Academic Profile

Statistics

Similar Authors

Papers on arXiv

We propose a distributional formulation of the spanning problem of a multi-asset payoff by vanilla basket options. This problem is shown to have a unique solution if and only if the payoff function ...

Motivated by the equations of cross valuation adjustments (XVAs) in the realistic case where capital is deemed fungible as a source of funding for variation margin, we introduce a simulation/regress...

Based on supermodularity ordering properties, we show that convex risk measures of credit losses are nondecreasing w.r.t. credit-credit and, in a wrong-way risk setup, credit-market, covariances of ...

This article is a follow up to Cr\'epey, Frikha, and Louzi (2023), where we introduced a nested stochastic approximation algorithm and its multilevel acceleration for computing the value-at-risk and...

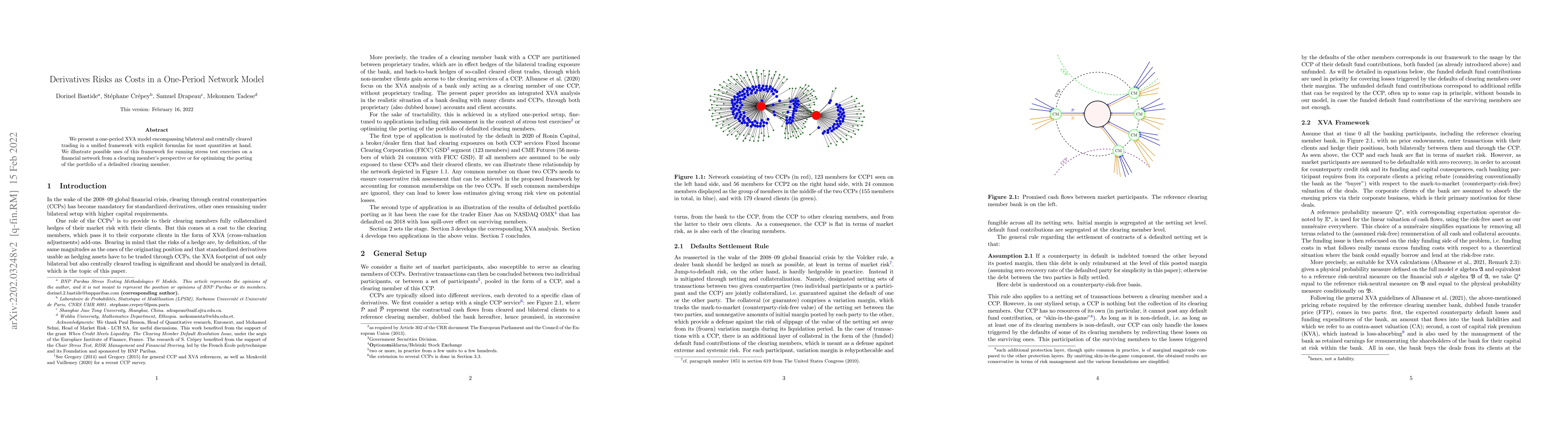

For vanilla derivatives that constitute the bulk of investment banks' hedging portfolios, central clearing through central counterparties (CCPs) has become hegemonic. A key mandate of a CCP is to pr...

Darwinian model risk is the risk of mis-price-and-hedge biased toward short-to-medium systematic profits of a trader, which are only the compensator of long term losses becoming apparent under extre...

We propose a multilevel stochastic approximation (MLSA) scheme for the computation of the value-at-risk (VaR) and expected shortfall (ES) of a financial loss, which can only be computed via simulati...

We explore the abilities of two machine learning approaches for no-arbitrage interpolation of European vanilla option prices, which jointly yield the corresponding local volatility surface: a finite...

We consider the computation by simulation and neural net regression of conditional expectations, or more general elicitable statistics, of functionals of processes $(X, Y )$. Here an exogenous compo...

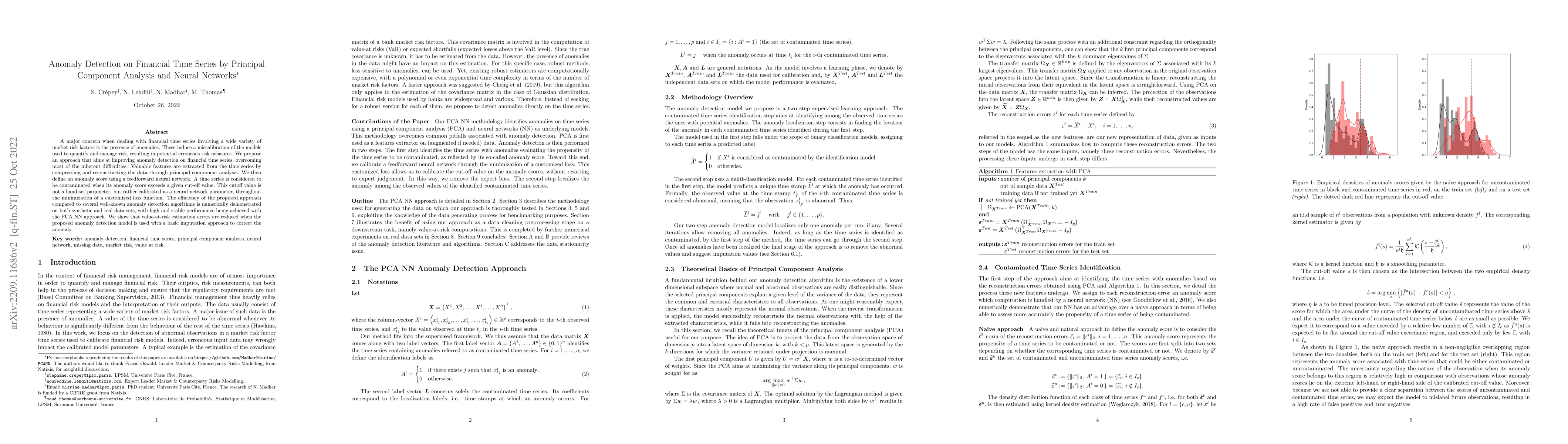

A major concern when dealing with financial time series involving a wide variety ofmarket risk factors is the presence of anomalies. These induce a miscalibration of the models used toquantify and m...

The dynamic hedging theory only makes sense in the setup of one given model, whereas the practice of dynamic hedging is just the opposite, with models fleeing after the data through daily recalibrat...

We present a one-period XVA model encompassing bilateral and centrally cleared trading in a unified framework with explicit formulas for most quantities at hand. We illustrate possible uses of this ...

Deep learning for option pricing has emerged as a novel methodology for fast computations with applications in calibration and computation of Greeks. However, many of these approaches do not enforce...

Cr\'epey, Frikha, and Louzi (2023) introduced a multilevel stochastic approximation scheme to compute the value-at-risk of a financial loss that is only simulatable by Monte Carlo. The optimal complex...

We present a unified framework for computing CVA sensitivities, hedging the CVA, and assessing CVA risk, using probabilistic machine learning meant as refined regression tools on simulated data, valid...

Emissions markets play a crucial role in reducing pollution by encouraging firms to minimize costs. However, their structure heavily relies on the decisions of policymakers, on the future economic act...

Invariance times are stopping times $\tau$ such that local martingales with respect to some reduced filtration and an equivalently changed probability measure, stopped before $\tau$ , are local martin...

Carbon pricing has become a central pillar of modern climate policy, with carbon taxes and emissions trading systems (ETS) serving as the two dominant approaches. Although economic theory suggests the...