Academic Profile

Statistics

Similar Authors

Papers on arXiv

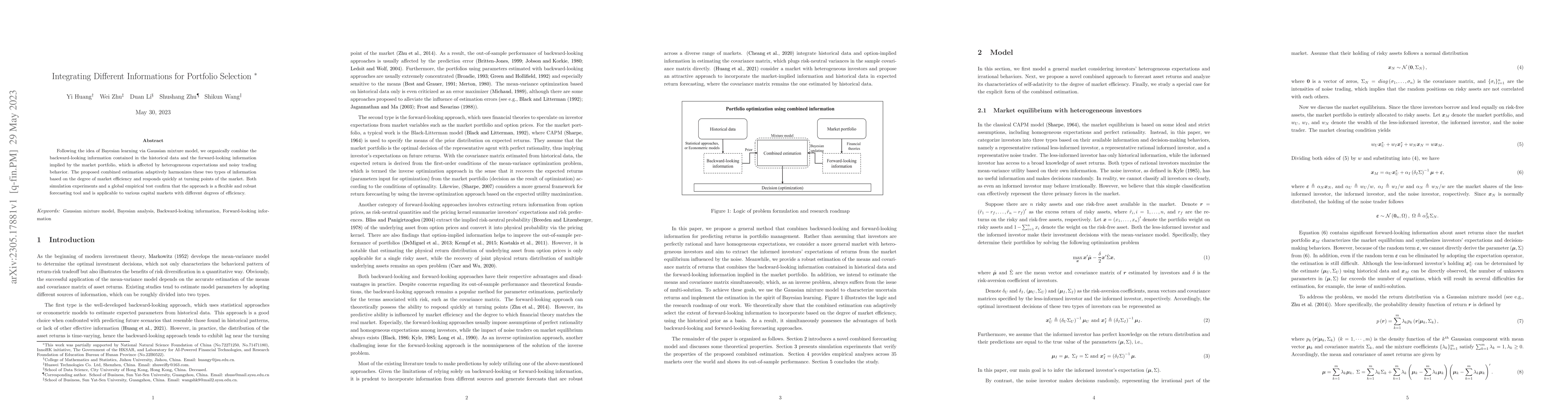

Following the idea of Bayesian learning via Gaussian mixture model, we organically combine the backward-looking information contained in the historical data and the forward-looking information impli...

This paper investigates the stochastic program with the chance constraint on a quadratic form of random variables following multivariate Gaussian mixture distribution (GMD). Under some mild conditio...

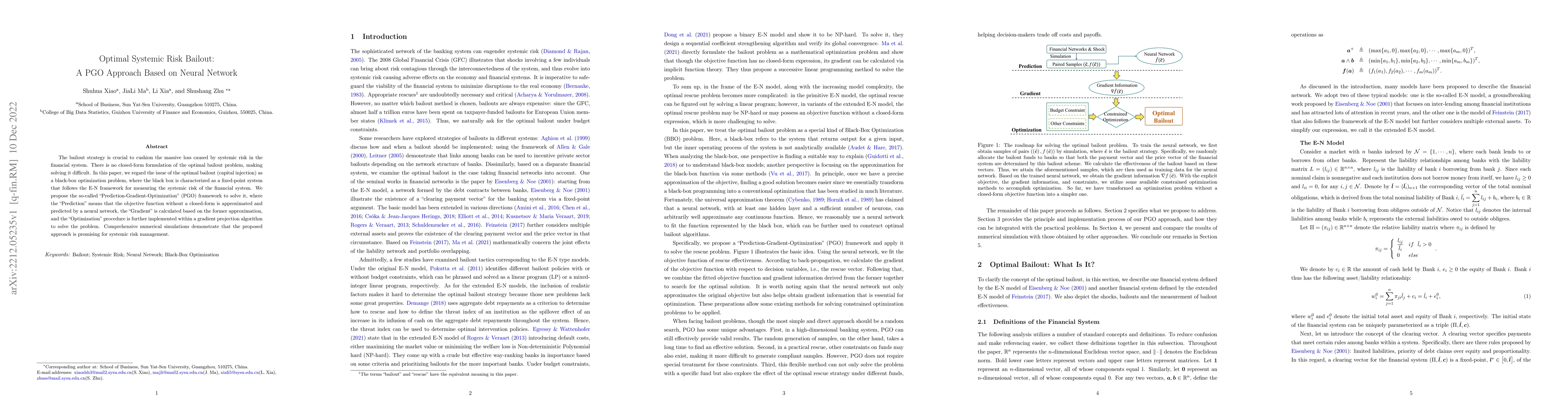

The bailout strategy is crucial to cushion the massive loss caused by systemic risk in the financial system. There is no closed-form formulation of the optimal bailout problem, making solving it dif...

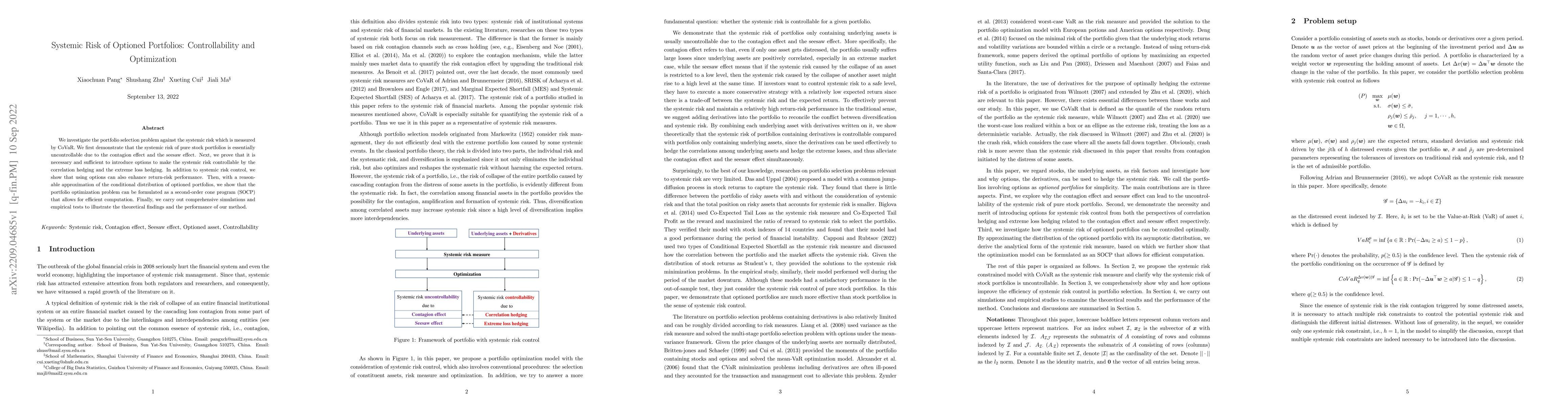

We investigate the portfolio selection problem against the systemic risk which is measured by CoVaR. We first demonstrate that the systemic risk of pure stock portfolios is essentially uncontrollabl...