Academic Profile

Statistics

Similar Authors

Papers on arXiv

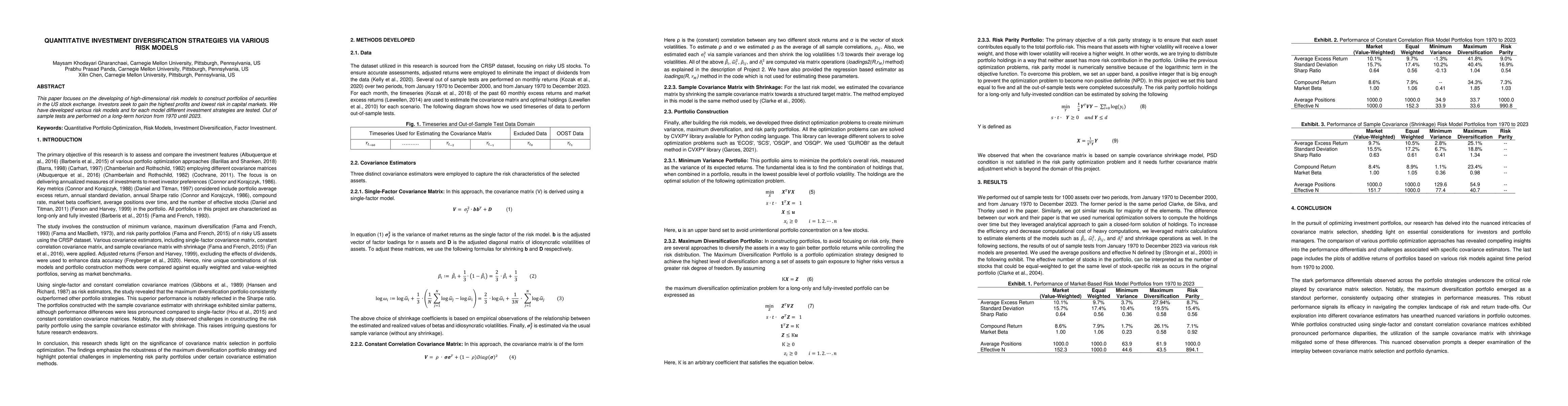

This paper focuses on the developing of high-dimensional risk models to construct portfolios of securities in the US stock exchange. Investors seek to gain the highest profits and lowest risk in cap...

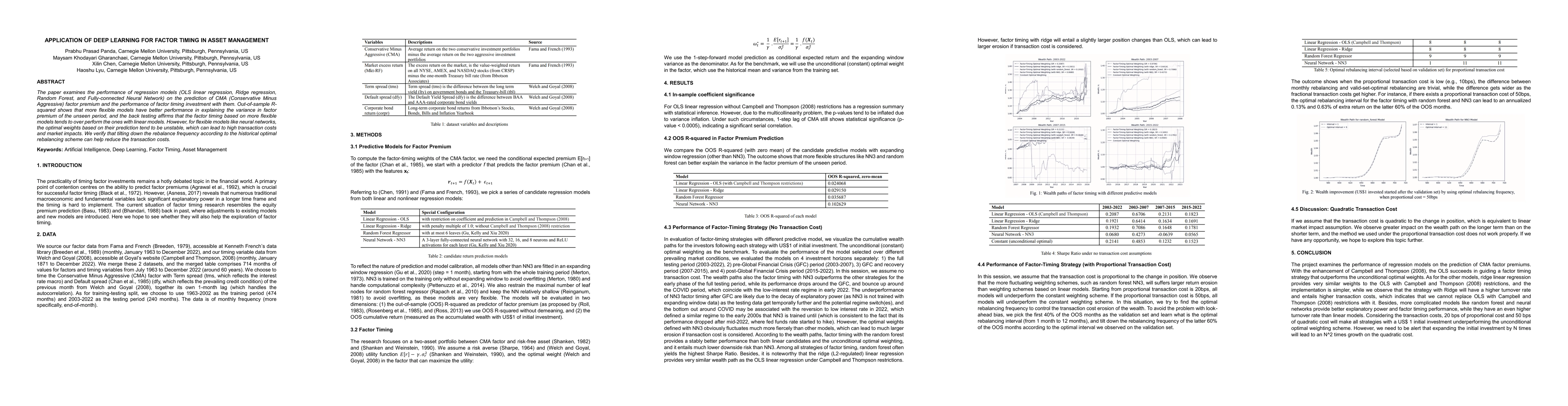

The paper examines the performance of regression models (OLS linear regression, Ridge regression, Random Forest, and Fully-connected Neural Network) on the prediction of CMA (Conservative Minus Aggr...

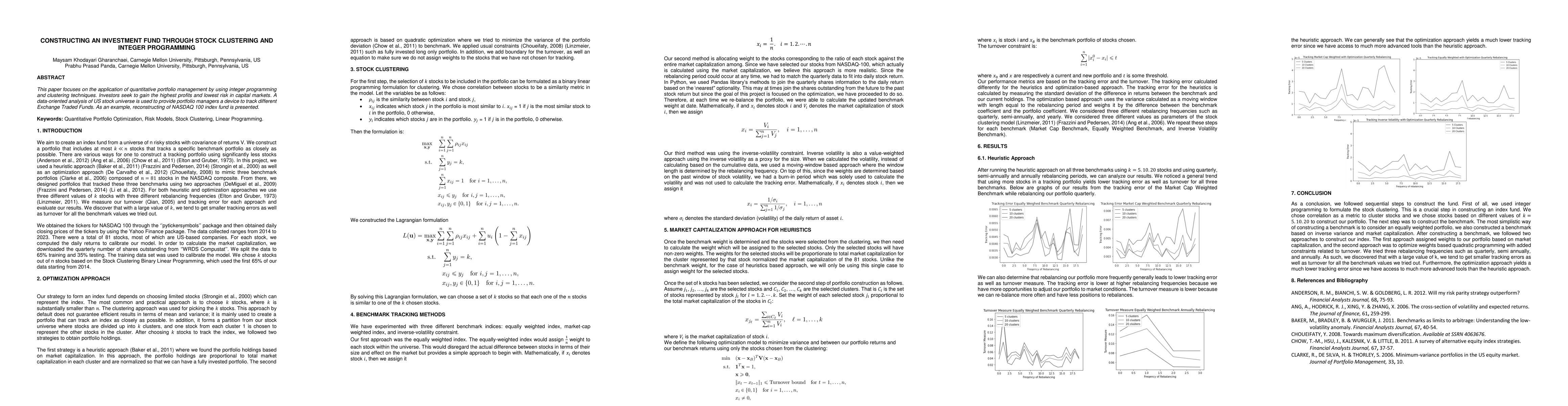

This paper focuses on the application of quantitative portfolio management by using integer programming and clustering techniques. Investors seek to gain the highest profits and lowest risk in capital...