Academic Profile

Statistics

Similar Authors

Papers on arXiv

We show how to price and replicate a variety of barrier-style claims written on the $\log$ price $X$ and quadratic variation $\langle X \rangle$ of a risky asset. Our framework assumes no arbitrage,...

We introduce Argoverse 2 (AV2) - a collection of three datasets for perception and forecasting research in the self-driving domain. The annotated Sensor Dataset contains 1,000 sequences of multimoda...

We price and replicate a variety of claims written on the log price $X$ and quadratic variation $[X]$ of a risky asset, modeled as a positive semimartingale, subject to stochastic volatility and jum...

We continue a series of papers where prices of the barrier options written on the underlying, which dynamics follows some one factor stochastic model with time-dependent coefficients and the barrier...

We present Argoverse -- two datasets designed to support autonomous vehicle machine learning tasks such as 3D tracking and motion forecasting. Argoverse was collected by a fleet of autonomous vehicl...

In this paper we formulate a regression problem to predict realized volatility by using option price data and enhance VIX-styled volatility indices' predictability and liquidity. We test algorithms ...

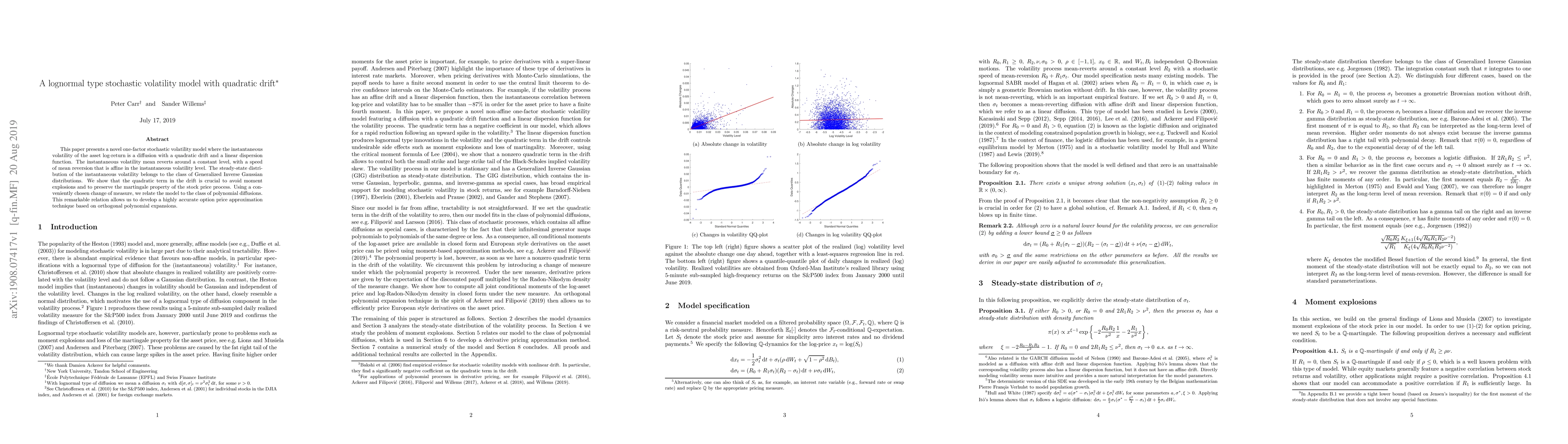

This paper presents a novel one-factor stochastic volatility model where the instantaneous volatility of the asset log-return is a diffusion with a quadratic drift and a linear dispersion function. ...

We derive a backward and forward nonlinear PDEs that govern the implied volatility of a contingent claim whenever the latter is well-defined. This would include at least any contingent claim written...

In this paper we apply Markovian approximation of the fractional Brownian motion (BM), known as the Dobric-Ojeda (DO) process, to the fractional stochastic volatility model where the instantaneous v...

We prove that the variance swap rate (fair strike) equals the price of a co-terminal European-style contract when the underlying is an exponential Markov process, time-changed by an arbitrary contin...