Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper introduces a novel stochastic control framework to enhance the capabilities of automated investment managers, or robo-advisors, by accurately inferring clients' investment preferences fro...

Diffusion models have emerged as a powerful tool rivaling GANs in generating high-quality samples with improved fidelity, flexibility, and robustness. A key component of these models is to learn the...

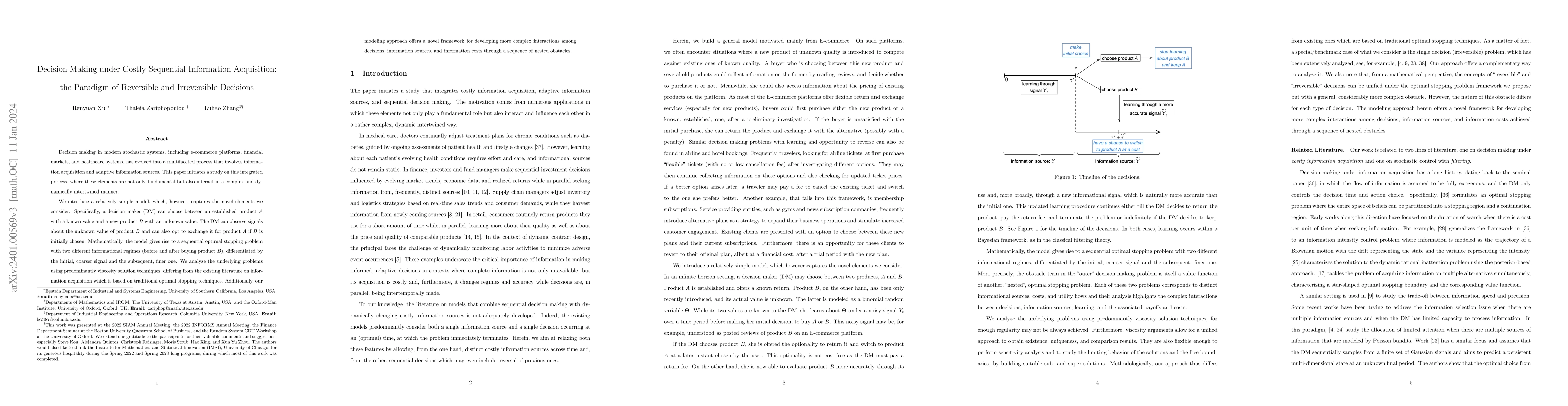

Decision making in modern stochastic systems, including e-commerce platforms, financial markets, and healthcare systems, has evolved into a multifaceted process that involves information acquisition...

This paper proposes and analyzes two new policy learning methods: regularized policy gradient (RPG) and iterative policy optimization (IPO), for a class of discounted linear-quadratic control (LQC) ...

Reinforcement Learning (RL) has gained substantial attention across diverse application domains and theoretical investigations. Existing literature on RL theory largely focuses on risk-neutral setti...

We consider two-player non-zero-sum linear-quadratic Gaussian games in which both players aim to minimize a quadratic cost function while controlling a linear and stochastic state process {using lin...

Nonlinear control systems with partial information to the decision maker are prevalent in a variety of applications. As a step toward studying such nonlinear systems, this work explores reinforcemen...

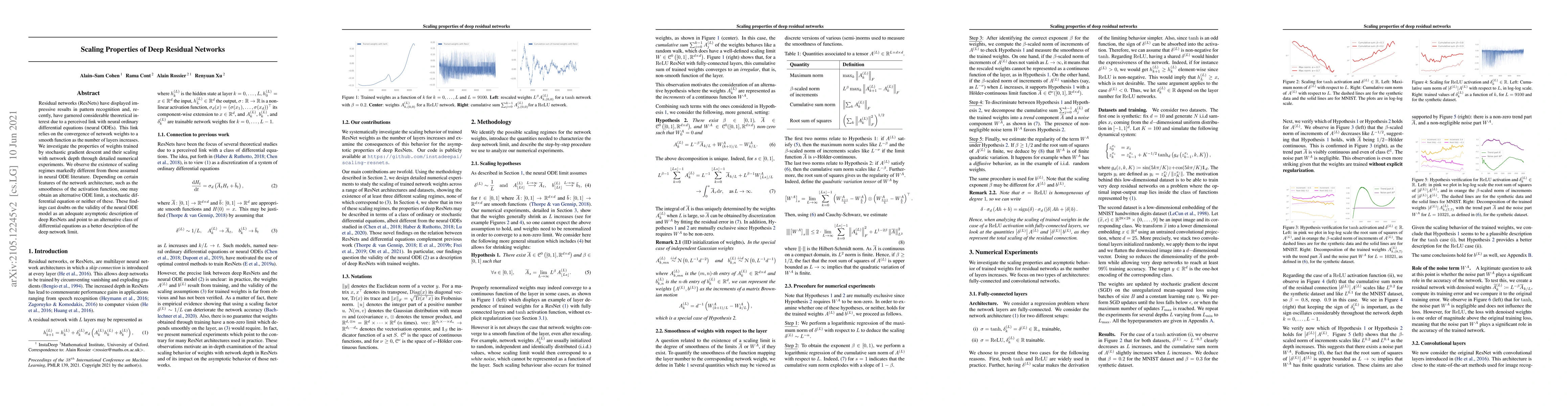

We investigate the asymptotic properties of deep Residual networks (ResNets) as the number of layers increases. We first show the existence of scaling regimes for trained weights markedly different ...

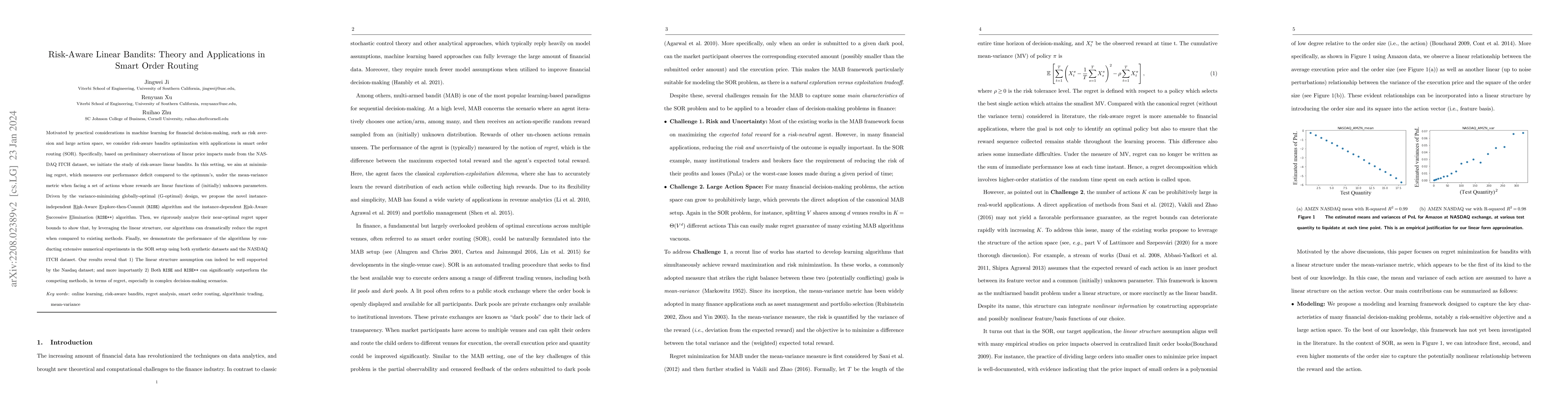

Motivated by practical considerations in machine learning for financial decision-making, such as risk aversion and large action space, we consider risk-aware bandits optimization with applications i...

The estimation of loss distributions for dynamic portfolios requires the simulation of scenarios representing realistic joint dynamics of their components, with particular importance devoted to the ...

The rapid changes in the finance industry due to the increasing amount of data have revolutionized the techniques on data processing and data analysis and brought new theoretical and computational c...

One of the challenges for multi-agent reinforcement learning (MARL) is designing efficient learning algorithms for a large system in which each agent has only limited or partial information of the e...

We consider a general-sum N-player linear-quadratic game with stochastic dynamics over a finite horizon and prove the global convergence of the natural policy gradient method to the Nash equilibrium...

Residual networks (ResNets) have displayed impressive results in pattern recognition and, recently, have garnered considerable theoretical interest due to a perceived link with neural ordinary diffe...

We introduce a model-free approach based on excursions of trading signals for analyzing the risk and return for a broad class of dynamic trading strategies, including pairs trading and other statist...

Entropy regularization has been extensively adopted to improve the efficiency, the stability, and the convergence of algorithms in reinforcement learning. This paper analyzes both quantitatively and...

This paper presents a general mean-field game (GMFG) framework for simultaneous learning and decision-making in stochastic games with a large population. It first establishes the existence of a uniq...

In this paper, we consider online learning in generalized linear contextual bandits where rewards are not immediately observed. Instead, rewards are available to the decision-maker only after some d...

Dynamic programming principle (DPP) is fundamental for control and optimization, including Markov decision problems (MDPs), reinforcement learning (RL), and more recently mean-field controls (MFCs)....

The electronic platform has been increasingly popular for executing large corporate bond orders by asset managers, who in turn have to assess the quality of their executions via Transaction Cost Ana...

This paper presents a general mean-field game (GMFG) framework for simultaneous learning and decision-making in stochastic games with a large population. It first establishes the existence of a uniq...

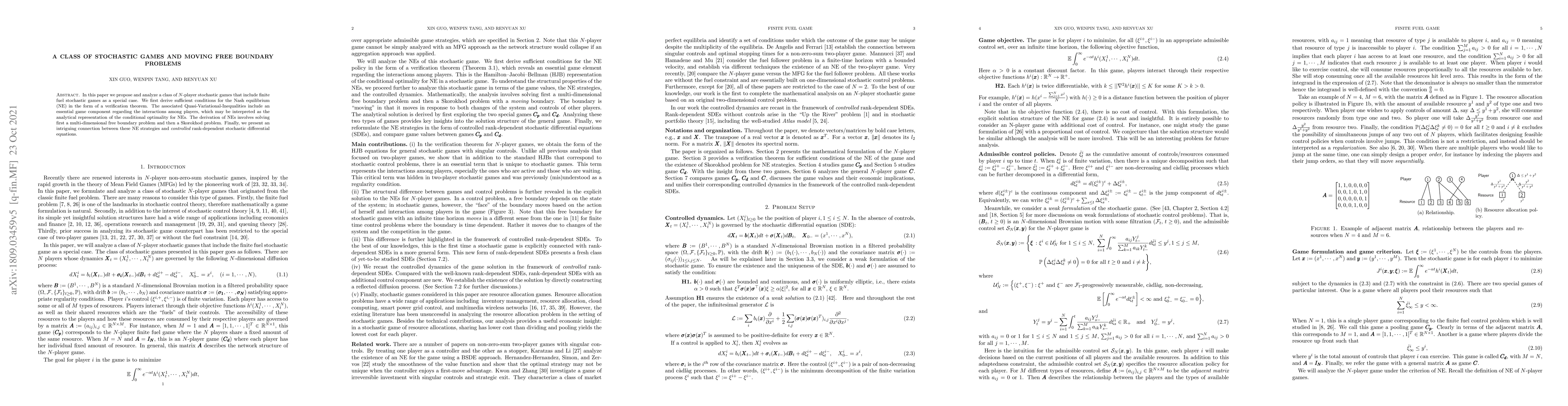

In this paper we propose and analyze a class of $N$-player stochastic games that include finite fuel stochastic games as a special case. We first derive sufficient conditions for the Nash equilibriu...

This paper explores continuous-time and state-space optimal stopping problems from a reinforcement learning perspective. We begin by formulating the stopping problem using randomized stopping times, w...

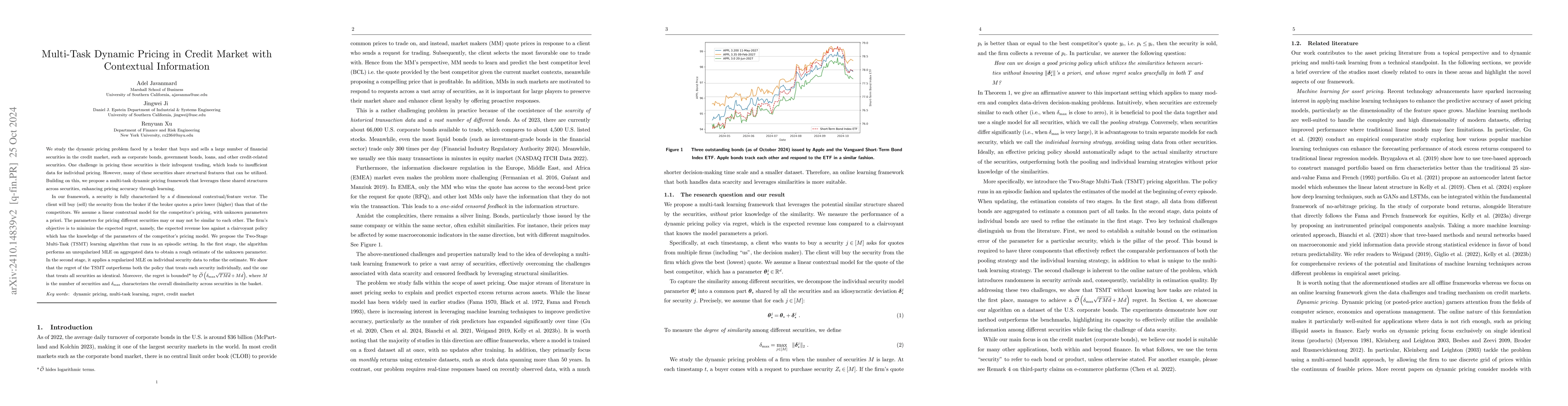

We study the dynamic pricing problem faced by a broker that buys and sells a large number of financial securities in the credit market, such as corporate bonds, government bonds, loans, and other cred...

Motivated by recent empirical findings on the periodic phenomenon of aggregated market volumes in equity markets, we aim to understand the causes and consequences of periodic trading activities throug...

Diffusion models have emerged as powerful tools for generative modeling, demonstrating exceptional capability in capturing target data distributions from large datasets. However, fine-tuning these mas...

Financial scenario simulation is essential for risk management and portfolio optimization, yet it remains challenging especially in high-dimensional and small data settings common in finance. We propo...

We study mean-field games of optimal stopping (OS-MFGs) and introduce an entropy-regularized framework to enable learning-based solution methods. By utilizing randomized stopping times, we reformulate...

Generative AI can be framed as the problem of learning a model that maps simple reference measures into complex data distributions, and it has recently found a strong connection to the classical theor...

We study reinforcement learning for controlled diffusion processes with unbounded continuous state spaces, bounded continuous actions, and polynomially growing rewards: settings that arise naturally i...

We study conditional generation in diffusion models under hard constraints, where generated samples must satisfy prescribed events with probability one. Such constraints arise naturally in safety-crit...

Motivated by modern machine learning applications where we only have access to empirical measures constructed from finite samples, we relax the marginal constraints of the classical Schrödinger bridge...

We investigate an entropy-regularized reinforcement learning (RL) approach to optimal stopping problems motivated by real option models. Classical stopping rules are strict and non-randomized, limitin...

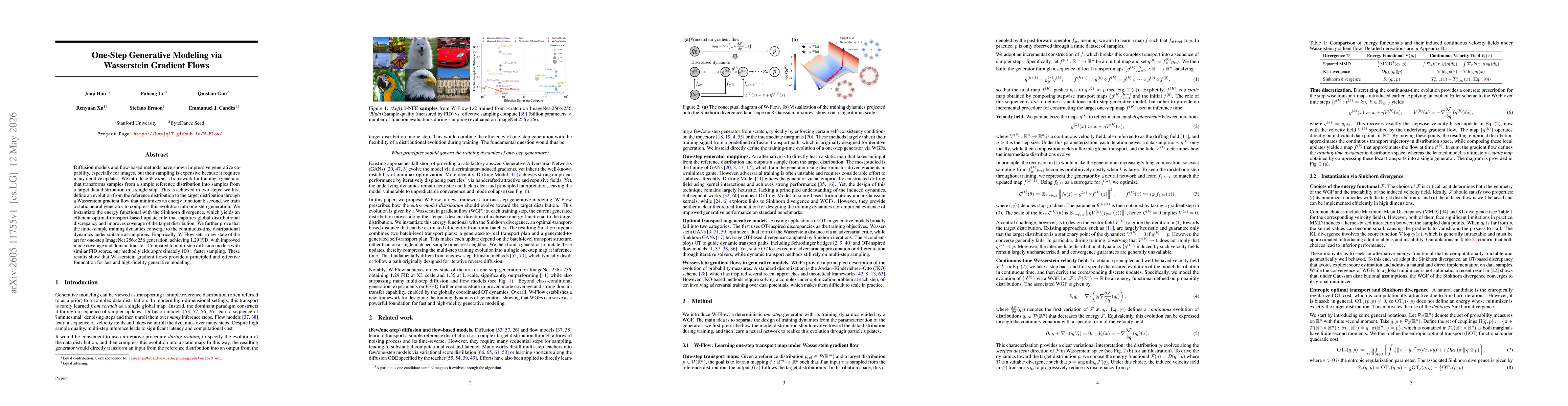

Diffusion models and flow-based methods have shown impressive generative capability, especially for images, but their sampling is expensive because it requires many iterative updates. We introduce W-F...

Bi-causal optimal transport (OT) is a natural framework for comparing and coupling stochastic processes under nonanticipative information constraints, with important applications in robust finance, se...

Generating realistic synthetic sequential data is critical in real-world applications across operations research, finance, healthcare, energy systems, and scientific computing, where time-indexed obse...

Diffusion-based policies have recently emerged as powerful policy parameterizations for reinforcement learning, representing state-conditioned action distributions as terminal laws of diffusion proces...