Academic Profile

Statistics

Similar Authors

Papers on arXiv

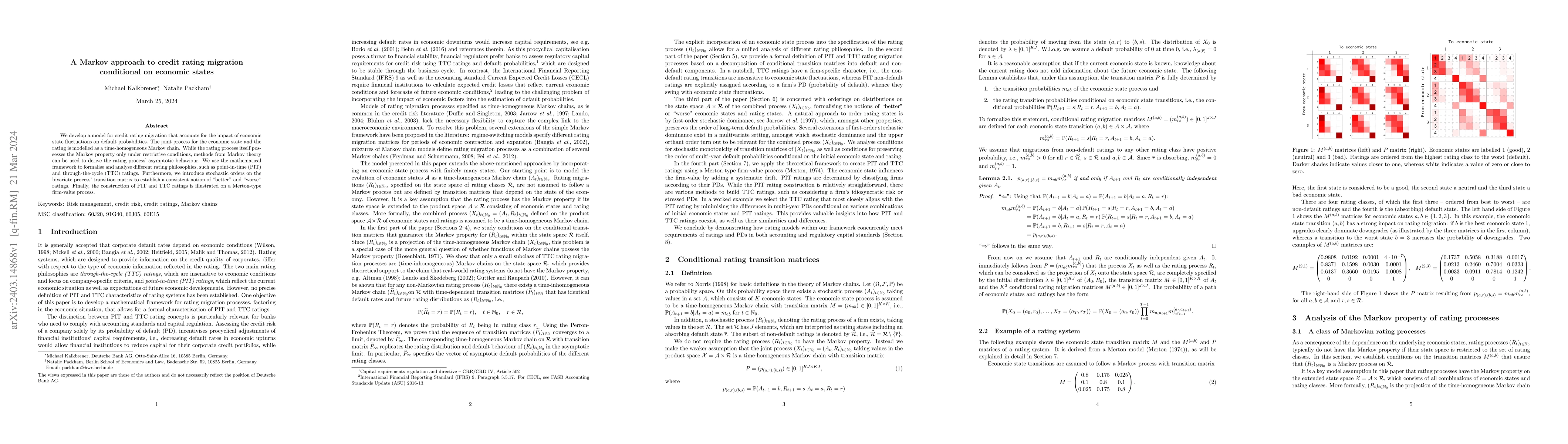

We develop a model for credit rating migration that accounts for the impact of economic state fluctuations on default probabilities. The joint process for the economic state and the rating is modell...

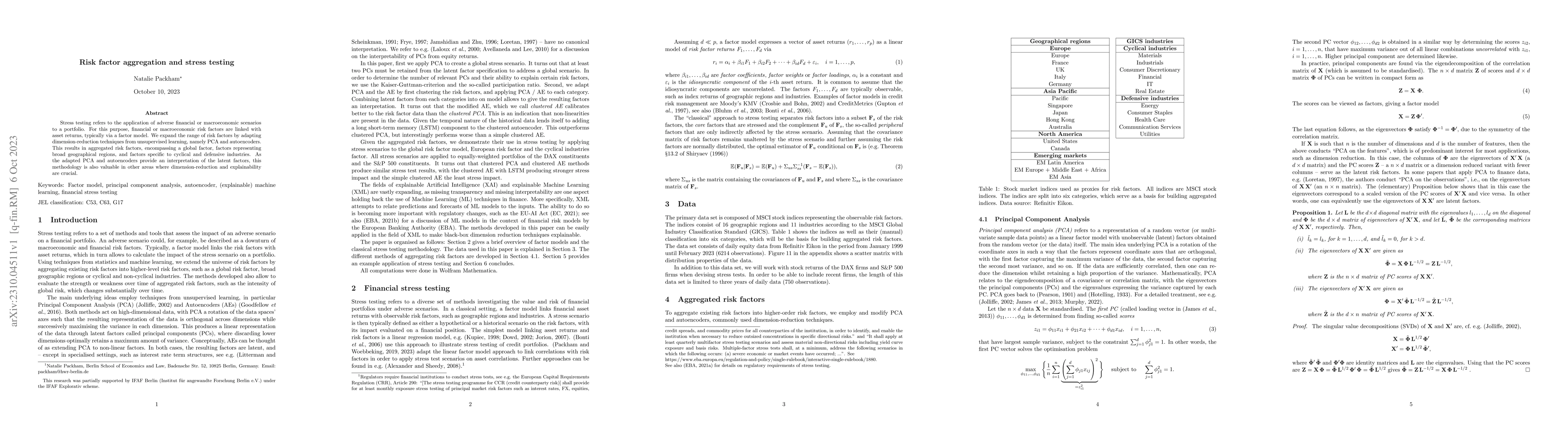

Stress testing refers to the application of adverse financial or macroeconomic scenarios to a portfolio. For this purpose, financial or macroeconomic risk factors are linked with asset returns, typi...

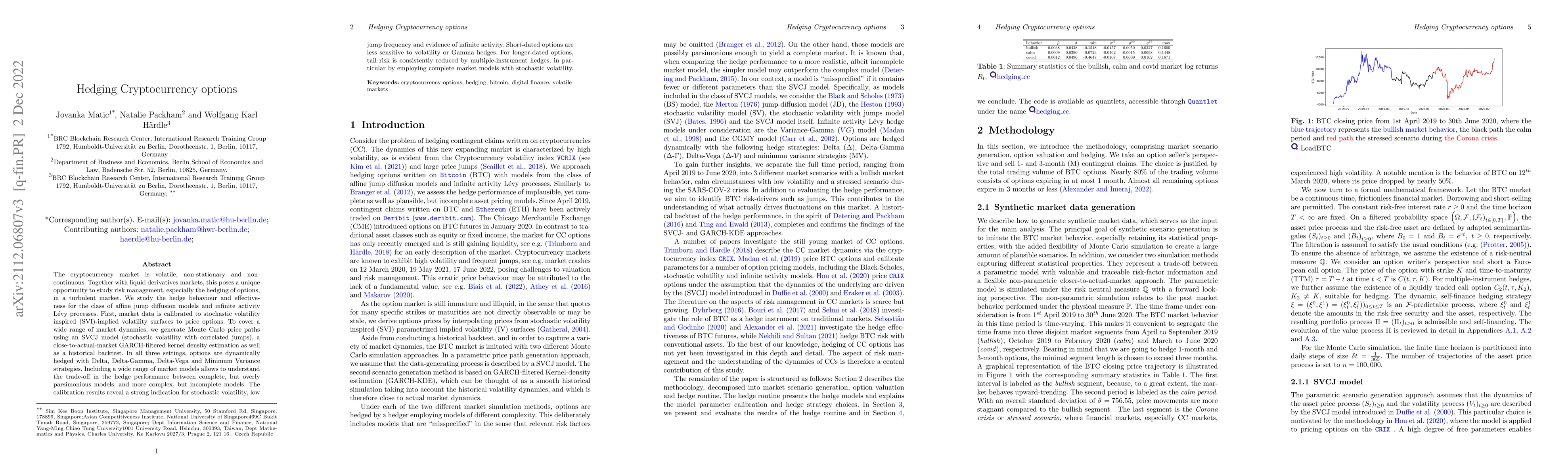

The cryptocurrency market is volatile, non-stationary and non-continuous. Together with liquid derivatives markets, this poses a unique opportunity to study risk management, especially the hedging o...

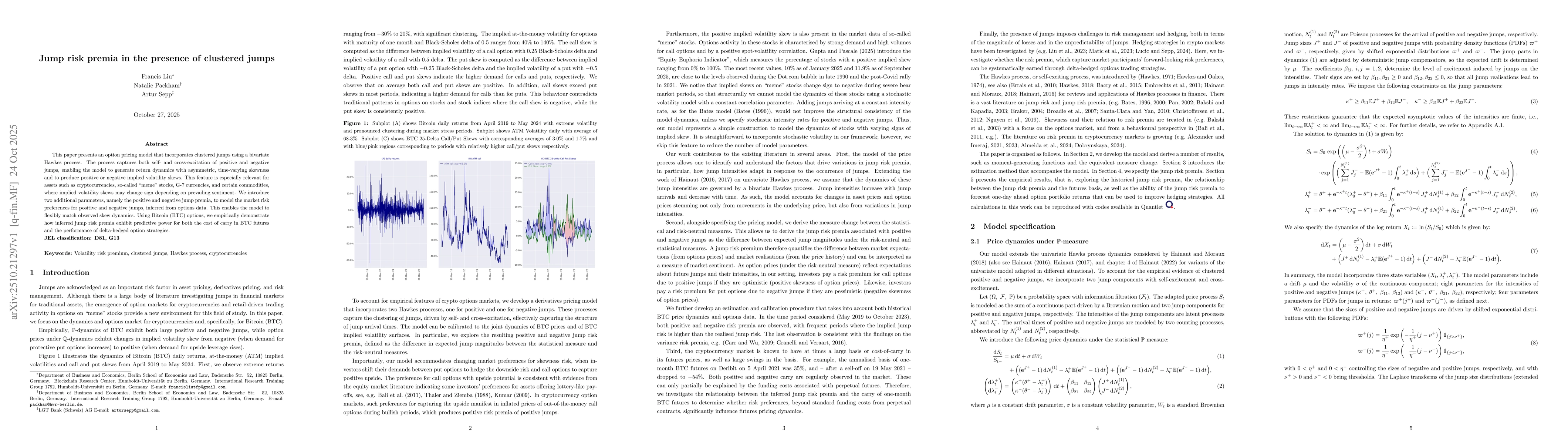

This paper presents an option pricing model that incorporates clustered jumps using a bivariate Hawkes process. The process captures both self- and cross-excitation of positive and negative jumps, ena...