Academic Profile

Statistics

Similar Authors

Papers on arXiv

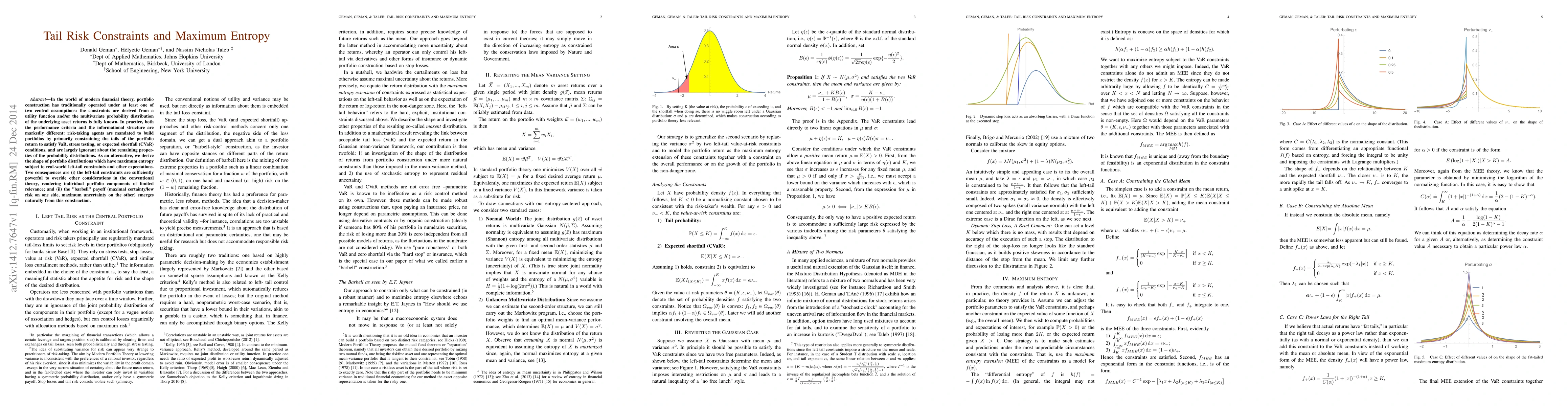

In the world of modern financial theory, portfolio construction has traditionally operated under at least one of two central assumptions: the constraints are derived from a utility function and/or t...

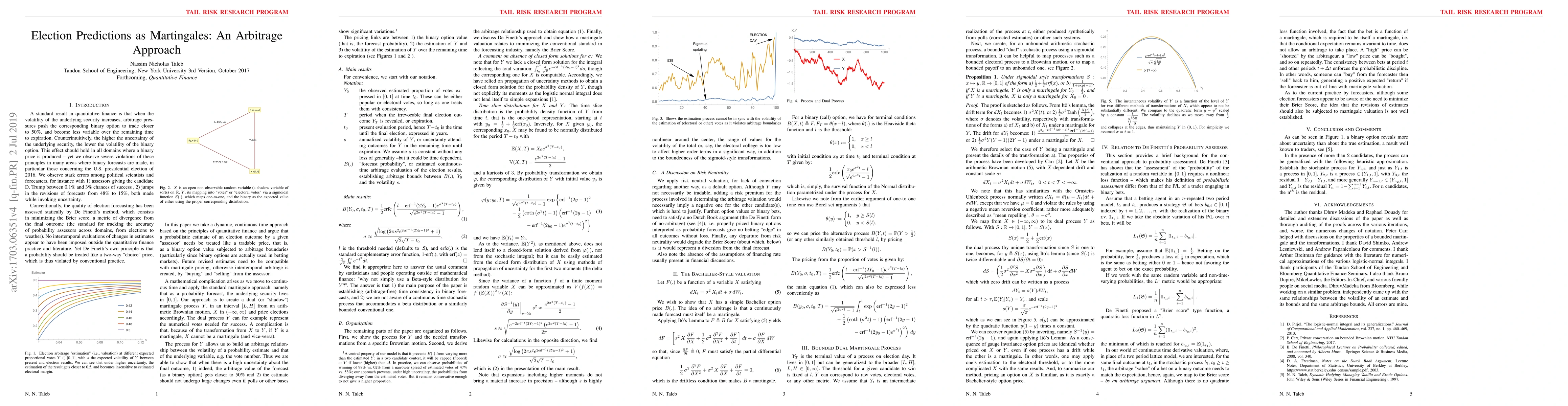

We consider the estimation of binary election outcomes as martingales and propose an arbitrage pricing when one continuously updates estimates. We argue that the estimator needs to be priced as a bi...

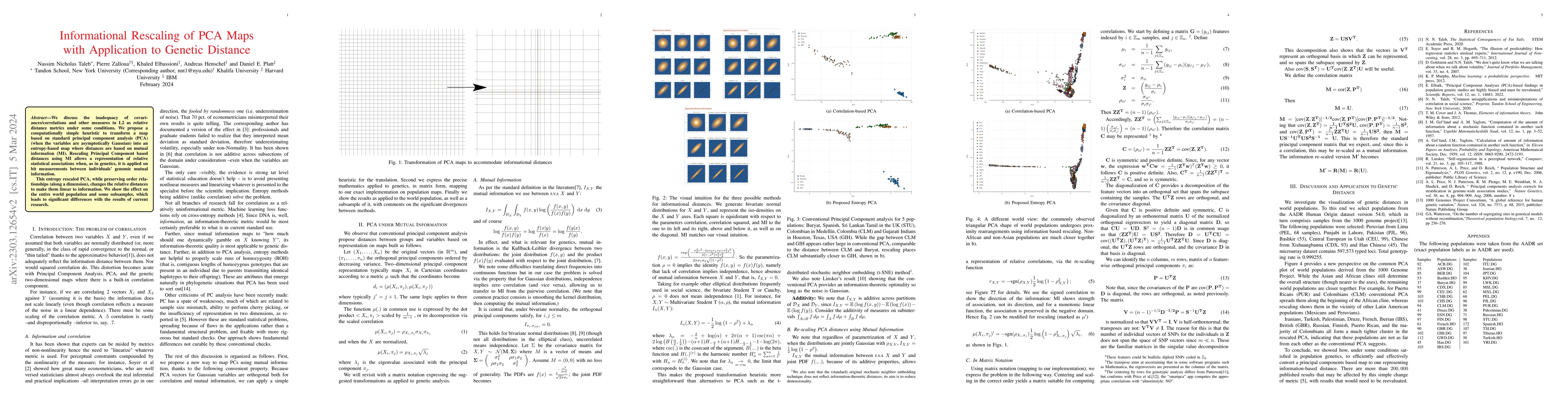

We discuss the inadequacy of covariances/correlations and other measures in L2 as relative distance metrics under some conditions. We propose a computationally simple heuristic to transform a map ba...

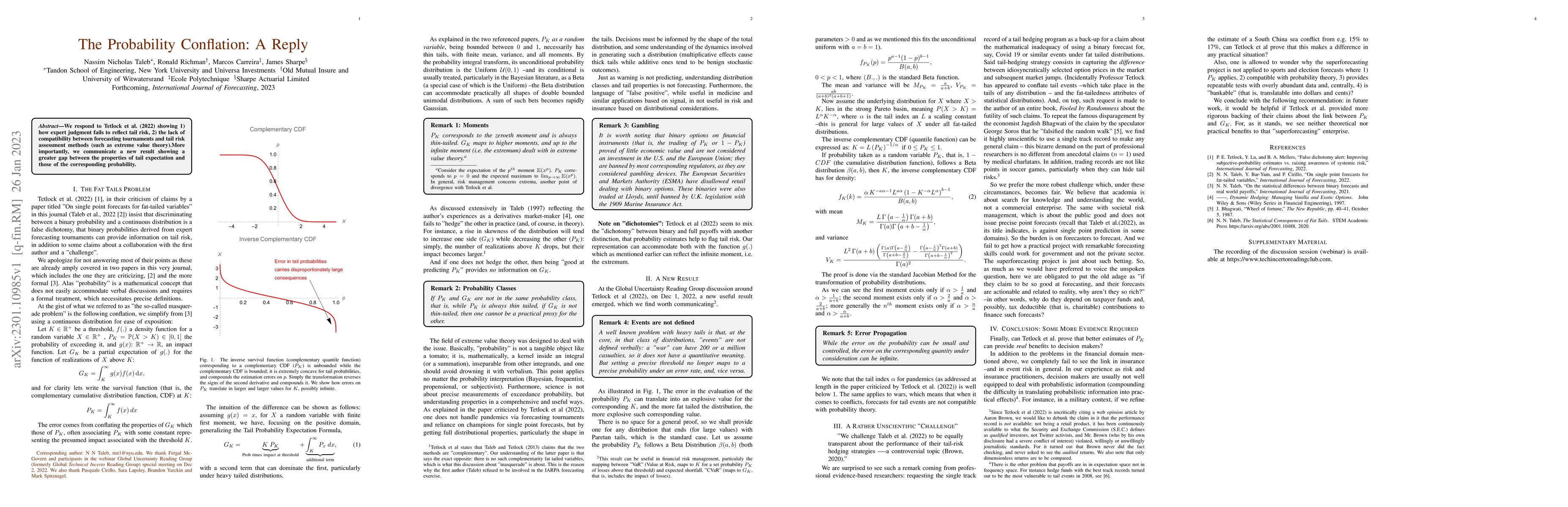

We respond to Tetlock et al. (2022) showing 1) how expert judgment fails to reflect tail risk, 2) the lack of compatibility between forecasting tournaments and tail risk assessment methods (such as ...

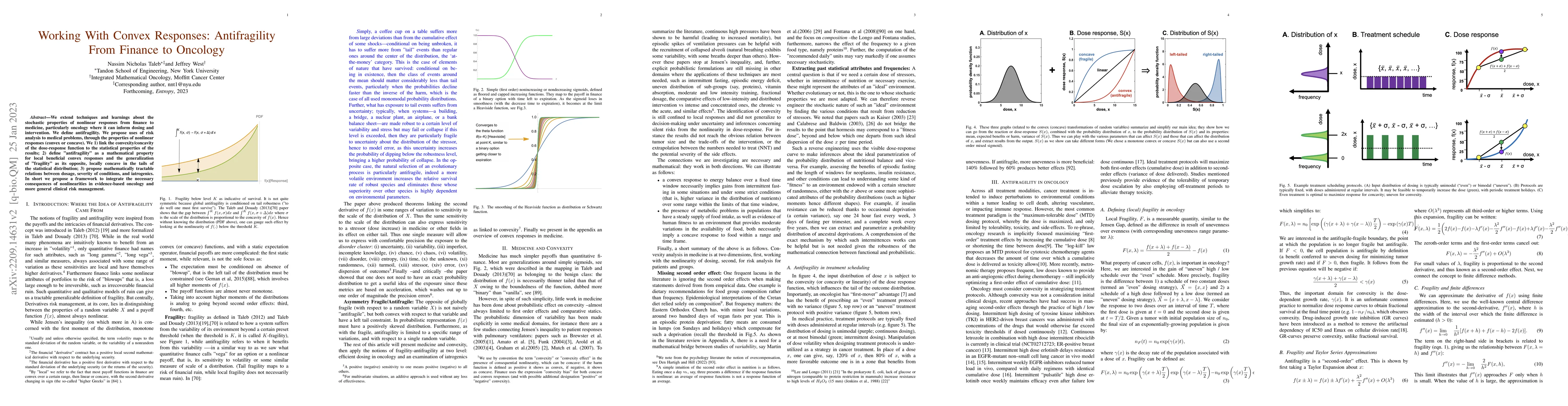

We extend techniques and learnings about the stochastic properties of nonlinear responses from finance to medicine, particularly oncology where it can inform dosing and intervention. We define antif...

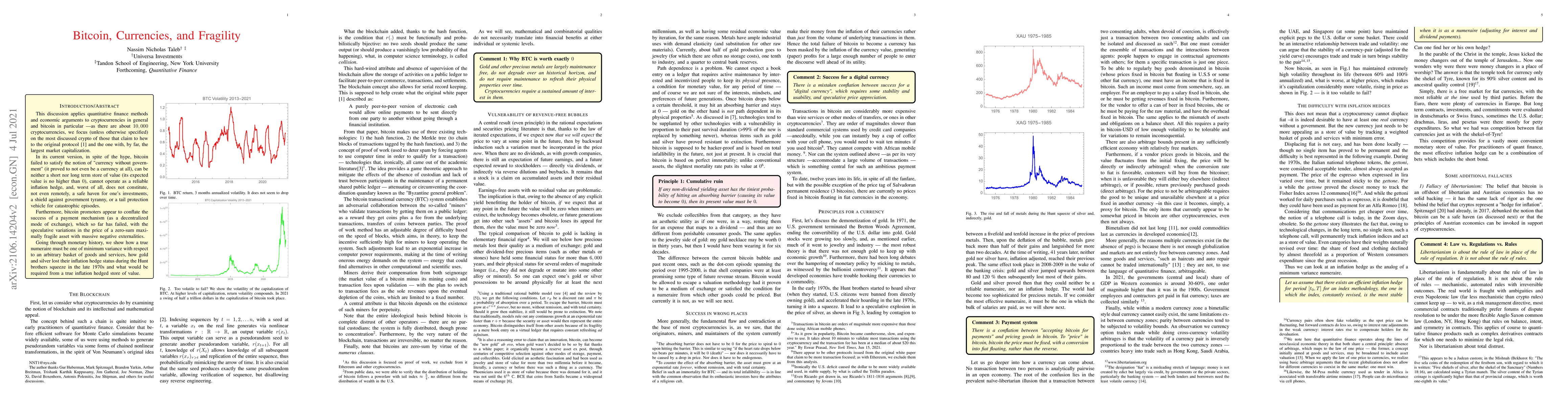

This discussion applies quantitative finance methods and economic arguments to cryptocurrencies in general and bitcoin in particular -- as there are about $10,000$ cryptocurrencies, we focus (unless...

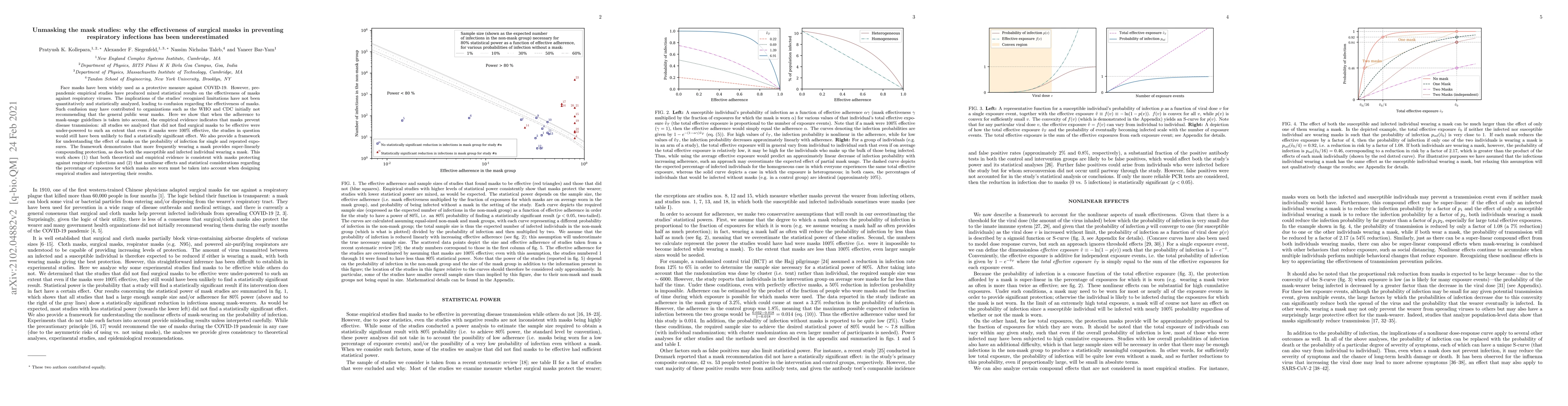

Face masks have been widely used as a protective measure against COVID-19. However, pre-pandemic empirical studies have produced mixed statistical results on the effectiveness of masks against respi...

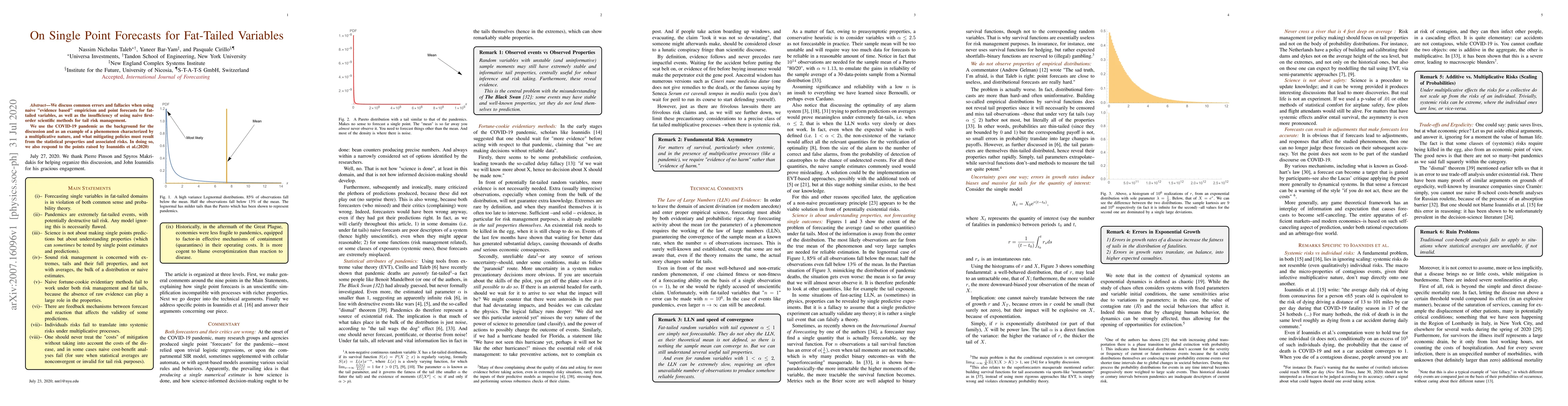

We discuss common errors and fallacies when using naive "evidence based" empiricism and point forecasts for fat-tailed variables, as well as the insufficiency of using naive first-order scientific m...

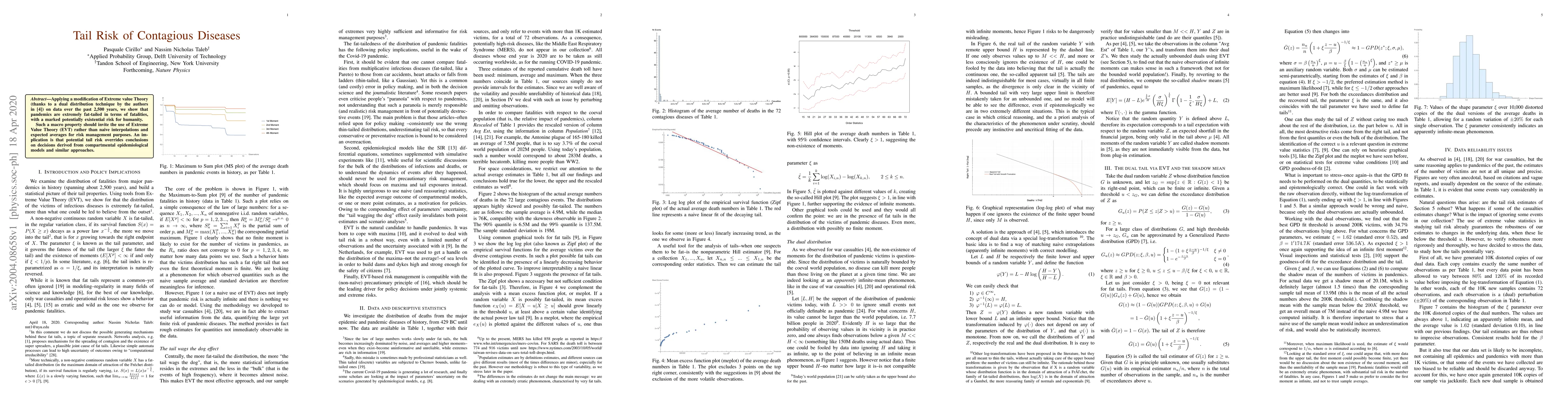

Applying a modification of Extreme value Theory (thanks to a dual distribution technique by the authors on data over the past 2,500 years, we show that pandemics are extremely fat-tailed in terms of...

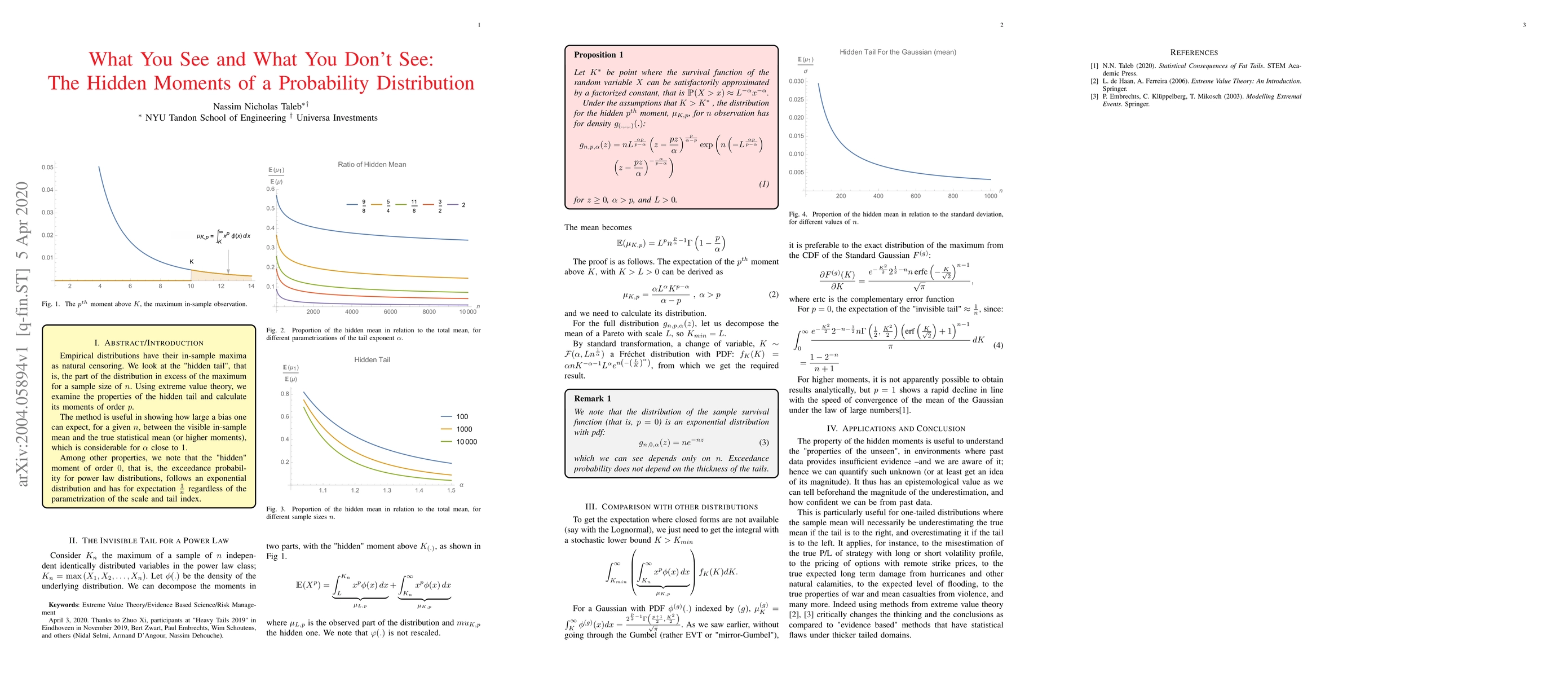

Empirical distributions have their in-sample maxima as natural censoring. We look at the "hidden tail", that is, the part of the distribution in excess of the maximum for a sample size of $n$. Using...

The monograph investigates the misapplication of conventional statistical techniques to fat tailed distributions and looks for remedies, when possible. Switching from thin tailed to fat tailed dis...

This is an epistemological approach to errors in both inference and risk management, leading to necessary structural properties for the probability distribution. Many mechanisms have been used to ...

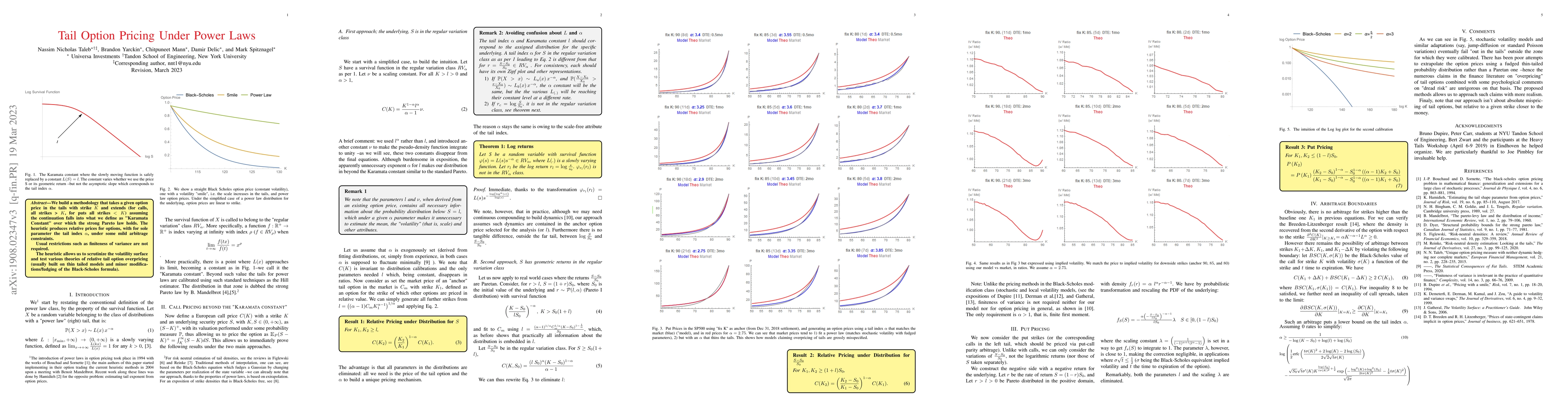

We build a methodology that takes a given option price in the tails with strike $K$ and extends (for calls, all strikes > $K$, for puts all strikes $< K$) assuming the continuation falls into what w...