Academic Profile

Statistics

Similar Authors

Papers on arXiv

We propose a novel generative model for multivariate discrete-time time series data. Drawing inspiration from the construction of neural spline flows, our algorithm incorporates linear transformatio...

We present a method for finding optimal hedging policies for arbitrary initial portfolios and market states. We develop a novel actor-critic algorithm for solving general risk-averse stochastic cont...

We present an actor-critic-type reinforcement learning algorithm for solving the problem of hedging a portfolio of financial instruments such as securities and over-the-counter derivatives using pur...

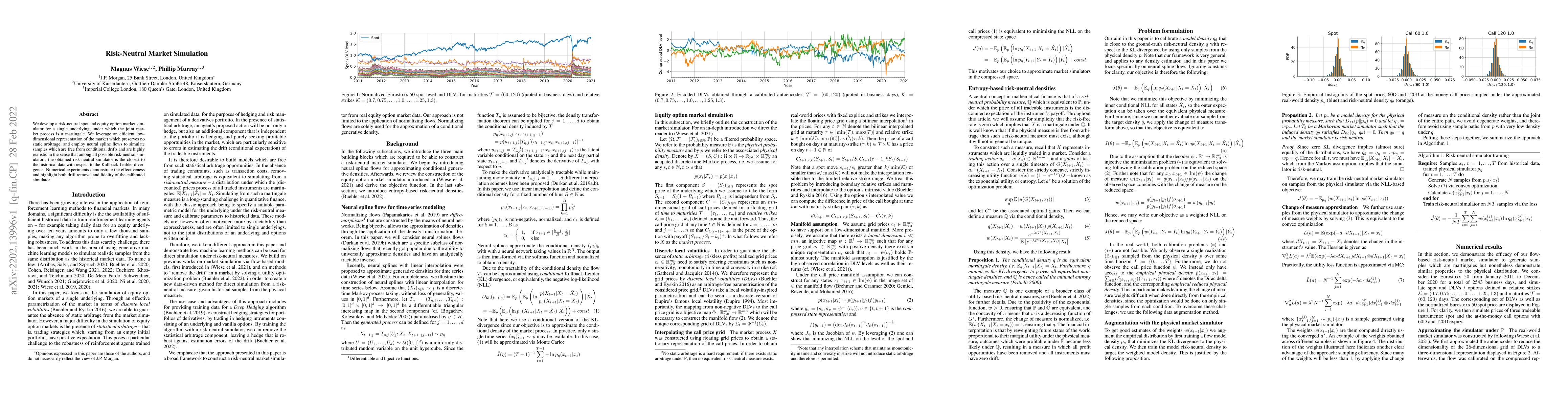

We develop a risk-neutral spot and equity option market simulator for a single underlying, under which the joint market process is a martingale. We leverage an efficient low-dimensional representati...

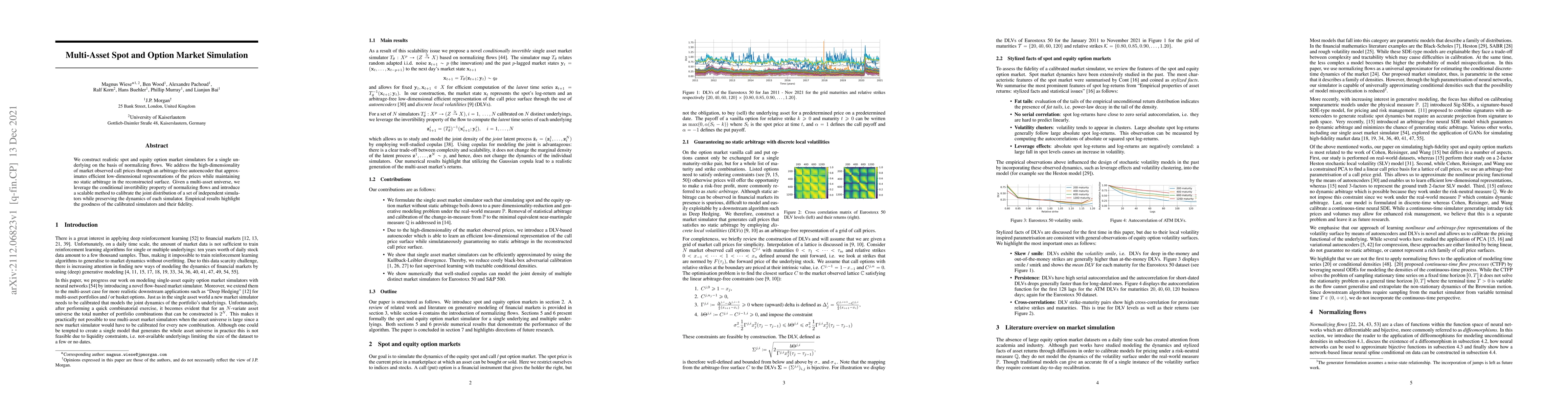

We construct realistic spot and equity option market simulators for a single underlying on the basis of normalizing flows. We address the high-dimensionality of market observed call prices through a...

We present a machine learning approach for finding minimal equivalent martingale measures for markets simulators of tradable instruments, e.g. for a spot price and options written on the same underl...

We present a numerically efficient approach for learning a risk-neutral measure for paths of simulated spot and option prices up to a finite horizon under convex transaction costs and convex trading...