Academic Profile

Statistics

Similar Authors

Papers on arXiv

Identification of market abuse is an extremely complicated activity that requires the analysis of large and complex datasets. We propose an unsupervised machine learning method for contextual anomal...

Networks of financial exposures are the key propagators of risk and distress among banks, but their empirical structure is not publicly available because of confidentiality. This limitation has trig...

Financial order flow exhibits a remarkable level of persistence, wherein buy (sell) trades are often followed by subsequent buy (sell) trades over extended periods. This persistence can be attribute...

Identifying market abuse activity from data on investors' trading activity is very challenging both for the data volume and for the low signal to noise ratio. Here we propose two complementary unsup...

Shannon entropy is the most common metric to measure the degree of randomness of time series in many fields, ranging from physics and finance to medicine and biology. Real-world systems may be in ge...

This paper presents results from the SESAR ER3 Domino project. Three mechanisms are assessed at the ECAC-wide level: 4D trajectory adjustments (a combination of actively waiting for connecting passe...

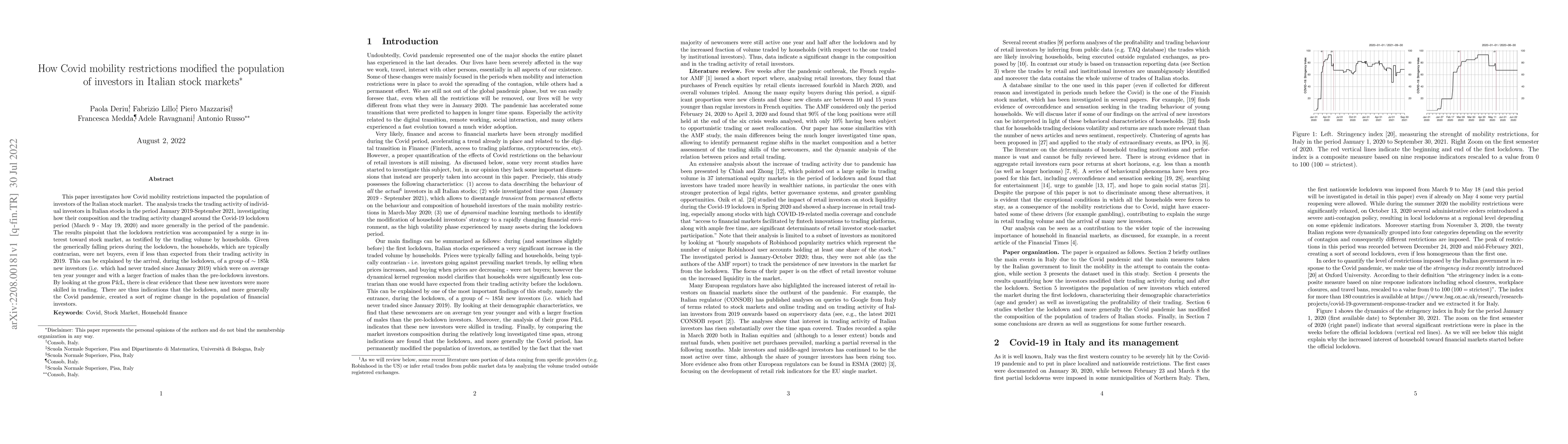

This paper investigates how Covid mobility restrictions impacted the population of investors of the Italian stock market. The analysis tracks the trading activity of individual investors in Italian ...

This paper investigates the degree of efficiency for the Moscow Stock Exchange. A market is called efficient if prices of its assets fully reflect all available information. We show that the degree ...

Betweenness centrality quantifies the importance of a vertex for the information flow in a network. We propose a flexible definition of betweenness for temporal multiplexes, where geodesics are dete...

Change points in real-world systems mark significant regime shifts in system dynamics, possibly triggered by exogenous or endogenous factors. These points define regimes for the time evolution of the ...

In the dynamic landscape of contemporary society, the popularity of ideas, opinions, and interests fluctuates rapidly. Traditional dynamical models in social sciences often fail to capture this inhere...

The level of systemic risk in economic and financial systems is strongly determined by the structure of the underlying networks of interdependent entities that can propagate shocks and stresses. Since...

In financial risk management, Value at Risk (VaR) is widely used to estimate potential portfolio losses. VaR's limitation is its inability to account for the magnitude of losses beyond a certain thres...

The Kelly criterion provides a general framework for optimizing the growth rate of an investment portfolio over time by maximizing the expected logarithmic utility of wealth. However, the optimality c...

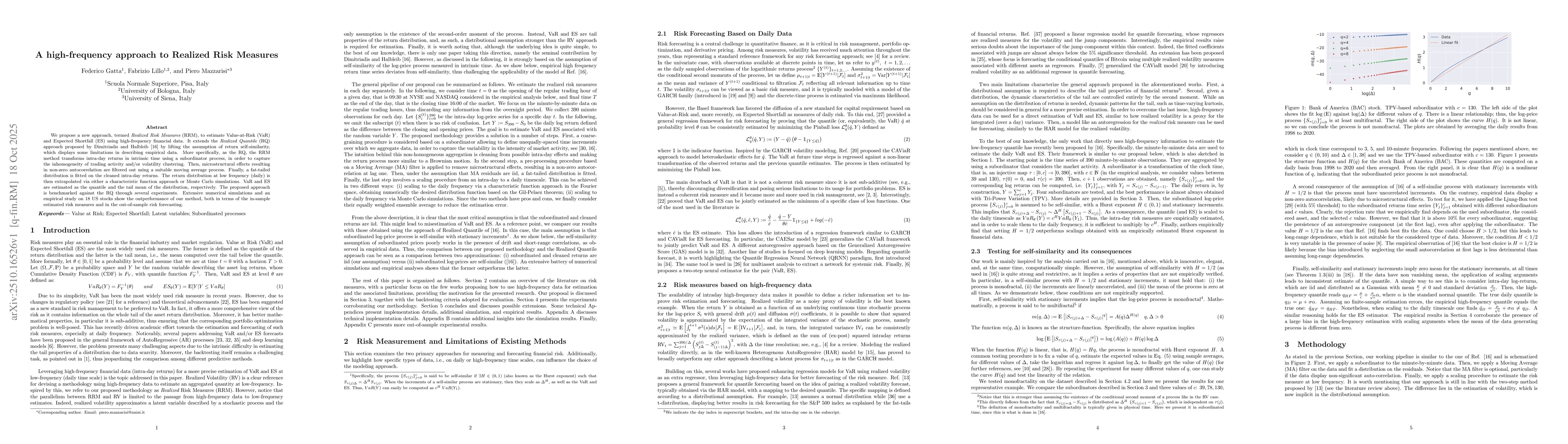

We propose a new approach, termed Realized Risk Measures (RRM), to estimate Value-at-Risk (VaR) and Expected Shortfall (ES) using high-frequency financial data. It extends the Realized Quantile (RQ) a...

Shorting for hedging exposes to risk when the market dynamics is uncertain. Managing uncertainty and risk exposure is key in portfolio management practice. This paper develops a robust framework for d...