Academic Profile

Statistics

Similar Authors

Papers on arXiv

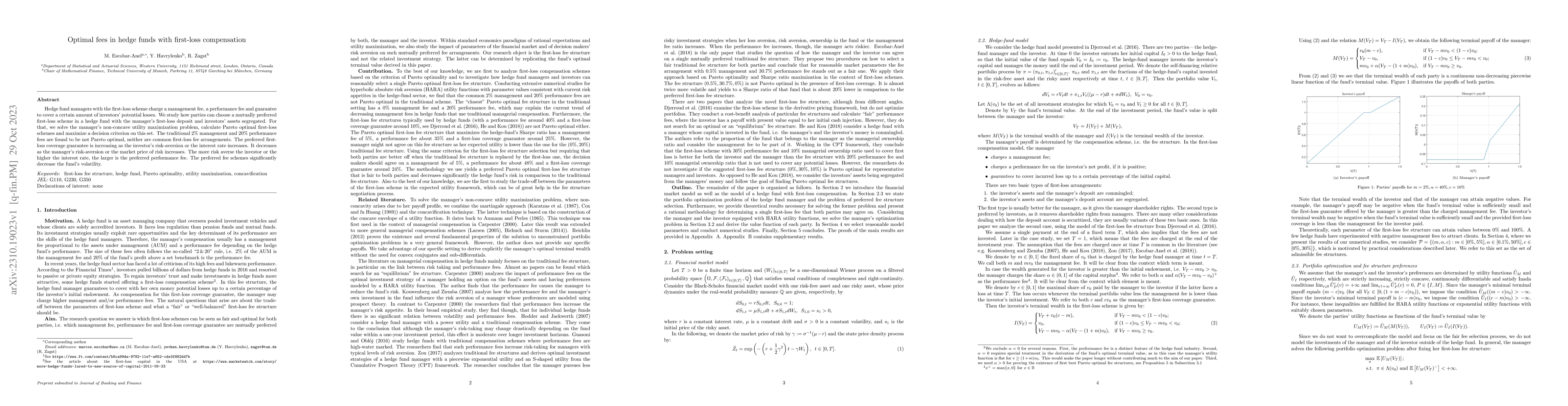

Hedge fund managers with the first-loss scheme charge a management fee, a performance fee and guarantee to cover a certain amount of investors' potential losses. We study how parties can choose a mu...

This paper proposes an expected multivariate utility analysis for ESG investors in which green stocks, brown stocks, and a market index are modeled in a one-factor, CAPM-type structure. This setting...

We consider a portfolio optimisation problem for a utility-maximising investor who faces convex constraints on his portfolio allocation in Heston's stochastic volatility model. We apply the duality ...

We study the expected utility portfolio optimization problem in an incomplete financial market where the risky asset dynamics depend on stochastic factors and the portfolio allocation is constrained...

We solve an expected utility-maximization problem with a Value-at-risk constraint on the terminal portfolio value in an incomplete financial market due to stochastic volatility. To derive the optima...

This paper investigates the optimal choices of financial derivatives to complete a financial market in the framework of stochastic volatility (SV) models. We introduce an efficient and accurate simu...

This paper challenges the use of stocks in portfolio construction, instead we demonstrate that Asian derivatives, straddles, or baskets could be more convenient substitutes. Our results are obtained...

We analyze the potential of reinsurance for reversing the current trend of decreasing capital guarantees in life insurance products. Providing an insurer with an opportunity to shift part of the fin...

This paper develops the first closed-form optimal portfolio allocation formula for a spot asset whose variance follows a GARCH(1,1) process. We consider an investor with constant relative risk avers...