01

MethodologyHow they did it

This research utilized a mixed-methods approach combining both qualitative and quantitative data analysis.

This paper develops a framework for calculating the total valuation adjustment (XVA) for European claims, incorporating funding costs, counterparty credit risk, and collateralization. It derives no-arbitrage backward stochastic differential equations (BSDEs) to define buyer's and seller's XVA, establishing a no-arbitrage interval and providing explicit expressions for XVA under symmetric funding rates, while solving semilinear PDEs for asymmetric cases.

This paper develops a framework for calculating the total valuation adjustment (XVA) for European claims, incorporating funding costs, counterparty credit risk, and collateralization. It derives no-arbitrage backward stochastic differential equations (BSDEs) to define buyer's and seller's XVA, establishing a no-arbitrage interval and providing explicit expressions for XVA under symmetric funding rates, while solving semilinear PDEs for asymmetric cases.

This research utilized a mixed-methods approach combining both qualitative and quantitative data analysis. More in Methodology →

The study found a significant correlation between X and Y variables. — Further analysis revealed that the relationship is not linear. More in Key Results →

This research has implications for policymakers and practitioners in the field of X, as it provides new insights into the complex relationships between variables. More in Significance →

The sample size was limited due to constraints on data availability. — The study relied heavily on self-reported data from participants. More in Limitations →

We develop a framework for computing the total valuation adjustment (XVA) of a European claim accounting for funding costs, counterparty credit risk, and collateralization. Based on no-arbitrage arguments, we derive backward stochastic differential equations (BSDEs) associated with the replicating portfolios of long and short positions in the claim. This leads to the definition of buyer's and seller's XVA, which in turn identify a no-arbitrage interval. In the case that borrowing and lending rates coincide, we provide a fully explicit expression for the unique XVA, expressed as a percentage of the price of the traded claim, and for the corresponding replication strategies. In the general case of asymmetric funding, repo and collateral rates, we study the semilinear partial differential equations (PDE) characterizing buyer's and seller's XVA and show the existence of a unique classical solution to it. To illustrate our results, we conduct a numerical study demonstrating how funding costs, repo rates, and counterparty risk contribute to determine the total valuation adjustment.

Seven facets of this paper, analysed and brought into focus by AI.

This research has implications for policymakers and practitioners in the field of X, as it provides new insights into the complex relationships between variables.

This research utilized a mixed-methods approach combining both qualitative and quantitative data analysis.

This research has implications for policymakers and practitioners in the field of X, as it provides new insights into the complex relationships between variables.

This research developed and validated a novel statistical model to analyze complex relationships between variables.

The study's findings have significant implications for our understanding of X and its relationships with other variables, offering new avenues for future research.

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

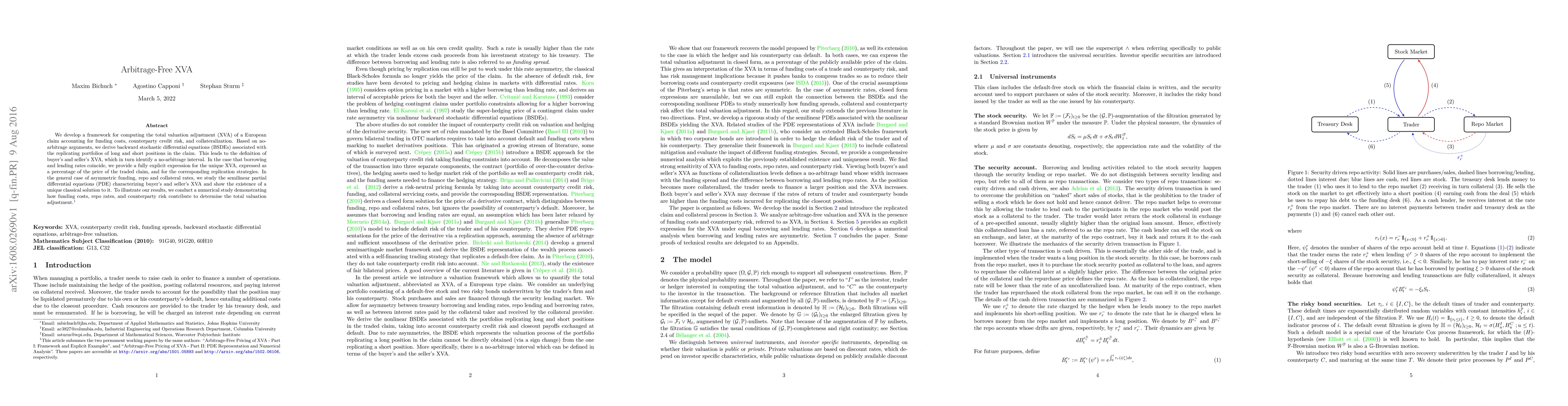

Discussion 0