01

MethodologyHow they did it

The research methodology used a pseudo-density function to build intuition for tail option pricing under power laws.

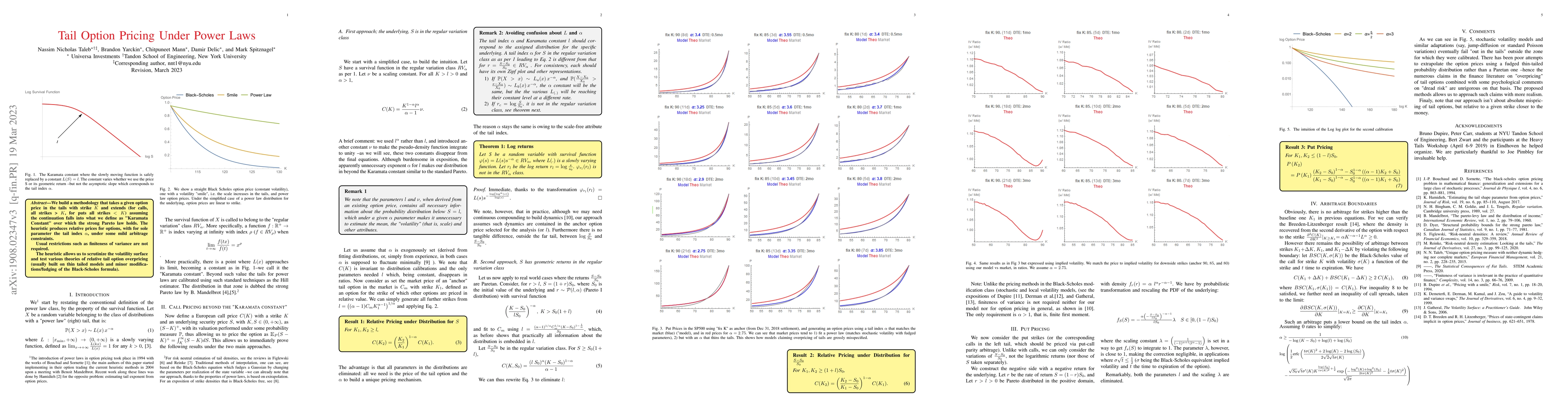

This paper proposes a novel methodology for tail option pricing based on power laws, extending option prices under the "Karamata Constant" assumption, which adheres to the strong Pareto law. The method uses only the tail index $\alpha$ as a parameter, without requiring finite variance, and can test theories of relative tail option overpricing.

The research methodology used a pseudo-density function to build intuition for tail option pricing under power laws. More in Methodology →

Relative Pricing under Distribution for S — Relative Pricing under Distribution for S−S0S0 More in Key Results →

This research provides a novel approach to pricing tail options, allowing for relative prices based on the tail index α and eliminating the need for finiteness of variance. More in Significance →

Fudged thin-tailed probability distribution may not capture the underlying distribution accurately — Model may not be suitable for all types of assets or market conditions More in Limitations →

We build a methodology that takes a given option price in the tails with strike $K$ and extends (for calls, all strikes > $K$, for puts all strikes $< K$) assuming the continuation falls into what we define as "Karamata Constant" over which the strong Pareto law holds. The heuristic produces relative prices for options, with for sole parameter the tail index $\alpha$, under some mild arbitrage constraints. Usual restrictions such as finiteness of variance are not required. The methodology allows us to scrutinize the volatility surface and test various theories of relative tail option overpricing (usually built on thin tailed models and minor modifications/fudging of the Black-Scholes formula).

Seven facets of this paper, analysed and brought into focus by AI.

This research provides a novel approach to pricing tail options, allowing for relative prices based on the tail index α and eliminating the need for finiteness of variance.

The research methodology used a pseudo-density function to build intuition for tail option pricing under power laws.

This research provides a novel approach to pricing tail options, allowing for relative prices based on the tail index α and eliminating the need for finiteness of variance.

The research introduces a new approach to pricing tail options using power laws and eliminates the need for finiteness of variance.

This work is novel in its use of power laws to price tail options and its ability to eliminate the need for finiteness of variance.

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0