Academic Profile

Statistics

Similar Authors

Papers on arXiv

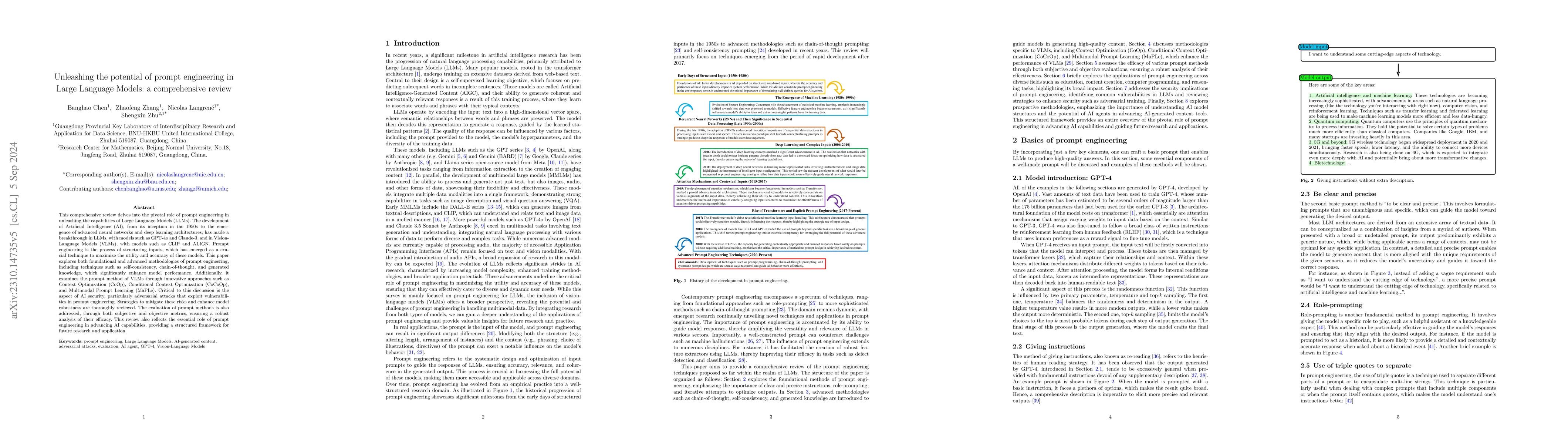

This paper delves into the pivotal role of prompt engineering in unleashing the capabilities of Large Language Models (LLMs). Prompt engineering is the process of structuring input text for LLMs and i...

In this paper, we present a probabilistic numerical algorithm combining dynamic programming, Monte Carlo simulations and local basis regressions to solve non-stationary optimal multiple switching pr...

We propose a probabilistic numerical algorithm to solve Backward Stochastic Differential Equations (BSDEs) with nonnegative jumps, a class of BSDEs introduced in [9] for representing fully nonlinear...

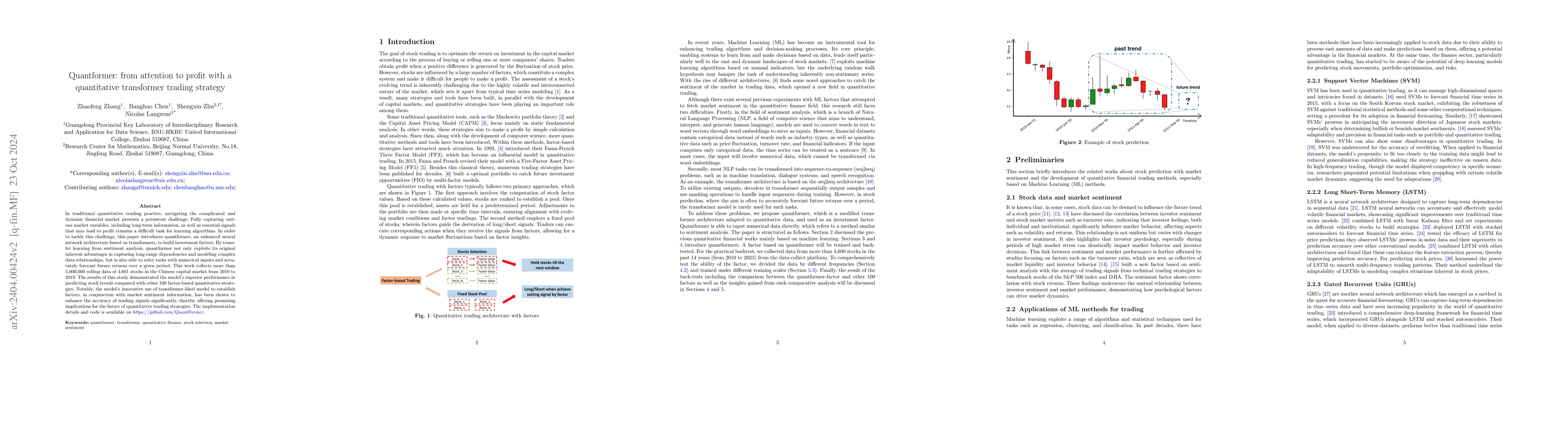

In traditional quantitative trading practice, navigating the complicated and dynamic financial market presents a persistent challenge. Former machine learning approaches have struggled to fully capt...

Indexes are useful for summarizing multivariate information into single metrics for monitoring, communicating, and decision-making. While most work has focused on defining new indexes for specific p...

In this paper, we introduce two methods to solve the American-style option pricing problem and its dual form at the same time using neural networks. Without applying nested Monte Carlo, the first me...

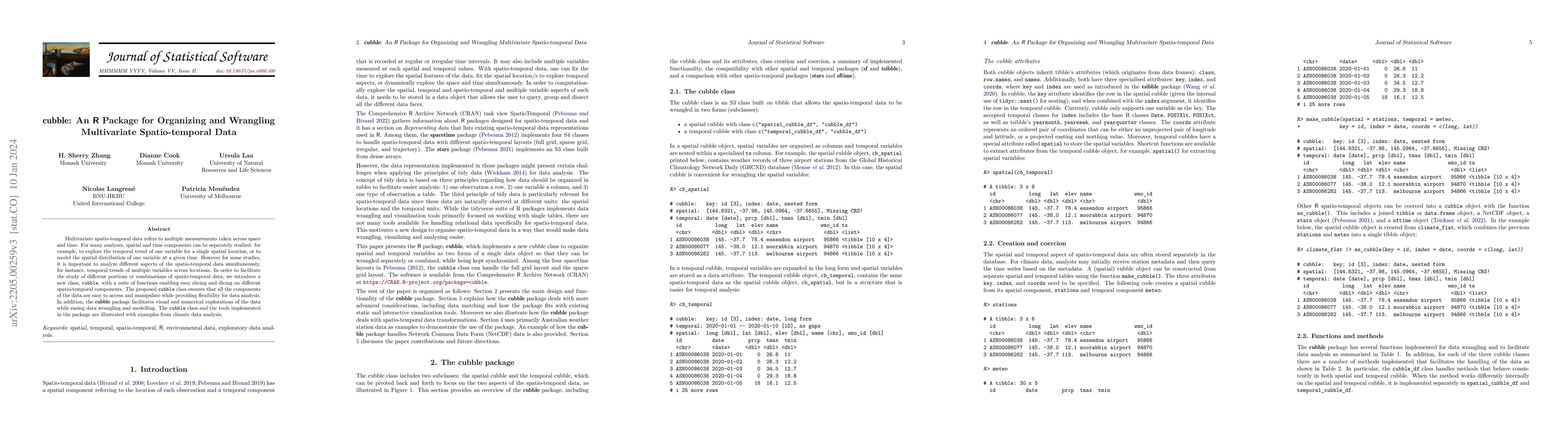

Multivariate spatio-temporal data refers to multiple measurements taken across space and time. For many analyses, spatial and time components can be separately studied: for example, to explore the t...

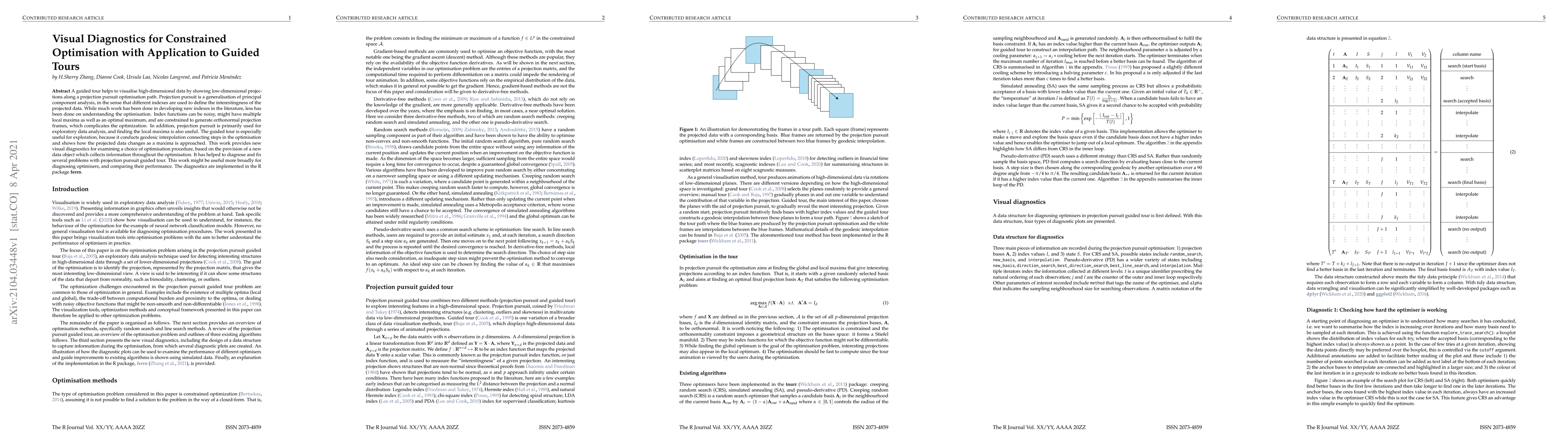

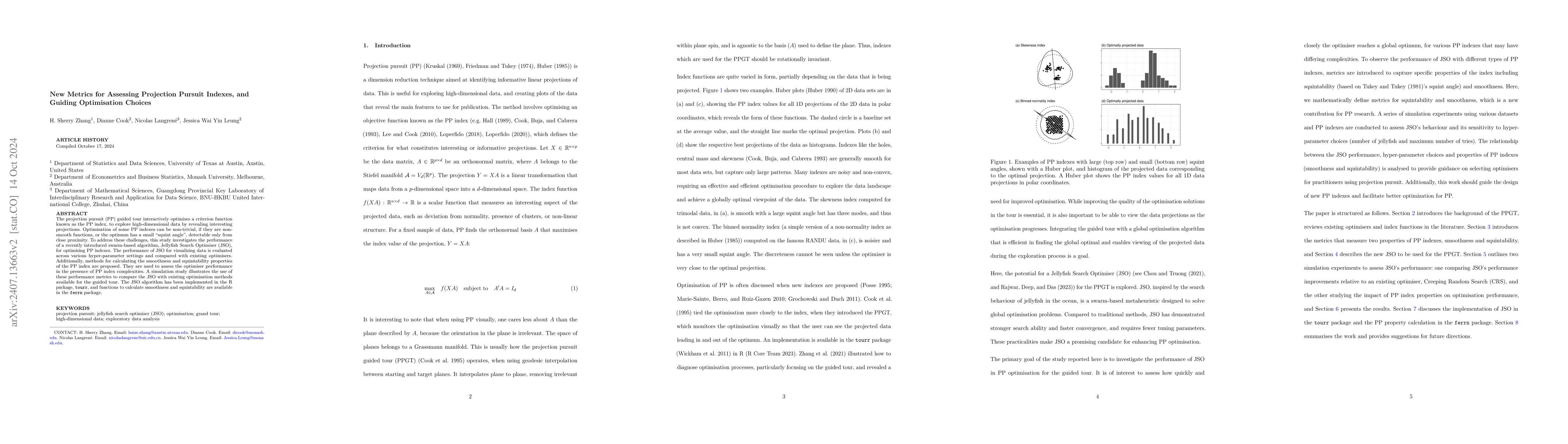

A guided tour helps to visualise high-dimensional data by showing low-dimensional projections along a projection pursuit optimisation path. Projection pursuit is a generalisation of principal compon...

We propose two deep neural network-based methods for solving semi-martingale optimal transport problems. The first method is based on a relaxation/penalization of the terminal constraint, and is sol...

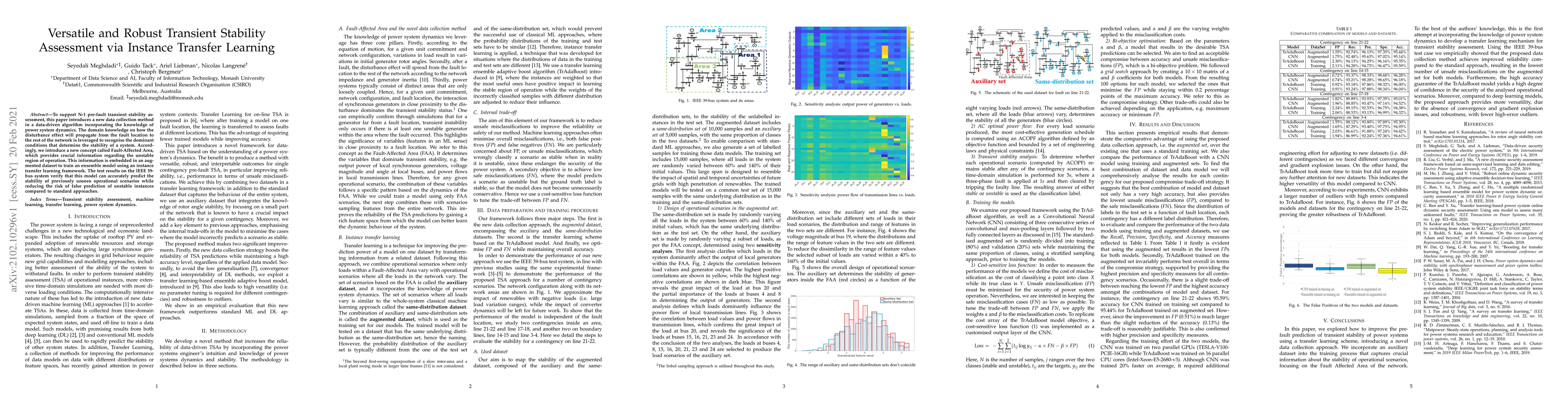

To support N-1 pre-fault transient stability assessment, this paper introduces a new data collection method in a data-driven algorithm incorporating the knowledge of power system dynamics. The domai...

This paper studies a portfolio allocation problem, where the goal is to prescribe the wealth distribution at the final time. We study this problem with the tools of optimal mass transport. We provid...

The recently developed rough Bergomi (rBergomi) model is a rough fractional stochastic volatility (RFSV) model which can generate more realistic term structure of at-the-money volatility skews compa...

We obtain an explicit approximation formula for European put option prices within a general stochastic volatility model with time-dependent parameters. Our methodology involves writing the put optio...

This paper addresses the problem of utility maximization under uncertain parameters. In contrast with the classical approach, where the parameters of the model evolve freely within a given range, we...

We consider closed-form approximations for European put option prices within the Heston and GARCH diffusion stochastic volatility models with time-dependent parameters. Our methodology involves writ...

This paper presents several numerical applications of deep learning-based algorithms that have been introduced in [HPBL18]. Numerical and comparative tests using TensorFlow illustrate the performanc...

The projection pursuit (PP) guided tour interactively optimises a criteria function known as the PP index, to explore high-dimensional data by revealing interesting projections. The optimisation in PP...

Rahimi and Recht [31] introduced the idea of decomposing shift-invariant kernels by randomly sampling from their spectral distribution. This famous technique, known as Random Fourier Features (RFF), i...

To speed up Gaussian process inference, a number of fast kernel matrix-vector multiplication (MVM) approximation algorithms have been proposed over the years. In this paper, we establish an exact fast...

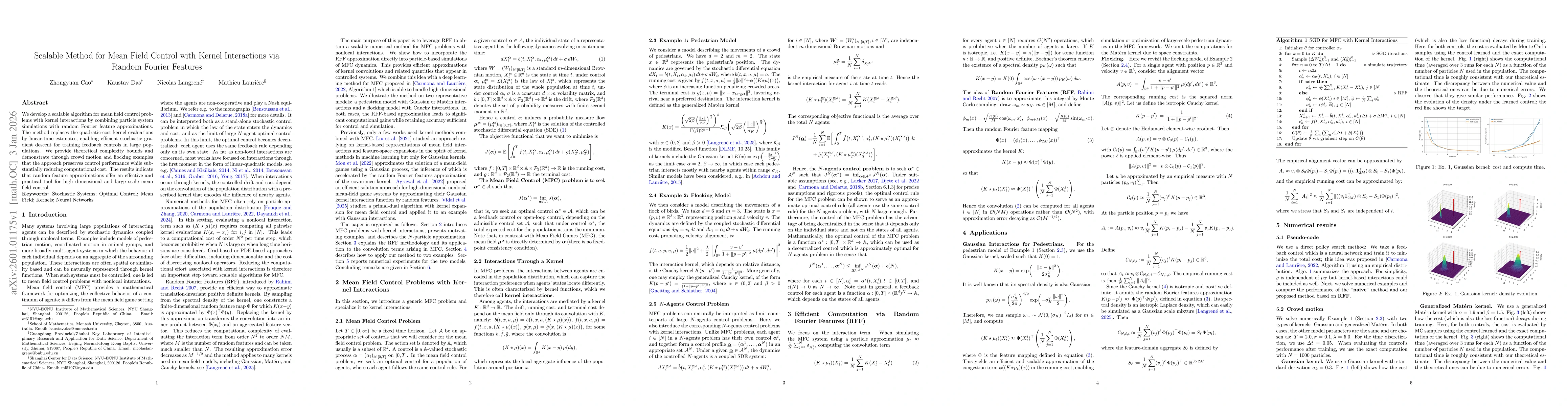

We develop a scalable algorithm for mean field control problems with kernel interactions by combining particle system simulations with random Fourier feature approximations. The method replaces the qu...

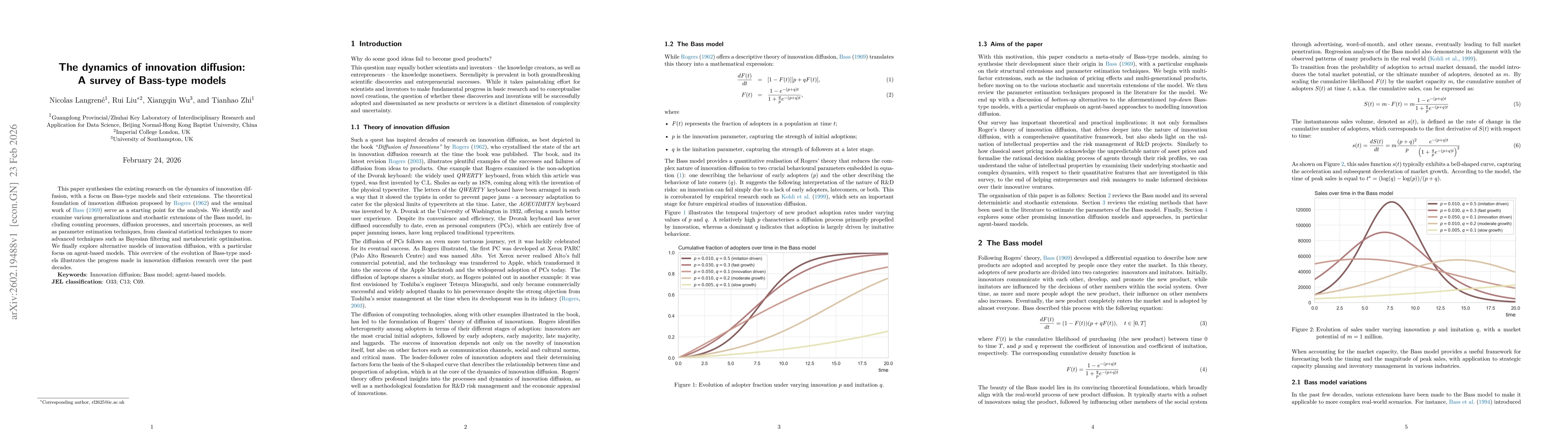

This paper synthesises the existing research on the dynamics of innovation diffusion, with a focus on Bass-type models and their extensions. The theoretical foundation of innovation diffusion proposed...

A fast simulation framework for stochastic Volterra processes based on Random Fourier Features (RFF) approximation of the kernel is developed. After recalling the main properties of Volterra processes...

This paper develops a deep learning-based framework for pricing convertible bonds with path-dependent contractual features, namely downward conversion price reset and issuer call clauses under rolling...

In general, the pricing of variable annuities with guarantees can be done by solving the corresponding optimal stochastic control problem if the contract withdrawal strategy is assumed to be optimal. ...