Multi-Task Dynamic Pricing in Credit Market with Contextual Information

Publication

Metrics

AI Quick Summary

This paper proposes a multi-task dynamic pricing framework for securities in the credit market that leverages shared structural features across different securities to enhance pricing accuracy. The framework minimizes expected regret compared to competitor pricing and demonstrates bounded regret, outperforming both individual and uniform pricing policies.

Paper Preview

Abstract

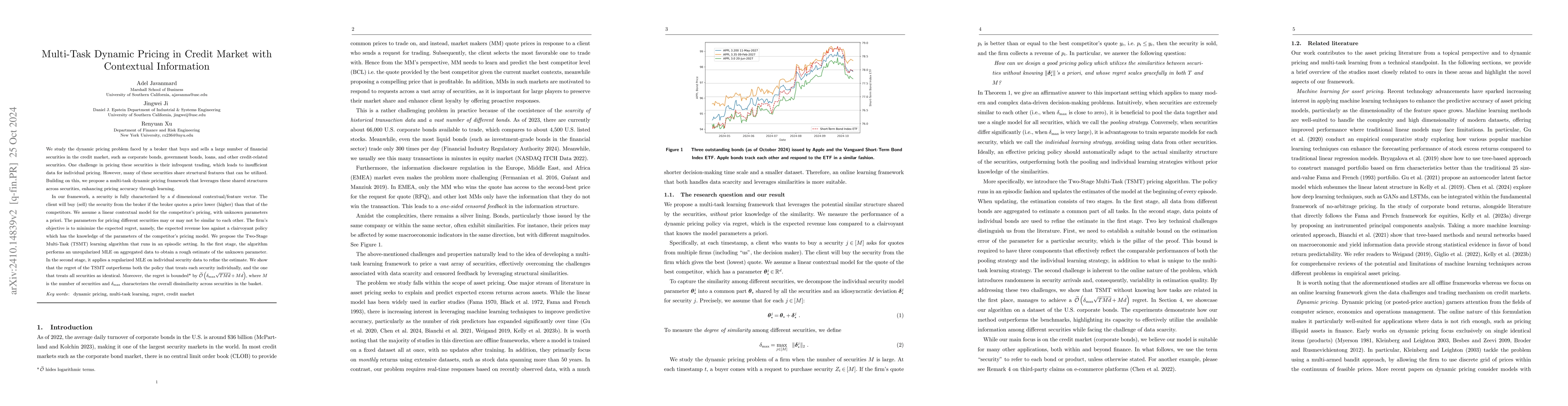

We study the dynamic pricing problem faced by a broker that buys and sells a large number of financial securities in the credit market, such as corporate bonds, government bonds, loans, and other credit-related securities. One challenge in pricing these securities is their infrequent trading, which leads to insufficient data for individual pricing. However, many of these securities share structural features that can be utilized. Building on this, we propose a multi-task dynamic pricing framework that leverages these shared structures across securities, enhancing pricing accuracy through learning. In our framework, a security is fully characterized by a $d$ dimensional contextual/feature vector. The customer will buy (sell) the security from the broker if the broker quotes a price lower (higher) than that of the competitors. We assume a linear contextual model for the competitor's pricing, with unknown parameters a prior. The parameters for pricing different securities may or may not be similar to each other. The firm's objective is to minimize the expected regret, namely, the expected revenue loss against a clairvoyant policy which has the knowledge of the parameters of the competitor's pricing model. We show that the regret of our policy is better than both a policy that treats each security individually and a policy that treats all securities as the same. Moreover, the regret is bounded by $\tilde{O} ( \delta_{\max} \sqrt{T M d} + M d ) $, where $M$ is the number of securities and $\delta_{\max}$ characterizes the overall dissimilarity across securities in the basket.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0