Academic Profile

Statistics

Similar Authors

Papers on arXiv

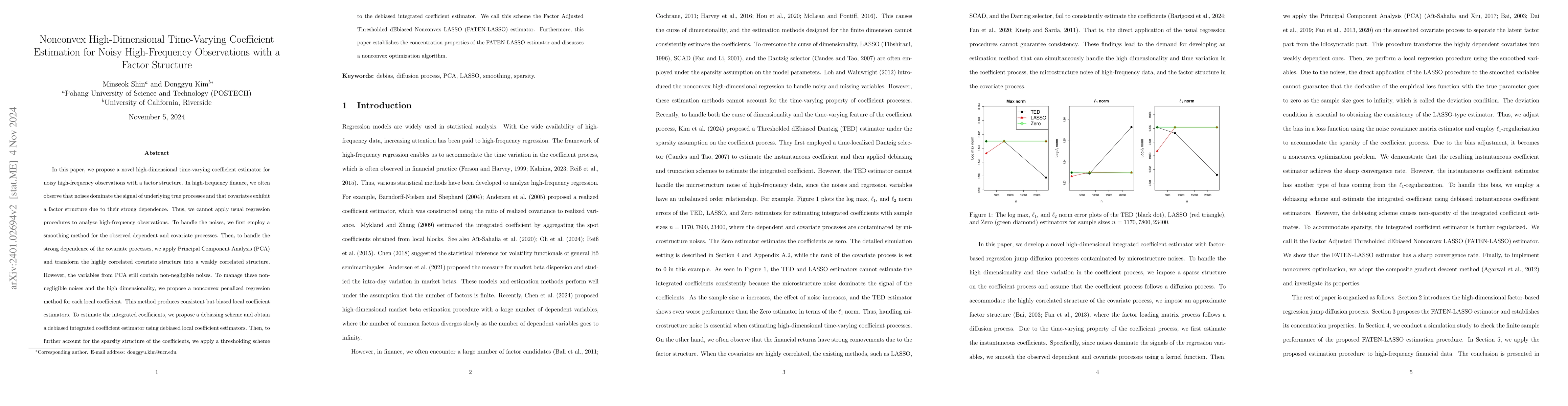

In this paper, we propose a novel high-dimensional time-varying coefficient estimator for noisy high-frequency observations. In high-frequency finance, we often observe that noises dominate a signal...

In this paper, we develop a novel high-dimensional coefficient estimation procedure based on high-frequency data. Unlike usual high-dimensional regression procedure such as LASSO, we additionally ha...

This paper introduces novel volatility diffusion models to account for the stylized facts of high-frequency financial data such as volatility clustering, intra-day U-shape, and leverage effect. For ...

In this paper, we develop a novel high-dimensional time-varying coefficient estimation method, based on high-dimensional Ito diffusion processes. To account for high-dimensional time-varying coeffic...

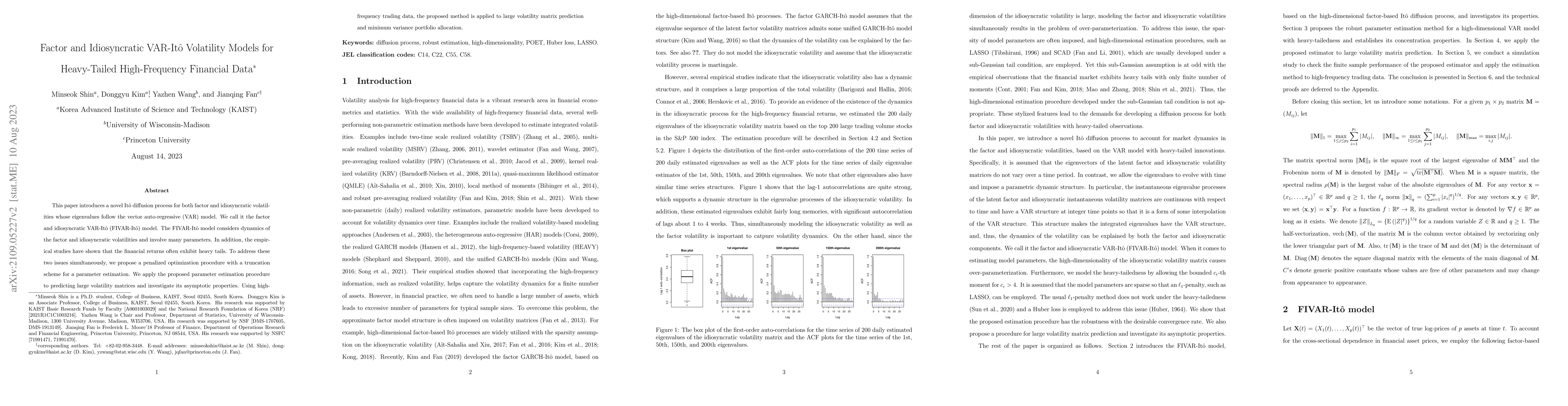

This paper introduces a novel It\^{o} diffusion process for both factor and idiosyncratic volatilities whose eigenvalues follow the vector auto-regressive (VAR) model. We call it the factor and idio...

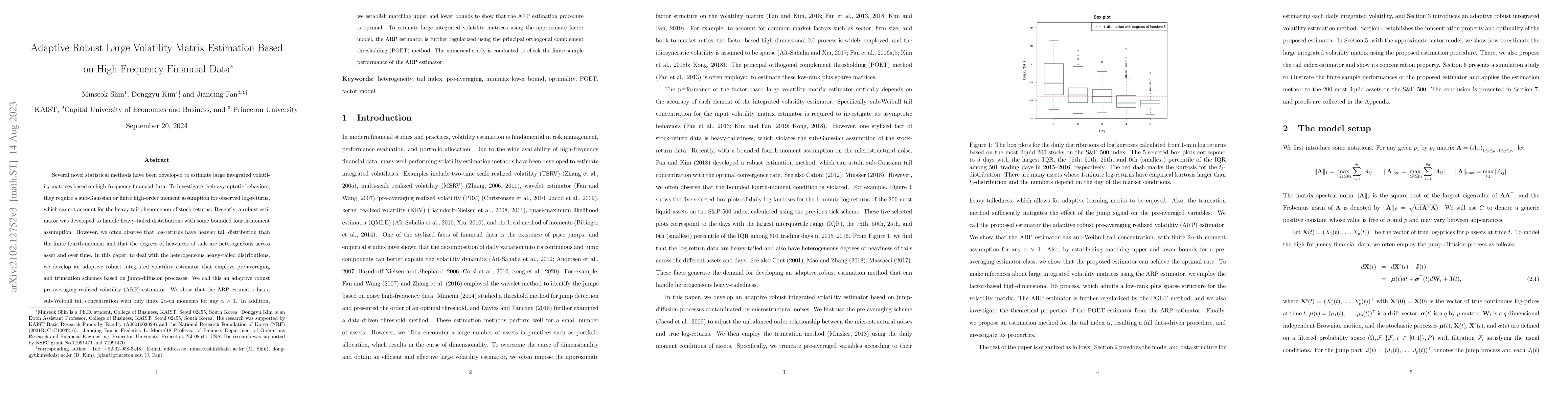

Several novel statistical methods have been developed to estimate large integrated volatility matrices based on high-frequency financial data. To investigate their asymptotic behaviors, they require...