Academic Profile

Statistics

Similar Authors

Papers on arXiv

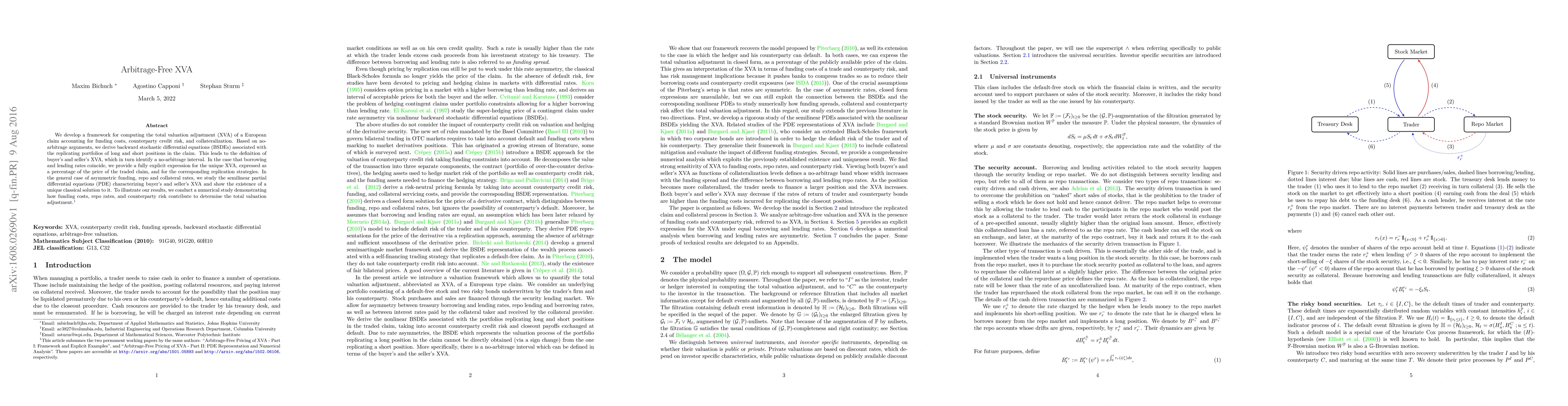

We develop a framework for computing the total valuation adjustment (XVA) of a European claim accounting for funding costs, counterparty credit risk, and collateralization. Based on no-arbitrage arg...

We aim to provide an intertemporal, cost-efficient consumption model that extends the consumption optimization inspired by the Distribution Builder, a tool developed by Sharpe, Johnson, and Goldstei...

This paper studies the topic of cost-efficiency in incomplete markets. A portfolio payoff is called cost-efficient if it achieves a given probability distribution at some given investment horizon wi...

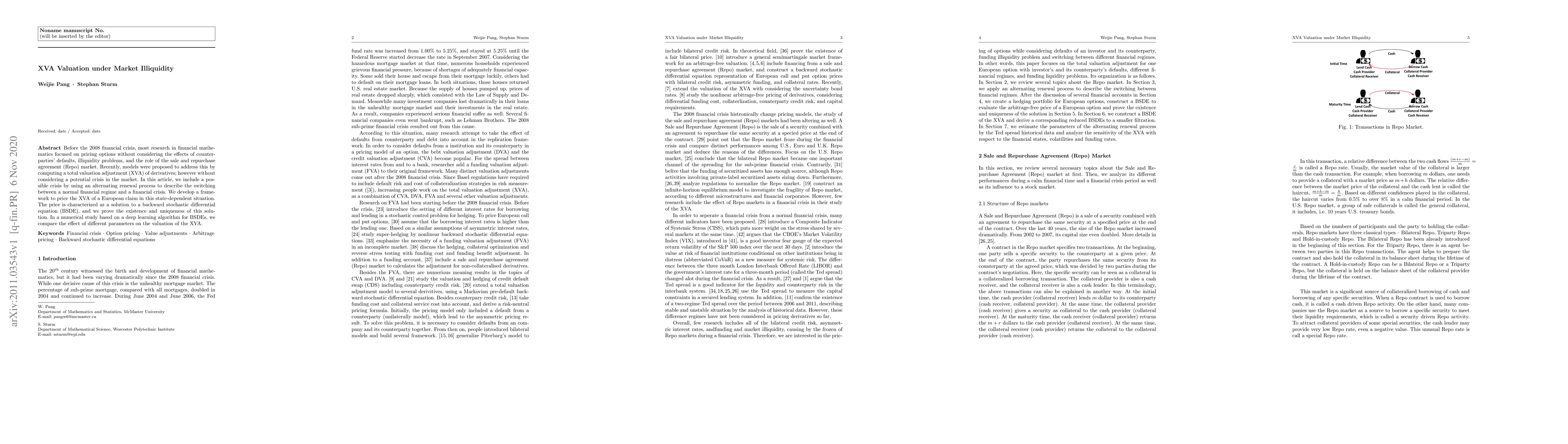

Before the 2008 financial crisis, most research in financial mathematics focused on pricing options without considering the effects of counterparties' defaults, illiquidity problems, and the role of...

This paper discusses the sensitivity of the long-term expected utility of optimal portfolios for an investor with constant relative risk aversion. Under an incomplete market given by a factor model,...

We introduce a two-agent problem which is inspired by price asymmetry arising from funding difference. When two parties have different funding rates, the two parties deduce different fair prices for...

We introduce an arbitrage-free framework for robust valuation adjustments. An investor trades a credit default swap portfolio with a risky counterparty, and hedges credit risk by taking a position i...

This paper studies the pricing of contingent claims of American style, using indifference pricing by fully dynamic convex risk measures. We provide a general definition of risk-indifference prices for...

We present a number of examples and counterexamples to illustrate the results on cost-efficiency in an incomplete market obtained in [BS24]. These examples and counterexamples do not only illustrate t...

Signature methods have been widely and effectively used as a tool for feature extraction in statistical learning methods, notably in mathematical finance. They lack, however, interpretability: in the ...

We provide an introduction to the topic of path signatures as means of feature extraction for machine learning from data streams. The article stresses the mathematical theory underlying the signature ...