Academic Profile

Statistics

Similar Authors

Papers on arXiv

American and Bermudan-type financial instruments are often priced with specific Monte Carlo techniques whose efficiency critically depends on the effective dimensionality of the problem and the avai...

We investigate portfolio optimization in financial markets from a trading and risk management perspective. We term this task Risk-Aware Trading Portfolio Optimization (RATPO), formulate the correspond...

An important step in the Financial Benchmarks Reform was taken on 13th September 2018, when the ECB Working Group on Euro Risk-Free Rates recommended the Euro Short-Term Rate ESTR as the new benchmark...

Global sensitivity analysis is employed to evaluate the effective dimension reduction achieved through Chebyshev interpolation and the conditional pathwise method for Greek estimation of discretely mo...

The SABR model is a cornerstone of interest rate volatility modeling, but its practical application relies heavily on the analytical approximation by Hagan et al., whose accuracy deteriorates for high...

Risk allocation, the decomposition of a portfolio-wide risk measure into component contributions, is a fundamental problem in financial risk management due to the non-additive nature of risk measures,...

Quasi Monte Carlo (QMC) and Global Sensitivity Analysis (GSA) techniques are applied for pricing and hedging representative financial instruments of increasing complexity. We compare standard Monte Ca...

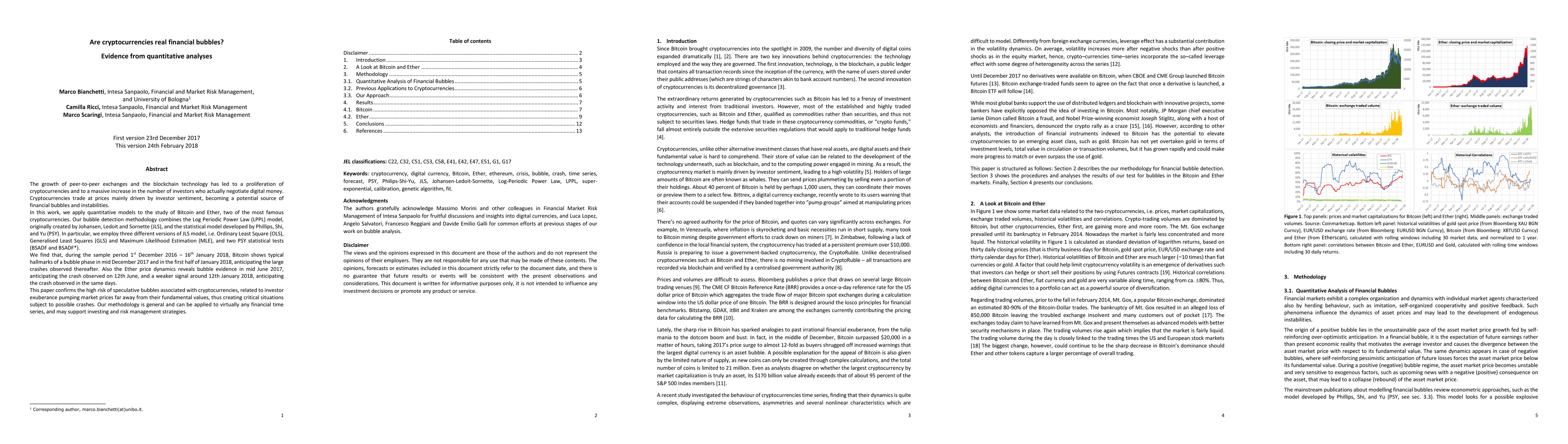

The growth of peer-to-peer exchanges and the blockchain technology has led to a proliferation of cryptocurrencies and to a massive increase in the number of investors who actually negotiate digital mo...