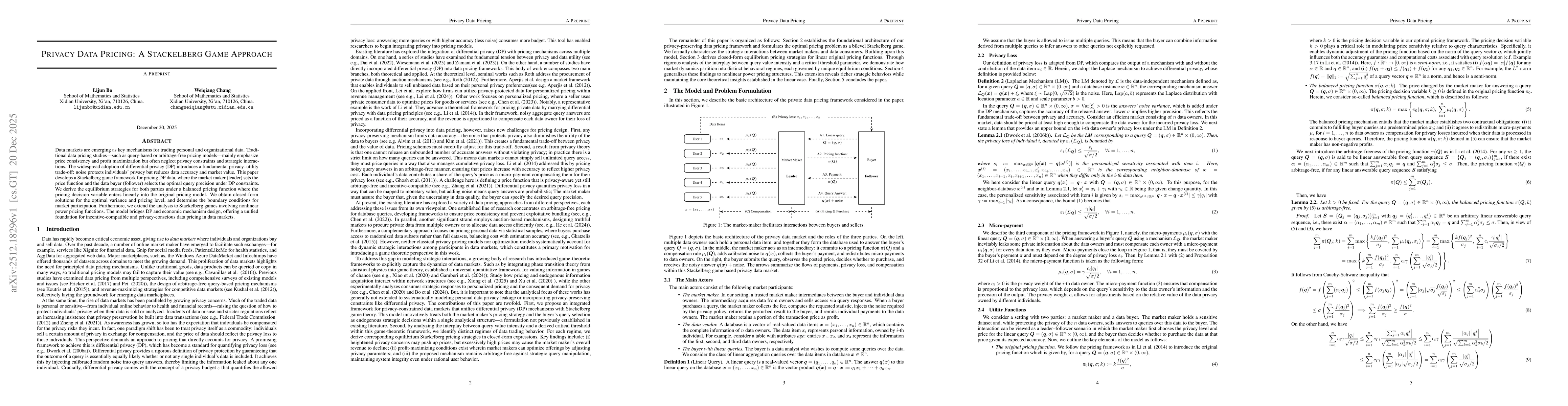

Data markets are emerging as key mechanisms for trading personal and organizational data. Traditional data pricing studies -- such as query-based or arbitrage-free pricing models -- mainly emphasize p...

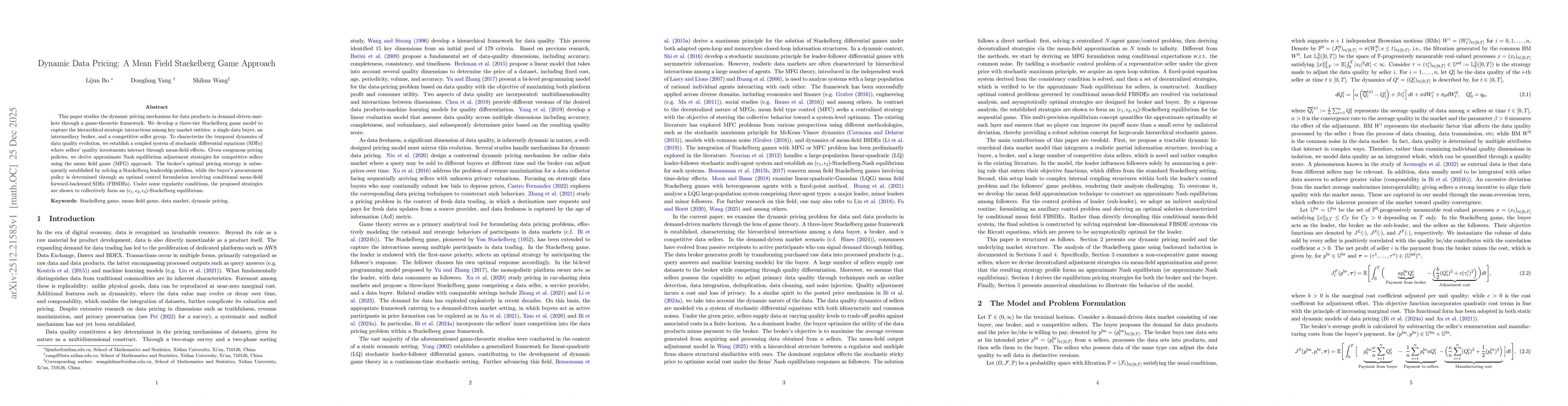

This paper studies the dynamic pricing mechanism for data products in demand-driven markets through a game-theoretic framework. We develop a three-tier Stackelberg game model to capture the hierarchic...

This paper studies the optimal portfolio, consumption, and endogenous early retirement problem within a benchmark tracking framework by incorporating a new relative performance evaluation. In this fra...