Academic Profile

Statistics

Similar Authors

Papers on arXiv

Left truncated and right censored data are encountered frequently in insurance loss data due to deductibles and policy limits. Risk estimation is an important task in insurance as it is a necessary ...

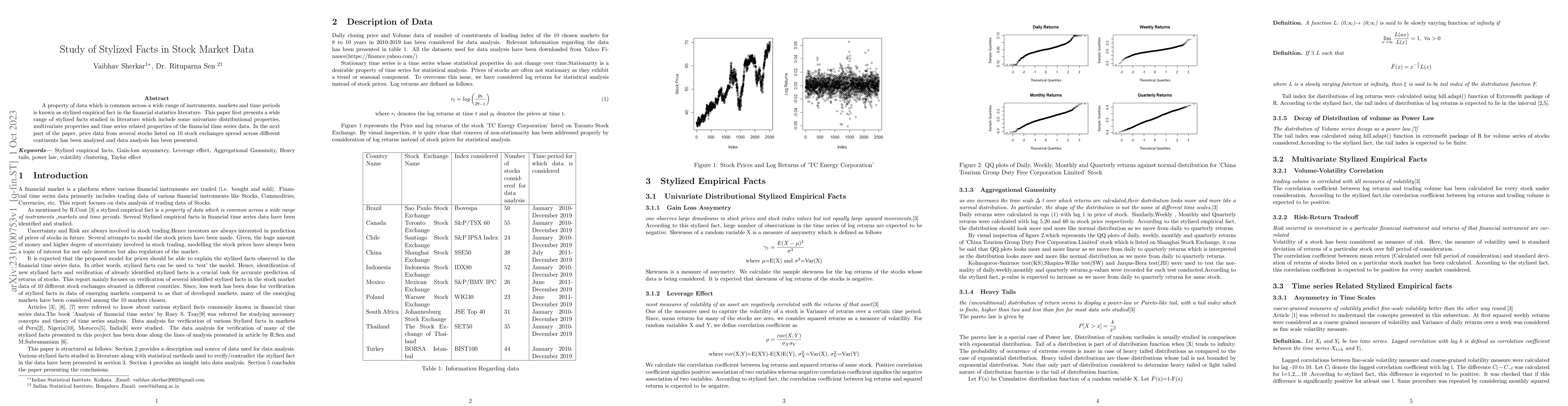

A property of data which is common across a wide range of instruments, markets and time periods is known as stylized empirical fact in the financial statistics literature. This paper first presents ...

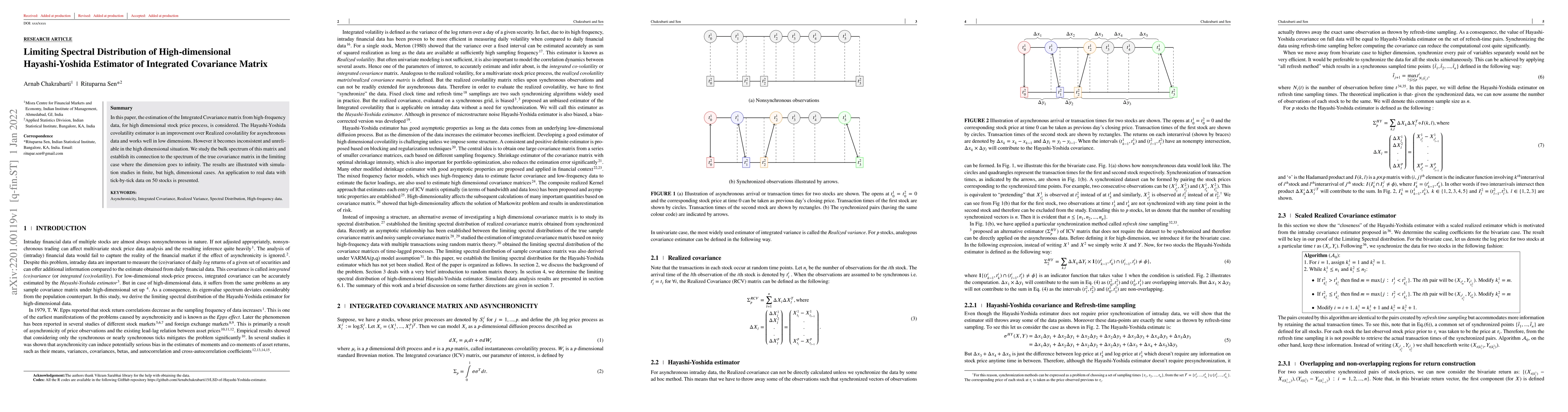

In this paper, the estimation of the Integrated Covariance matrix from high-frequency data, for high dimensional stock price process, is considered. The Hayashi-Yoshida covolatility estimator is an ...

We develop a multivariate functional autoregressive model (MFAR), which captures the cross-correlation among multiple functional time series and thus improves forecast accuracy. We estimate the para...

For a long investment time horizon, it is preferable to rebalance the portfolio weights at intermediate times. This necessitates a multi-period market model in which portfolio optimization is usuall...

Copula is a powerful tool to model multivariate data. We propose the modelling of intraday financial returns of multiple assets through copula. The problem originates due to the asynchronous nature ...

Historical daily data for eleven years of the fifty constituent stocks of the NIFTY index traded on the National Stock Exchange have been analyzed to check for the stylized facts in the Indian marke...

Spectral risk measures (SRMs) belong to the family of coherent risk measures. A natural estimator for the class of SRMs has the form of L-statistics. Various authors have studied and derived the asy...

For high dimensional data, some of the standard statistical techniques do not work well. So modification or further development of statistical methods are necessary. In this paper, we explore these ...

Diffusion processes driven by Fractional Brownian motion (FBM) have often been considered in modeling stock price dynamics in order to capture the long range dependence of stock price observed in re...

Widely used income inequality measure, Gini index is extended to form a family of income inequality measures known as Single-Series Gini (S-Gini) indices. In this study, we develop empirical likelih...

We presented Bayesian portfolio selection strategy, via the $k$ factor asset pricing model. If the market is information efficient, the proposed strategy will mimic the market; otherwise, the strate...

Historically, financial risk management has mostly addressed risk factors that arise from the financial environment. Climate risks present a novel and significant challenge for companies and financial...