Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this research note, we revisit the bandits with expert advice problem. Under a restricted feedback model, we prove a lower bound of order $\sqrt{K T \ln(N/K)}$ for the worst-case regret, where $K$ ...

Can a deep neural network be approximated by a small decision tree based on simple features? This question and its variants are behind the growing demand for machine learning models that are *interp...

We study stochastic linear bandits where, in each round, the learner receives a set of actions (i.e., feature vectors), from which it chooses an element and obtains a stochastic reward. The expected...

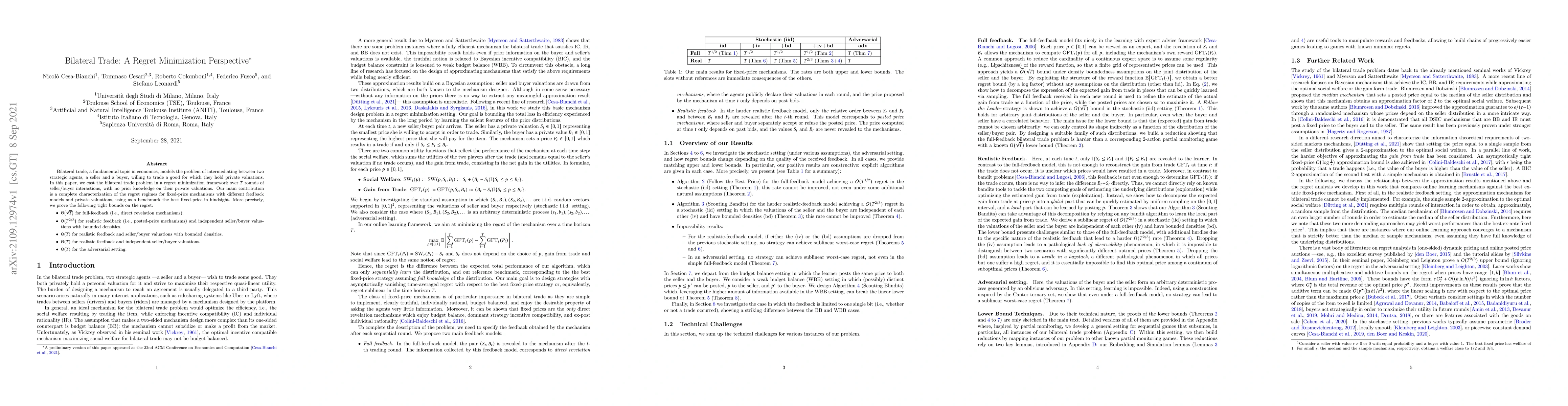

In online bilateral trade, a platform posts prices to incoming pairs of buyers and sellers that have private valuations for a certain good. If the price is lower than the buyers' valuation and highe...

This work addresses the mediator feedback problem, a bandit game where the decision set consists of a number of policies, each associated with a probability distribution over a common space of outco...

We study best-of-both-worlds algorithms for $K$-armed linear contextual bandits. Our algorithms deliver near-optimal regret bounds in both the adversarial and stochastic regimes, without prior knowl...

Many online decision-making problems correspond to maximizing a sequence of submodular functions. In this work, we introduce sum-max functions, a subclass of monotone submodular functions capturing ...

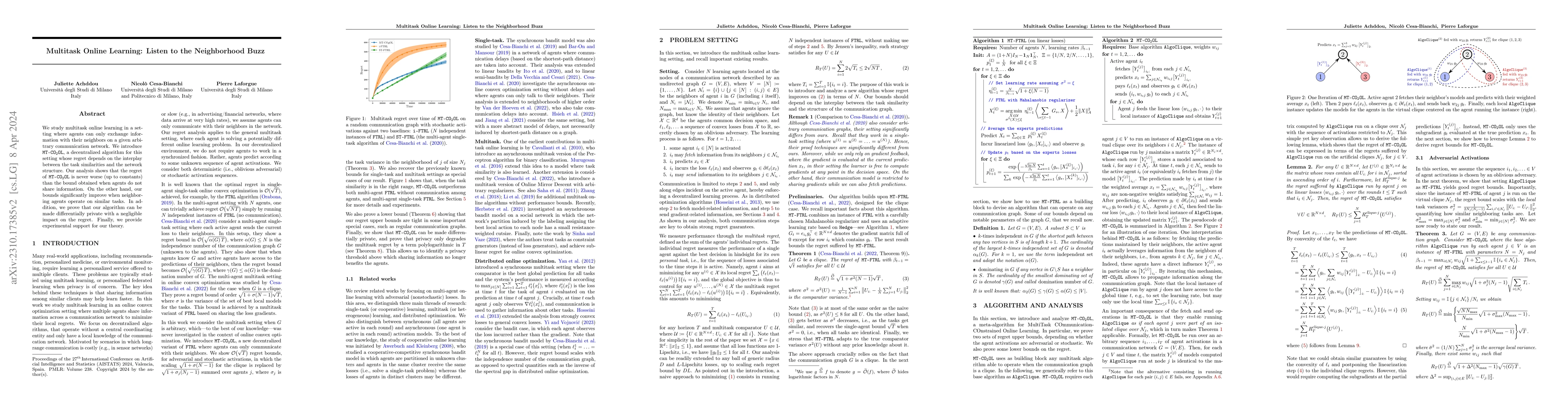

We study multitask online learning in a setting where agents can only exchange information with their neighbors on an arbitrary communication network. We introduce $\texttt{MT-CO}_2\texttt{OL}$, a d...

Online learning methods yield sequential regret bounds under minimal assumptions and provide in-expectation risk bounds for statistical learning. However, despite the apparent advantage of online gu...

Multitask learning is a powerful framework that enables one to simultaneously learn multiple related tasks by sharing information between them. Quantifying uncertainty in the estimated tasks is of p...

We study the problem of regret minimization for a single bidder in a sequence of first-price auctions where the bidder discovers the item's value only if the auction is won. Our main contribution is...

We study a $K$-armed bandit with delayed feedback and intermediate observations. We consider a model where intermediate observations have a form of a finite state, which is observed immediately afte...

In this work, we improve on the upper and lower bounds for the regret of online learning with strongly observable undirected feedback graphs. The best known upper bound for this problem is $\mathcal...

We investigate the problem of bandits with expert advice when the experts are fixed and known distributions over the actions. Improving on previous analyses, we show that the regret in this setting ...

We study repeated bilateral trade where an adaptive $\sigma$-smooth adversary generates the valuations of sellers and buyers. We provide a complete characterization of the regret regimes for fixed-p...

Nonstationary phenomena, such as satiation effects in recommendations, have mostly been modeled using bandits with finitely many arms. However, the richer action space provided by linear bandits is ...

The framework of feedback graphs is a generalization of sequential decision-making with bandit or full information feedback. In this work, we study an extension where the directed feedback graph is ...

We study exact active learning of binary and multiclass classifiers with margin. Given an $n$-point set $X \subset \mathbb{R}^m$, we want to learn any unknown classifier on $X$ whose classes have fi...

We study a repeated game between a supplier and a retailer who want to maximize their respective profits without full knowledge of the problem parameters. After characterizing the uniqueness of the ...

We consider prediction with expert advice for strongly convex and bounded losses, and investigate trade-offs between regret and "variance" (i.e., squared difference of learner's predictions and best...

We consider online learning with feedback graphs, a sequential decision-making framework where the learner's feedback is determined by a directed graph over the action set. We present a computationa...

We introduce and analyze AdaTask, a multitask online learning algorithm that adapts to the unknown structure of the tasks. When the $N$ tasks are stochastically activated, we show that the regret of...

We investigate a nonstochastic bandit setting in which the loss of an action is not immediately charged to the player, but rather spread over the subsequent rounds in an adversarial way. The instant...

We study nonstochastic bandits and experts in a delayed setting where delays depend on both time and arms. While the setting in which delays only depend on time has been extensively studied, the arm...

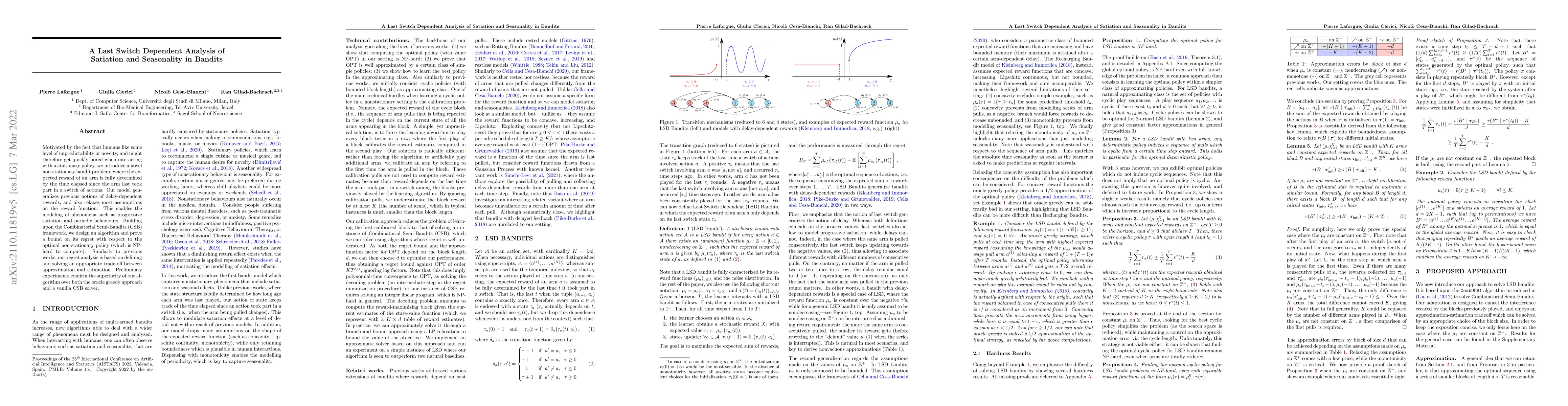

Motivated by the fact that humans like some level of unpredictability or novelty, and might therefore get quickly bored when interacting with a stationary policy, we introduce a novel non-stationary...

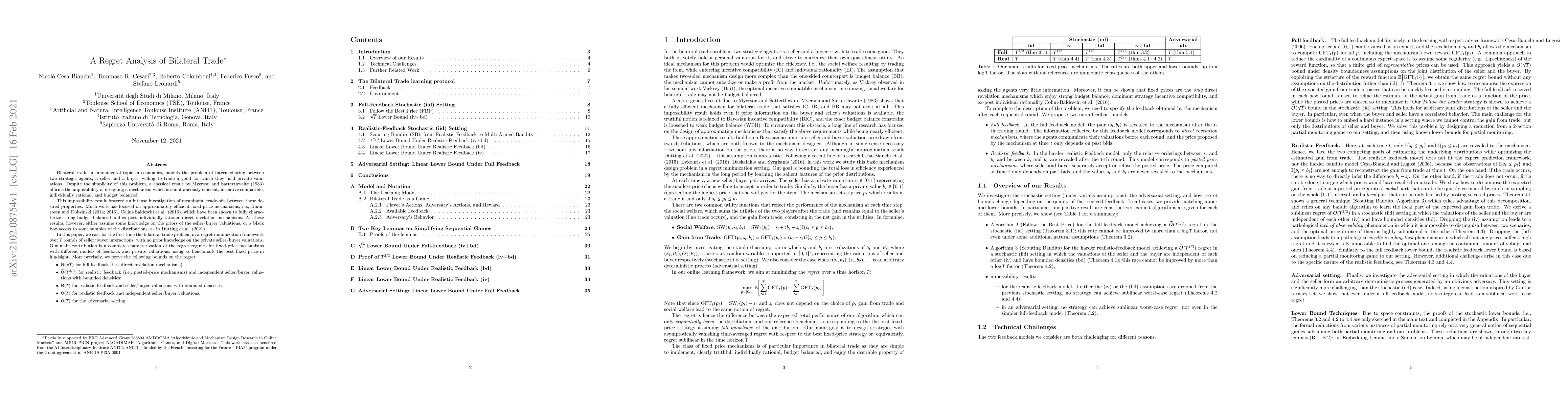

Bilateral trade, a fundamental topic in economics, models the problem of intermediating between two strategic agents, a seller and a buyer, willing to trade a good for which they hold private valuat...

We study the interplay between feedback and communication in a cooperative online learning setting where a network of agents solves a task in which the learners' feedback is determined by an arbitra...

We study an active cluster recovery problem where, given a set of $n$ points and an oracle answering queries like "are these two points in the same cluster?", the task is to recover exactly all clus...

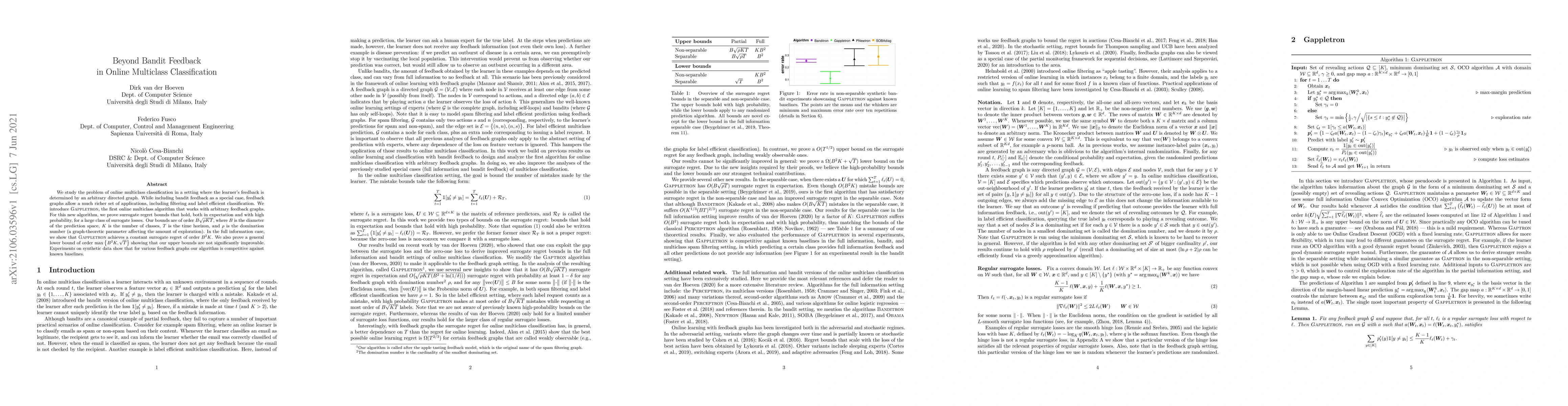

We study the problem of online multiclass classification in a setting where the learner's feedback is determined by an arbitrary directed graph. While including bandit feedback as a special case, fe...

We introduce and analyze MT-OMD, a multitask generalization of Online Mirror Descent (OMD) which operates by sharing updates between tasks. We prove that the regret of MT-OMD is of order $\sqrt{1 + ...

We propose an algorithm for stochastic and adversarial multiarmed bandits with switching costs, where the algorithm pays a price $\lambda$ every time it switches the arm being played. Our algorithm ...

Bilateral trade, a fundamental topic in economics, models the problem of intermediating between two strategic agents, a seller and a buyer, willing to trade a good for which they hold private valuat...

We investigate the problem of exact cluster recovery using oracle queries. Previous results show that clusters in Euclidean spaces that are convex and separated with a margin can be reconstructed ex...

The ELLIS PhD program is a European initiative that supports excellent young researchers by connecting them to leading researchers in AI. In particular, PhD students are supervised by two advisors f...

We study the cluster recovery problem in the semi-supervised active clustering framework. Given a finite set of input points, and an oracle revealing whether any two points lie in the same cluster, ...

One of the main strengths of online algorithms is their ability to adapt to arbitrary data sequences. This is especially important in nonparametric settings, where performance is measured against ri...

Motivated by recommendation problems in music streaming platforms, we propose a nonstationary stochastic bandit model in which the expected reward of an arm depends on the number of rounds that have...

We investigate multiarmed bandits with delayed feedback, where the delays need neither be identical nor bounded. We first prove that "delayed" Exp3 achieves the $O(\sqrt{(KT + D)\ln K} )$ regret bou...

In correlation clustering, we are given $n$ objects together with a binary similarity score between each pair of them. The goal is to partition the objects into clusters so to minimise the disagreem...

We introduce a novel theoretical framework for Return On Investment (ROI) maximization in repeated decision-making. Our setting is motivated by the use case of companies that regularly receive propo...

We study an asynchronous online learning setting with a network of agents. At each time step, some of the agents are activated, requested to make a prediction, and pay the corresponding loss. The lo...

We prove that two popular linear contextual bandit algorithms, OFUL and Thompson Sampling, can be made efficient using Frequent Directions, a deterministic online sketching technique. More precisely...

We study how the regret guarantees of nonstochastic multi-armed bandits can be improved, if the effective range of the losses in each round is small (e.g. the maximal difference between two losses i...

We consider a sequential decision-making setting where, at every round $t$, a market maker posts a bid price $B_t$ and an ask price $A_t$ to an incoming trader (the taker) with a private valuation for...

Motivated by practical federated learning settings where clients may not be always available, we investigate a variant of distributed online optimization where agents are active with a known probabili...

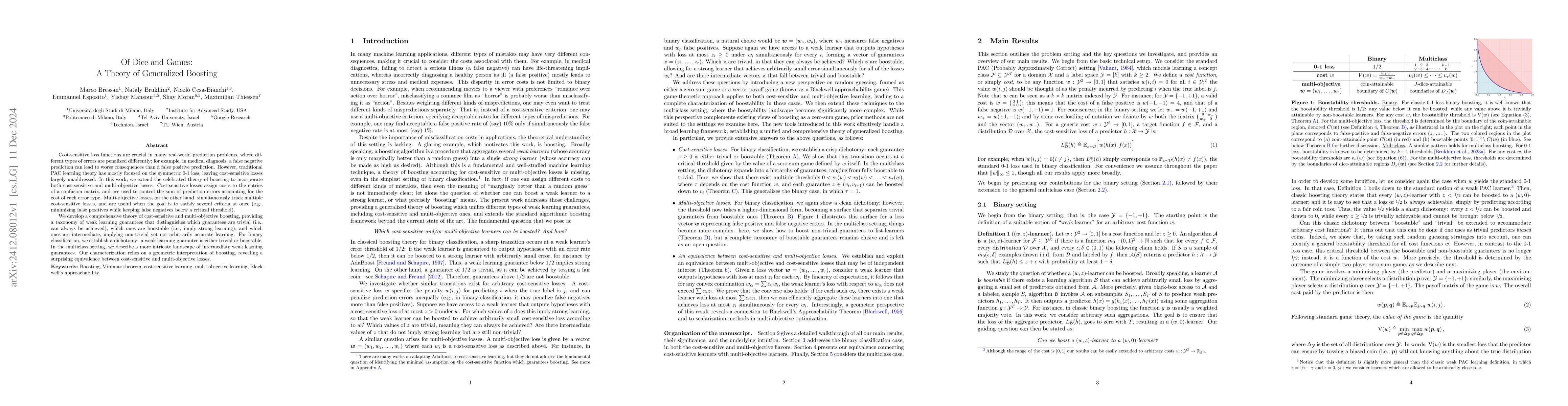

Cost-sensitive loss functions are crucial in many real-world prediction problems, where different types of errors are penalized differently; for example, in medical diagnosis, a false negative predict...

Motivated by applications in crowdsourcing, where a fixed sum of money is split among $K$ workers, and autobidding, where a fixed budget is used to bid in $K$ simultaneous auctions, we define a stocha...

We study the emergence of tacit collusion between adaptive trading agents in a stochastic market with endogenous price formation. Using a two-player repeated game between a market maker and a market t...

In contrast to the classic formulation of partial monitoring, linear partial monitoring can model infinite outcome spaces, while imposing a linear structure on both the losses and the observations. Th...

We study an online linear regression setting in which the observed feature vectors are corrupted by noise and the learner can pay to reduce the noise level. In practice, this may happen for several re...

We study distributed adversarial bandits, where $N$ agents cooperate to minimize the global average loss while observing only their own local losses. We show that the minimax regret for this problem i...

We study an identification problem in multi-armed bandits. In each round a learner selects one of $K$ arms and observes its reward, with the goal of eventually identifying an arm that will perform bes...

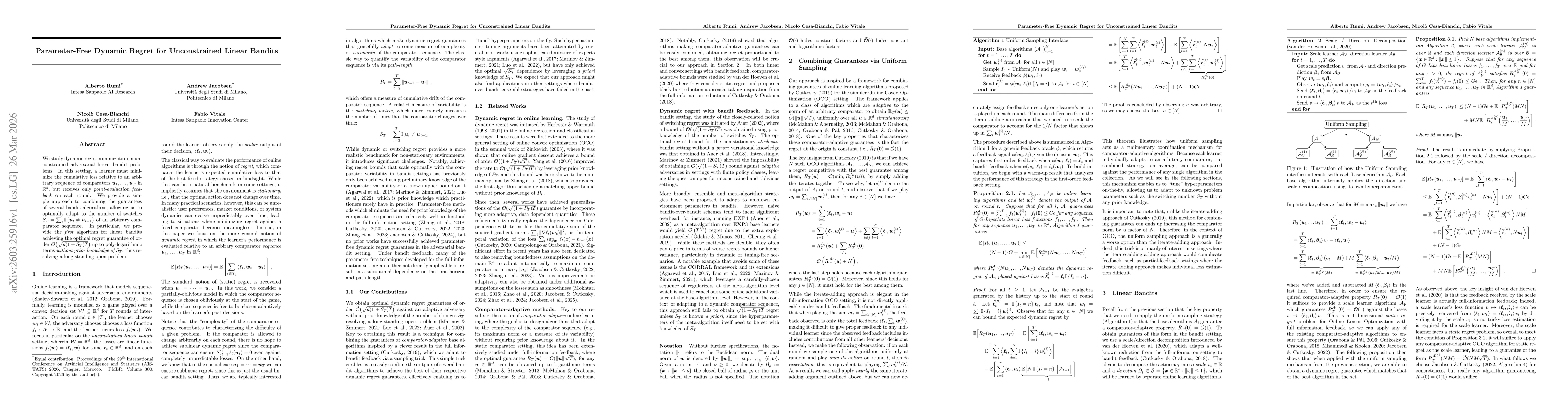

We study dynamic regret minimization in unconstrained adversarial linear bandit problems. In this setting, a learner must minimize the cumulative loss relative to an arbitrary sequence of comparators ...

We revisit the standard perturbation-based approach of Abernethy et al. (2008) in the context of unconstrained Bandit Linear Optimization (uBLO). We show the surprising result that in the unconstraine...

We develop parameter-free algorithms for unconstrained online learning with regret guarantees that scale with the gradient variation $V_T(u) = \sum_{t=2}^T \|\nabla f_t(u)-\nabla f_{t-1}(u)\|^2$. For ...

Motivated by real-world scenarios where malicious entities tamper with existing networks, we define a model where an adversary seeks to hide a set of \emph{corrupted vertices} inside a graph $G^*$. To...