Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce a mean field game for a family of filtering problems related to the classic sequential testing of the drift of a Brownian motion. To the best of our knowledge this work presents the fir...

Here, we develop a deep learning algorithm for solving Principal-Agent (PA) mean field games with market-clearing conditions -- a class of problems that have thus far not been studied and one that p...

In this paper we develop a concrete and fully implementable approach to the optimization of functionally generated portfolios in stochastic portfolio theory. The main idea is to optimize over a fami...

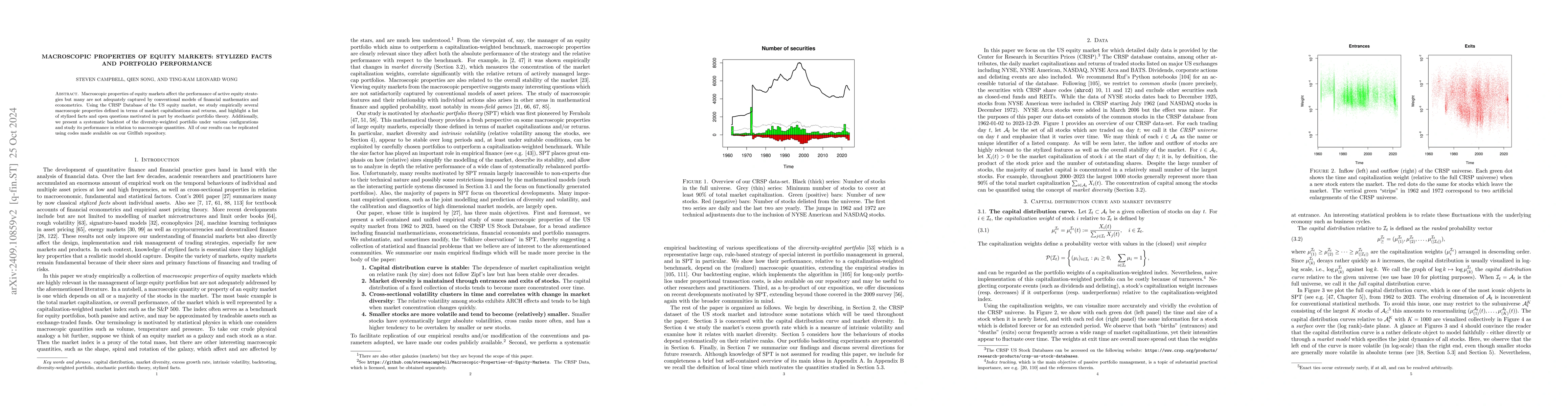

Macroscopic properties of equity markets affect the performance of active equity strategies but many are not adequately captured by conventional models of financial mathematics and econometrics. Using...

We study $N$-player optimal execution games in an Obizhaeva--Wang model of transient price impact. When the game is regularized by an instantaneous cost on the trading rate, a unique equilibrium exist...

In this note we introduce and solve a soft classification version of the famous Bayesian sequential testing problem for a Brownian motion's drift. We establish that the value function is the unique no...

We study a sequential estimation problem for an unknown reward in the presence of a random horizon. The reward takes one of two predetermined values which can be inferred from the drift of a Wiener pr...

We study optimal execution in markets with transient price impact in a competitive setting with $N$ traders. Motivated by prior negative results on the existence of pure Nash equilibria, we consider r...

Passive liquidity providers (LPs) in automated market makers (AMMs) face losses due to adverse selection (LVR), which static trading fees often fail to offset in practice. We study the key determinant...

We study a controlled version of the Bayesian sequential testing problem for the drift of a Wiener process, in which the observer exercises discretion over the signal intensity. This control incurs a ...

We study the excess growth rate -- a fundamental logarithmic functional arising in portfolio theory -- from the perspective of information theory. We show that the excess growth rate can be connected ...

Auto-deleveraging (ADL) mechanisms are a critical yet understudied component of risk management on cryptocurrency futures exchanges. When available margin and other loss-absorbing resources are insuff...

We study optimal portfolio choice for a household simultaneously managing a random-deadline goal, such as a medical emergency or job loss, and a fixed-deadline goal such as retirement or college tuiti...