Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we propose a novel conceptual framework to detect outliers using optimal transport with a concave cost function. Conventional outlier detection approaches typically use a two-stage proc...

This paper develops a novel method to estimate a latent factor model for a large target panel with missing observations by optimally using the information from auxiliary panel data sets. We refer to...

We consider the well-studied problem of predicting the time-varying covariance matrix of a vector of financial returns. Popular methods range from simple predictors like rolling window or exponentia...

This paper proposes a novel testing procedure for selecting a sparse set of covariates that explains a large dimensional panel. Our selection method provides correct false detection control while ha...

Missing time-series data is a prevalent problem in many prescriptive analytics models in operations management, healthcare and finance. Imputation methods for time-series data are usually applied to...

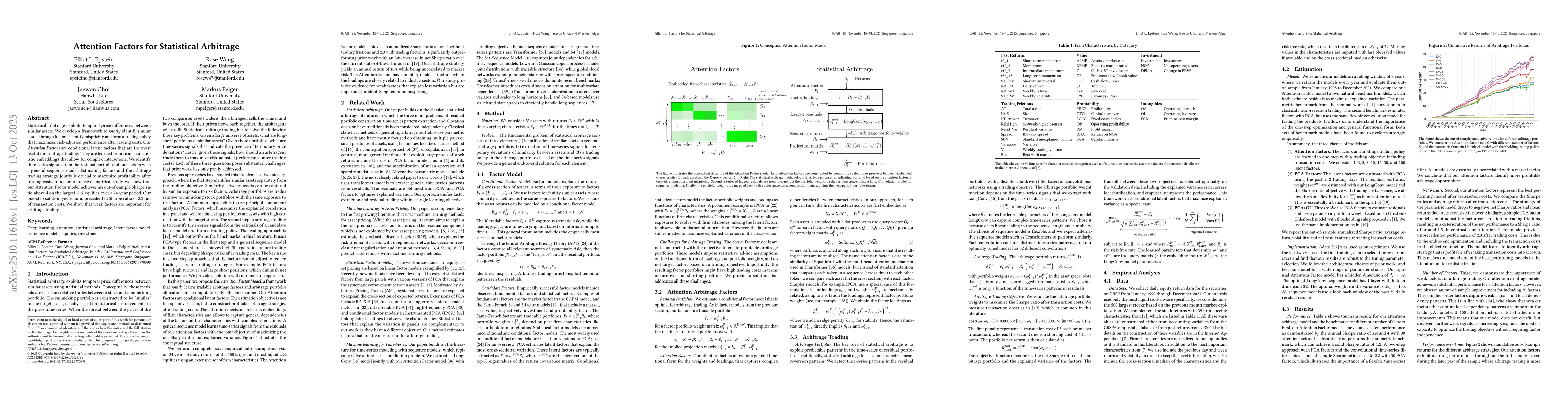

Statistical arbitrage exploits temporal price differences between similar assets. We develop a unifying conceptual framework for statistical arbitrage and a novel data driven solution. First, we con...

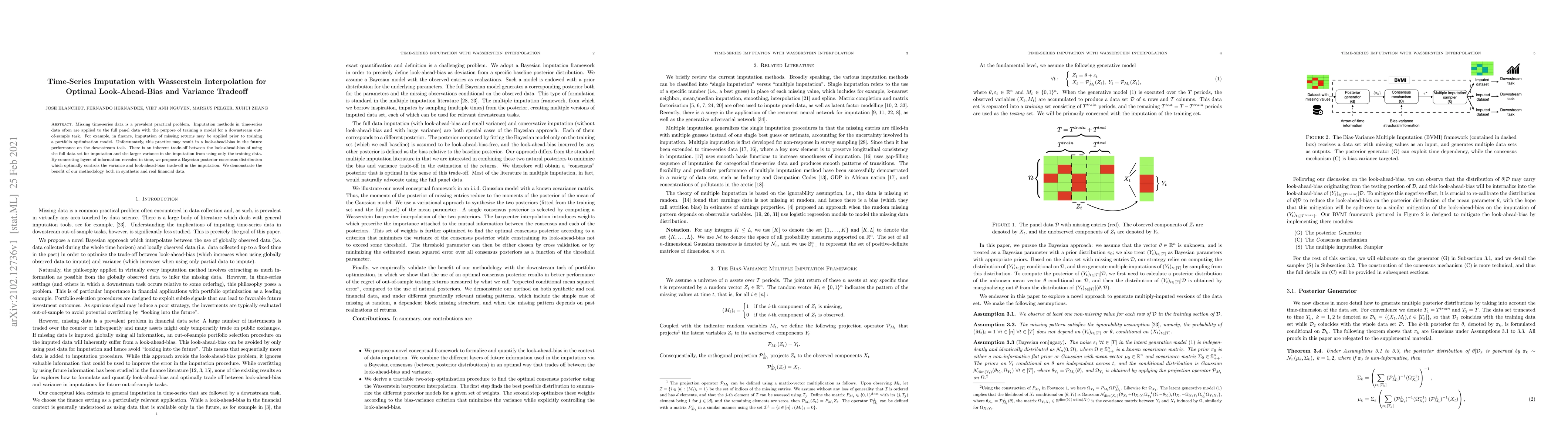

Missing time-series data is a prevalent practical problem. Imputation methods in time-series data often are applied to the full panel data with the purpose of training a model for a downstream out-o...

This paper develops the inferential theory for latent factor models estimated from large dimensional panel data with missing observations. We propose an easy-to-use all-purpose estimator for a laten...

We use deep neural networks to estimate an asset pricing model for individual stock returns that takes advantage of the vast amount of conditioning information, while keeping a fully flexible form a...

We propose novel methods for change-point testing for nonparametric estimators of expected shortfall and related risk measures in weakly dependent time series. We can detect general multiple structu...

This paper develops an inferential theory for state-varying factor models of large dimensions. Unlike constant factor models, loadings are general functions of some recurrent state process. We devel...

This paper proposes sparse and easy-to-interpret proximate factors to approximate statistical latent factors. Latent factors in a large-dimensional factor model can be estimated by principal compone...

We introduce and study the notion of sure profit via flash strategy, consisting of a high-frequency limit of buy-and-hold trading strategies. In a fully general setting, without imposing any semimar...

Statistical arbitrage exploits temporal price differences between similar assets. We develop a framework to jointly identify similar assets through factors, identify mispricing and form a trading poli...